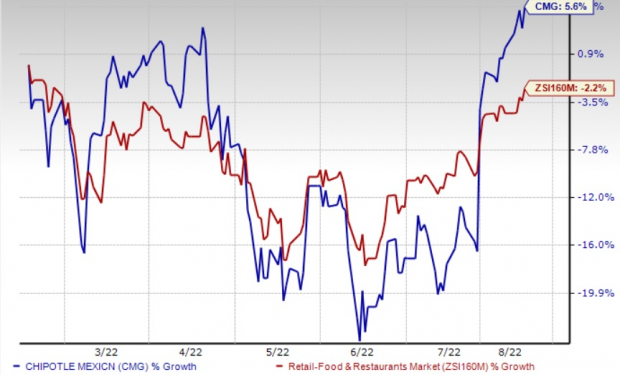

Chipotle Mexican Grill, Inc. (NYSE:CMG) is benefiting from comps growth, strength in digital sales, rise in menu prices and new restaurant openings. In the past six months, shares of the company have gained 5.6%, against the industry's decline of 2.2%. However, supply chain challenges, elevated wage inflation and expenses associated with new menus remain headwinds. Let's delve deeper.

Growth Drivers

Impressive comps performance continues to drive growth. Despite the pandemic, the company reported comps growth for the eighth straight quarter. During the second quarter, comparable restaurant sales increased 10.1% year over year, following growth of 9% (in first-quarter 2022), 15.2% (in fourth-quarter 2021), 15.1% (third-quarter 2021), 31.2% (second-quarter 2021), 17.2% (first-quarter 2021) and 5.7% (fourth-quarter 2020). Consistent strength in digital sales, solid recovery of in-restaurant sales and positive customer reception to new menu items contributed to the company's results. For the third quarter, the company expects comps growth, including planned price increases in August, in the mid to high single-digits.

The company's focus on expansion efforts bodes well. During the first and second quarters of 2022, Chipotle opened 51 and 42 new restaurants, including 42 and 32 Chipotlanes, respectively. The addition of Chipotlane enhanced customer access and convenience and bolstered new store restaurant sales, margins and returns. It continues to expand its digital drive with Chipotlane. The company has opened a digital-only kitchen as well. In 2022, the company expects to open 235-250 restaurants, with at least 80% of them including a Chipotlane. The company currently has 430 Chipotlanes.

Backed by impressive unit economics and the success of small-town locations, the company anticipates operating more than 7,000 restaurants in the long term in North America. CMG emphasized building a real estate pipeline with more than 80% of the restaurants having Chipotlane in it. The company anticipates its annual unit growth rate in the range of 8-10%.

Meanwhile, the company has been focusing on human capital technology to enhance the team member experience in its restaurants, paving the path for a more efficient, consistent and compliant environment. During the first quarter of 2022, the company initiated the testing of an autonomous kitchen assistant – Chippy – that integrates culinary traditions with artificial intelligence to make tortilla chips. The initiative involves robotics collaboration, thereby allowing the company to focus on other culinary tasks in the restaurant without sacrificing the quality and deliciousness of the item. The company plans to implement the initiative in a Southern California restaurant and leverage it with the stage-gate process before deciding its future course of implementation. Apart from this, the company has also rolled out a new labor scheduling program and initiated testing radio frequency identification technology to enhance traceability and inventory systems.

Concerns

The restaurant industry has been facing declining traffic for quite some time. The pandemic has aggravated the scenario. A rapid increase in menu prices and the coronavirus pandemic are the primary reasons behind the traffic erosion. The company said traffic continues to hurt the industry.

The company, like other industry players, has been facing significant supply chain challenges and inflation across most commodities and categories. During second-quarter 2022, food, beverage and packaging costs, as a percentage of revenues, remained flat year over year to 30.4%. In the second quarter of 2022, the benefit of menu price increases was overshadowed by higher costs for avocados, packaging, dairy, beef and chicken. For third-quarter 2022, the company anticipates labor cost to be 25% on account of leverage from the menu price increases.

Chipotle currently has a Zacks Rank #3 (Hold).

Key Picks

Some better-ranked stocks in the Zacks Retail-Wholesale sector are Potbelly Corporation (NASDAQ:PBPB), Arcos Dorados Holdings Inc. (NYSE:ARCO) and Dollar Tree Inc. (NASDAQ:DLTR).

Potbelly has a Zacks Rank #2 (Buy), at present. PBPB has a trailing four-quarter earnings surprise of 26.2%, on average. Shares of PBPB have declined 15.3% in the past year.

The Zacks Consensus Estimate for Potbelly's 2022 sales and EPS suggests growth of 14.1% and 90.4%, respectively, from the corresponding year-ago period's levels.

Arcos Dorados carries a Zacks Rank #2. ARCO has a long-term earnings growth of 34.4%. Shares of the company have increased 32.5% in the past year.

The Zacks Consensus Estimate for Arcos Dorados' 2022 sales and EPS suggests growth of 25.7% and 120.8%, respectively, from the year-ago period's levels.

Dollar Tree carries a Zacks Rank #2. DLTR has a trailing four-quarter earnings surprise of 13.1%, on average. The stock has gained 63% in the past year.

The Zacks Consensus Estimate for Dollar Tree's 2022 sales and EPS suggests growth of 6.7% and 40.5%, respectively, from the corresponding year-ago period's levels.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.