Closing summary

So Super Thursday came and went, and although there was still some uncertainty about when the Bank of England would raise interest rates, a move this year now seems less likely.

For the first time the Bank issued its latest inflation report and the minutes of its monetary policy committe meeting at the same time as its latest decision on rates and quantitative easing.

To no one’s surprise it left rates on hold at 0.5%, but unexpectedly the minutes showed an 8 to 1 vote in favour of no change. Traders had forecast that at least two members of the Bank’s monetary policy committee would vote for a rate rise, so this was more dovish than predicted.

So with all the signs suggesting that dearer borrowing costs could now be delayed until next year, the pound lost ground, down 0.75% against the dollar immediately after the news.

But Bank governor Mark Carney sounded a more hawkish tone in his press conference, saying the timing of the next rate rise was getting closer, and so sterling recovered some of its losses. Hence the uncertainty.

Elsewhere the Athens market closed 3.65% higher with the banking sector recovering after three days of heavy losses.

Meanwhile the International Monetary Fund said it would not decide whether to participate in a new bailout package for Greece until the autumn.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Back with Greece and talks between the Greek government and its lenders are set to continue into the weekend. Earlier the European Commission said the discussions were progressing in a satisfactory way, and there would be a teleconference on Friday to take stock of the situation.

Technical talks between Greek gov't and lenders to continue until Saturday, Finance Ministry sources have told @NikasSotiris #Greece

— Nick Malkoutzis (@NickMalkoutzis) August 6, 2015

European markets slip back

Shares ended the day on a downbeat note across Europe, with the UK market dominated by the release of the latest Bank of England rate decision and inflation report.

The pound fell from around $1.5632 to the current $1.5521 as the Bank of England hinted that although a rate rise was getting closer, it may not come this year as some had been expecting.

The closing levels on stock markets were:

- The FTSE 100 slipped 5.32 points or 0.08% to 6747.09

- Germany’s Dax dipped 0.44% to 11,585.10

- France’s Cac closed down 0.09% at 5192.11

- Italy’s FTSE MIB fell 0.42% to 23,811.09

- Spain’s Ibex ended 0.23% lower at 11,253.6

- But the Athens market added 3.65% to 666.68

On Wall Street the Dow Jones Industrial Average is currently 138 points or 0.79% lower ahead of Friday’s non-farm payroll numbers. It is now down around 5% since its recent high in May.

Updated

Hope the closing figure in Athens isn’t ominous.

Athens ASE Index closes up 3.65% to finish at 666 as bank sell-off stops http://t.co/MJlkyCF6i2 pic.twitter.com/TYFzv8rmBX

— Bloomberg Markets (@markets) August 6, 2015

Speaking of Greece, the Athens stock market has ended the day 3.65% higher.

The beleaguered banking sector moved higher for the first time since the market reopened on Monday, with the banking index rising 17.8% after falling 63% in the previous three days.

Among the individual banks, National Bank of Greece added 27% and Attica Bank rose 23%.

Over in Portugal, and the International Monetary Fund has said the country’s economic recovery remained on track but more still needs to be done.

In a report at the end of a second monitoring programme, it said:

Portugal’s economic recovery remains on track in 2015, boosted by rising exports and consumption, together with a recent upturn in investment. Real GDP expanded by 1.5 percent (year-on-year) in the first quarter, and is projected to increase 1.6 percent for the full year. Fiscal adjustment has slowed, meanwhile, with a structural loosening likely this year. Employment has declined in recent quarters, after increasing sharply from early-2013 through mid-2014, and the unemployment rate was at 13.7 percent at the end of March.

The banking system as a whole remains adequately capitalized, with decreasing reliance on Eurosystem financing, but loan performance has continued to deteriorate. Non-performing loans increased to 12.3 percent at the end of March, putting further pressure on already weak profitability as banks absorb large impairment expenses and high operating costs.

Recent market volatility related to Greece has had limited impact on Portugal, reflecting the country’s improving fundamentals in addition to the overall supportive external environment. Portugal has benefitted from favorable commodity prices, low interest rates and a weaker euro. Growth is projected to moderate over the medium term, however, as these supportive cyclical factors weaken and still high public and private debt constrain the pace of recovery.

But it added:

With increased financial market volatility in the context of developments in Greece, it is crucial to ensure that investors retain confidence in the direction of economic policies. The authorities have made progress in improving the profile of public debt, but medium-term financing needs remain large, and rising bond market volatility implies significant risks around the baseline financing plan. The authorities should continue to retain a large cash buffer in order to maintain flexibility in implementing their borrowing program.

Further fiscal adjustment is needed to further reduce vulnerabilities from high public debt, particularly given the increased risk of financial market turbulence.

More decisive steps to improve banks’ balance sheets are desirable. Weak profitability provides little cushion for banks to absorb further losses, in the context of still-rising non-performing loans. More concerted efforts are needed to reduce operating costs in order to improve financial performance and accelerate the process of balance sheet repair; banks should not rely on economic growth alone to mend their balance sheets.

It will be essential to regain momentum on structural reforms when a newly elected government is formed. The current economic recovery and beginning of a new political cycle presents a favorable opportunity to press ahead with reforms, particularly in the areas of labor market and public sector reform. Moving forward, it is critical to ensure that product market reforms introduced in recent years are fully implemented as intended, to achieve tangible results on the ground. It will also be important to ensure that the difficult reforms that have been undertaken, such as to contain the rise in energy costs, are not reversed.

UK economy grew by 0.7% in three months to July - NIESR

The UK economy grew by 0.7% in the three months to July, according to the latest estimates from the National Institute of Economic Research. It said:

Our monthly estimates of GDP suggest that output grew by 0.7% in the three months ending in July after growth of 0.7% in the three months ending in June 2015. Compared to the same three month period in 2014, this implies a year-on-year growth rate of 2.7%. This is consistent with our recently released quarterly forecast in which we expect an average rate of growth of 2.5% for 2015 as a whole.

Updated

The Bank of England’s torrent of documents has not really helped clarify its thinking, says Guardian financial editor Nils Pratley:

“Super Thursday” didn’t quite live up to the grand billing. The moment of the first hike in interest rates is getting closer, said the Bank of England governor, Mark Carney, but it is also clear that this song could remain the same for some time. Only one member of the monetary policy committee, not the expected two, voted for a rate hike. It is now highly unlikely that interest rates will rise this year.

Despite Carney’s many references to “robust momentum” in the economy, next May is viewed by financial markets as the most likely moment the Bank increases the cost of borrowing...

The other question here is whether the slew of simultaneous-released documents – a rate decision, the supporting minutes, and a quarterly inflation report – actually improves the market’s understanding. That, after all, is meant to be the point of Super Thursday – less noise, and less confusing signals. A proper judgment is impossible on day one. But one can’t say on Thursday that the new era of greater transparency has aided understanding. We still have a Bank governor who sounds increasingly hawkish on rates – but lacks a cast-iron case for moving soon.

The timing of the decision on when to move rates will move into “sharper relief” around the turn of the year, Carney repeated on Thursday. Well, it might. But it’s also possible that the real world – a blow-up in Greece, a steeper slowdown in China or more wobbly unemployment data – intervenes.

The full comment is here:

Updated

Here’s a graph showing sterling’s performance against the dollar so far today. As the Bank’s statements were released it fell sharply, since the comments were more dovish that expected and only one member of the monetary policy committee voted for a rate rise.

But with governor Mark Carney showing a more hawkish tone during the press conference, the pound has regained some of its lost ground:

52 mentions of sterling in BoE Inflation Report today vs 42 in May's.

— Jamie McGeever (@ReutersJamie) August 6, 2015

68 mentions of "productivity" in today's BoE Inflation Report vs 84 in May's. 39 mentions of "slack" today vs 75 in May.

— Jamie McGeever (@ReutersJamie) August 6, 2015

Updated

Foreign exchange business Foenix Partners reckons the Bank’s statements and press conference have not really made things any clearer. Managing director Richard de Meo, said:

Just one voting member in favour of a rate hike within the MPC delivered a conflicted message during today’s unprecedented Bank of England session, with Carney’s press conference leaving currency and fixed income traders little clearer on the timings of policy action.

The new meeting structure strives for transparency, yet efforts to get markets on side included generic and at times cryptic comments, with the overall tone very mixed: an upbeat assessment of UK growth and productivity, a dismissal of the impact of sterling strength, and then obvious caution around employment growth and the inflation outlook. With wording borrowed from Janet Yellen, the “data-dependant” stance ensures heighted scrutiny of inflation data, despite the likelihood of upcoming negative readings.

We see the range of timings for the first rate hike unchanged, to occur between October and February 2016, with the only major adjustment to the house view being that Carney is no longer boring.

Updated

Nordic bank SEB also expects the first UK rate rise to be delayed until February next year. Economist Mattias Bruér said:

While the UK economy has momentum, there is no CPI inflation at all which is an argument against rate hikes...With respect to annual inflation averages, the Bank of England forecast that inflation will only average 0.3% in 2015 compared to 0.6% in May and increasing to 1.5% in 2016. As such, the outlook for inflation is not suggesting that rate hikes are imminent and does not change our view of a February 2016 lift-off.

“Dovish surprise, but not a dovish report” – says Alan Clarke at Scotiabank.

While the minutes of the August MPC meeting showed that one member voted for an immediate rate hike, expectations had been for two dissents and possibly more. As such, this represents a baby step closer to a rate hike rather than a stride. There was a grudging downward revision to the inflation projection – down two years ahead from 2.08% y/y to 2.03% y/y.

In the context of monetary policy, a rate hike before the end of the year is still possible, but it would require some positive surprises on the data front. Meanwhile, a hike in early-2016 seems more likely unless the data disappoints substantially.”

James Knightley, UK economist at ING, and others reckon the tone of Carney’s comments was a bit more hawkish than the earlier triple release.

Mark Carney clarified the much quoted “the decision as to when to start that process of raising interest rates will likely come into sharper relief around the turn of this year” he used on July 21st. He said that he was speaking from a personal perspective and was not reflecting the general view of the MPC, which implies he is on the more hawkish end of the spectrum of views within the committee.

Other than that, the tone is perhaps marginally more hawkish than the triple whammy of announcement, minutes and inflation report. Lots of emphasis on the tightening labour market and the implications for wages. Carney also suggests that the strength of the pound is doing some of the work to tighten monetary conditions, but there is uncertainty as to how much this will feed through into lower CPI [inflation]. Moreover, the needs of rate hikes over the coming year reflects domestic inflation pressures and the decision to hike will, of course, be data dependent.

To recap our view. We look for a 25bp hike in February 2016, to be followed by two more in mid-2016 leaving Bank Rate at 1.25% for end 2016. We think that wage growth will continue to edge higher as companies increasingly worry about staff retention and the central bank will respond to the threat this poses for CPI missing its target over the medium term. Nonetheless, policy tightening will be slow and gradual reflecting high debt levels and the currency implications feeding back into CPI. Brexit concerns as the vote approaches on the UK’s ongoing membership of the EU and its implications for consumer and business confidence and spending will also likely lead to caution from the BoE.

Carney @bankofengland: the market's path for rates "does not deliver a sustainable return of inflation to target": hawkish

— Heather Stewart (@heatherstewart3) August 6, 2015

Updated

The press conference is over. Towards the end Carney reiterated the MPC’s plan not to unwind quantitative easing by selling off gilts until rates start to rise, saying

We want to use interest rates as the marginal instrument of monetary policy.”

Carney says there would probably have to be "material" rises in interest rates before Bank would contemplate sales of £375bn of QE gov debt

— Robert Peston (@Peston) August 6, 2015

Updated

Here are Carney’s earlier comments on sterling in full:

There’s no question the persistent strength of sterling is having an influence on policy, and it’s one of the factors, but it has to persist. We will take it into account. But even taking it into account... we see robust private sector growth here and consistent with that is a need to begin to increase interest rates. Sterling hasn’t taken away that requirement.”

The pound has recouped some of its earlier losses and is now trading at $1.5526, down 0.46% on the day.

Updated

The TUC, on the other hand, has applauded the Bank for keeping borrowing costs unchanged.

TUC assistant general secretary Paul Nowak said:

The Bank is right to keep rates on hold and recognise the ongoing risks to our weak economic recovery.

Given the chancellor’s plans for severe spending cuts, putting interest rates up too soon would hit growth hard, choking off recent gains in employment and earnings for working-age people.”

Ranko Berich, head of market analysis at foreign exchange specialist Monex Europe, says:

Today’s releases from the Bank of England were not so super after all, as caution still reigns supreme at the Bank of England. This is the same old ultra-cautious Bank of England we’ve had for years, and yet today’s releases came as a surprise.

Although the inflation report is still being picked apart, sterling is being sold off across the board and gilt yields are going down, suggesting that the markets were expecting a far more hawkish set of minutes.

Now the MPC, along with the markets, will be watching wage growth data even more intently. Should the spike recently seen in wages extend over the coming months, the balance of votes could quickly swing in favour of hikes. For now however, the core dynamic that has kept the Bank in wait-and-see mode for years remains very much in play, as uncertainty around labour market slack and a murky international outlook keep the majority of the MPC on the dovish side.”

Carney has reiterated that the Bank is “mildly encouraged” by the recent pick-up in UK productivity. But, he added

We haven’t run to the other side of the boat as a consequence of a few good reports. We have taken about half of that improvement in productivity into the forecasts.”

Updated

Carney highlighted the UK’s current account deficit as a major risk to financial stability.

Sterling. A major headache for Bank of England and fast becoming the key reason it won't - can't - raise rates. pic.twitter.com/H0qteTQxOx

— Jamie McGeever (@ReutersJamie) August 6, 2015

Bank of England keeps interest rates on hold, but its forecasts are based on slightly faster rises in rates next year than expected in May

— Robert Peston (@Peston) August 6, 2015

Why on earth is Bank of England mooting interest-rate rise when unemployment is rising slightly & inflation is zero? http://t.co/XlRvuFtQ5N

— Robert Peston (@Peston) August 6, 2015

The Bank’s deputy governor Ben Broadbent added that the economic recovery is driven as much by business investment as consumer spending.

Carney said:

This is not a debt fuelled consumer recovery... Households are consuming out of income [rather than savings].

There is absolutely a sustainability to that aspect of the recovery particularly as productivity starts to fill in.

Mark Carney @bankofengland: "There's no question that the persistent strength of sterling is having an influence on policy".

— Heather Stewart (@heatherstewart3) August 6, 2015

Updated

You can watch the press conference live here.

The Bank of England governor denied suggestions that he said in a speech in July that borrowing costs would rise around the turn of the year. He said he was speaking in a personal capacity, rather than representing the MPC as a whole.

The central bank has kept its base rate at a record low of 0.5% for more than six years, after slashing rates at the height of the global financial crisis like other central banks around the world.

Updated

In response to a question from the Guardian’s Heather Stewart about how the stock market crash in China and the Greek crisis have influenced the MPC’s rate decision, Carney said:

These were not factors that were weighing on the committee’s decision in any form”

except in terms of how they impacted on the economic fundamentals.

He said the “situation in Greece was a steady feed of news about an important situation” and it showed that

some of the defences that had been put in place by the European authorities were holding.

Events in China are important, but they’re important first and foremost from a perspective of global demand.

The financial links to China are nowhere near as strong as the scale of that economy would suggest.

China is the world’s second-largest economy.

Updated

Carney: timing of first rate rise 'drawing closer'

Carney said the Bank will be closely monitoring economic developments, in particular wage growth, productivity, core inflation, import prices and risks to the international environment.

He stressed that interest rate increases will be “gradual and limited,” adding that the “path is more important than the likely timing of the first increase”.

The likely timing of the first bank rate increase is drawing closer. However the exact timing of the first move cannot be predicted in advance. It will be the product of economic developments and prospects. In short it will be data dependent.”

Mark Carney @bankofengland "the exact timing of the first move [in rates] cannot be predicted in advance": will be "data dependent".

— Heather Stewart (@heatherstewart3) August 6, 2015

Carney @bankofengland Near-term inflation outlook "muted"; but "little evidence of a deflationary mindset" among consumers or businesses.

— Heather Stewart (@heatherstewart3) August 6, 2015

Carney: despite strong global demand, "exports will still be held back by the strength of sterling".

— Heather Stewart (@heatherstewart3) August 6, 2015

Updated

Set against that, UK private domestic demand has been robust and is expected to remain so, the Bank’s governor said. Demand growth can return inflation to its 2% target within two years.

Updated

Carney said the most striking development in the UK over the past year has been the fall in inflation, which hit zero in June.

Updated

The press conference is under way: Bank of England governor Mark Carney is reading out the opening statement.

The FTSE 100 index has turned positive: it is now trading nearly 7 points higher at 6759.25, a 0.1% gain. Before the Bank of England’s release, it was drifting lower, trading down nearly 0.4%.

Housebuilding and property shares have been lifted as the prospects of an interest rate rise before the end of the year receded after the Bank’s reports.

Taylor Wimpey is up 3%, while Persimmon, Barratt Developments and Bovis Homes are all up nearly 2%. Property website Zoopla has risen nearly 1%, as has estate agency Countrywide.

Updated

The British Chambers of Commerce warned that a “premature” rate hike could derail Britain’s economic recovery.

John Longworth, the group’s director general, said:

The MPC has shown composure and sound judgement in keeping rates unchanged. It would have been imprudent to push through a rate rise at this moment when our economic recovery remains in need of care and encouragement. Rates will eventually have to rise and when they do it should be done slowly and steadily. Until that moment, the Bank of England is right to keep interest rates at current levels.”

David Kern, the BCC’s chief economist, added:

Those who advocate higher interest rates, underestimate the fragility of the economic recovery, especially in the face of a highly uncertain international backdrop.

The MPC will be watching increases in earnings closely. But any adverse inflationary pressures will be mitigated by the declines in oil and commodity prices and by the strength of sterling seen over recent months. Our view remains that inflation will remain below the 2% target until well into 2016. That being the case, the MPC should keep interest rates at current levels for the foreseeable future and, in doing so, it will not take any undue risks.”

Sterling falls 0.75% after BOE's triple release

Sterling has fallen by 0.75% to $1.5484 after the minutes of the Bank of England’s rate-setting committee meeting showed only one member (out of 9) voted for a rate rise this month. Most of the members thought that inflation will rise more slowly than previously thought, due to lower oil prices and a rise in the value of sterling in recent months.

The minutes said:

For most members, the outlook for inflation described in the August Inflation Report meant that it was not necessary to change the policy stance at this meeting. In light of the reduction in oil prices and appreciation of sterling over the past three months, it appeared that the increase in inflation over the following year would be more gradual than had previously been supposed.”

At the same time, UK economic growth is now expected to be slightly stronger than previously thought, at 0.7% in the third quarter, and 2.6% for this year as a whole, against a 2.5% forecast in May, as cheap energy costs and rising wages underpin consumer spending.

Updated

James Knightley, UK economist at ING, has taken a closer look at the BOE releases. We are now waiting for the press conference from governor Mark Carney who will provide more colour on the MPC’s thinking… it is due to start at 12:45 UK time

The minutes showed that the Bank is concerned about the effects of sterling strength weighing on inflation, but that these were offset by rising wage pressures, which “surprised significantly to the upside over the past quarter”. Consequently, “some members saw upside risks to the inflation forecast”, citing stronger demand, less spare capacity in the economy and higher wages. For McCafferty, these risks were sufficient to justify tighter policy.

We also get the Inflation Report, which shows that in the collective judgement of the Bank inflation will be fractionally above 2% in 2 and 3 years’ time (2.03% and 2.14% respectively) based on market expectations for Bank Rate of 0.9% in 3Q 16 and 1.7% in 3Q18. The near term inflation profile is lower than what they had predicted three months ago, reflecting stronger sterling, but then the higher wage story leads to inflation pushing back to 2%.

All in all this is perhaps a slightly more dovish combination that the market was probably anticipating. Nonetheless, it doesn’t lead us to alter our view that the first rate hike is most likely to come in 1Q15. Two weeks ago Mark Carney had suggested “the decision as to when to start that process of raising interest rates will likely come into sharper relief around the turn of this year”. November seems too early to us given that the annual rate of inflation will still be well below 1% at that time and it may create presentational difficulties for the BoE in justifying tighter monetary policy to the broader public.

We also expect the political noise in Europe to become louder given the December Spanish elections and the likelihood that Greece/EU tensions will be rising after a summer lull. With headline YoY inflation likely to rise reasonably swiftly in early 2016 as the sterling/energy effects fade from the annual comparison of prices, we favour February as the start point for the tightening cycle.”

Peter Cameron, of EdenTree Investment Management says:

Amongst today’s deluge of data, perhaps the most significant piece of information – while just from one member - is the widely anticipated MPC split over rate hikes. For the first time in 2015, the committee is divided. While the dissenter remains in the minority, today’s results are yet another nod that the first hike could be just around the corner, after six years of record low rates.

The waters have been muddied of late - on the one hand oil prices are falling again, but countering that is stronger than expected wage growth. These conflicting inflation trends are adding an extra layer of complexity to the rates outlook, but today’s vote count indicates an incrementally more hawkish stance by the Committee as we approach the end of the year.”

Some instant reaction from Samuel Tombs, senior UK Economist at Capital Economics, who says the triple release of rate decision, minutes and inflation report suggests a rate hike this year is still unlikely.

Today’s ‘Super Thursday’ releases from the UK Monetary Policy Committee suggest that an interest rate rise is still not imminent. Contrary to widespread expectations of a 7-2 split, only Ian McCafferty broke ranks and voted for a rate rise. And the Committee revised down its forecast for CPI inflation over the next twelve months and still expects it to only just return to the 2% target at the two year policy horizon. This suggests that most MPC members see the market expectations on which the forecast is based – for interest rates to start rising in spring 2016 – as broadly correct.

It would not be surprising if one or two more MPC members joined Ian McCafferty in the coming months – the minutes emphasised that “some members” saw upside risks to the inflation forecast. But we doubt that rates will rise until the Governor changes his view – note that interest rates have never risen without the Governor voting to hike. And in his speech last month, Mark Carney stated that he wanted to see core inflation and growth in unit wage costs pick up before voting to raise rates. The recent strengthening of the pound and rebound in productivity suggest that those pick-ups are unlikely to be seen in the data for some time. So while the Governor’s previous capriciousness means that a 2015 hike cannot be entirely ruled out, today’s releases support our view that a majority will vote to keep interest rates on hold until the second quarter of next year.”

Here is a quick first take on the Bank of England’s Super Thursday, from Heather Stewart on our economics desk, who is at the Bank of England in Threadneedle Street.

MPC voted 8-1 for unchanged interest rates, with Ian McCafferty the sole hawk. Is Carney's "turn of the year" timetable looking stretched?

— Heather Stewart (@heatherstewart3) August 6, 2015

So, is Carney going to come out guns blazing at the press conference?

— Jo Michell (@jomicheII) August 6, 2015

Shorter BoE Inflation Report: "Um, not sure, more of the same, probably? We'll hit the target in the medium term." pic.twitter.com/MffhKXfbLS

— Jo Michell (@jomicheII) August 6, 2015

Updated

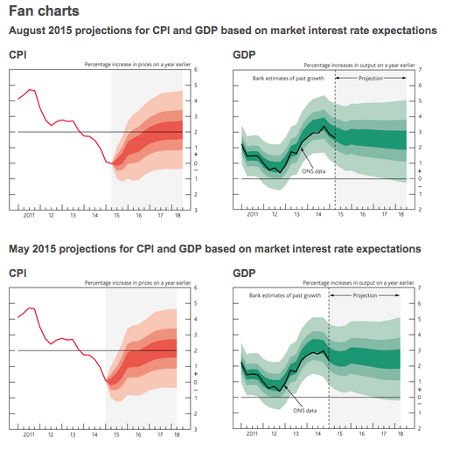

Here are the famous fan charts which illustrate the Bank of England’s latest growth and inflation forecasts. The Bank downgraded its near-term forecasts for inflation, after a renewed drop in global oil prices, which are below $50 a barrel.

Updated

Sterling continues to fall and is now down 0.67% on the day, to $1.5491.

Updated

Here is a link to the Bank of England’s rate decision.

You can find its quarterly inflation report here.

Updated

City economists had expected two or even three members of the monetary policy committee to back a rate rise this month.

Minutes of the meeting, which were for the first time published at the same time as the the monthly monetary policy decision, said:

The near-term outlook for inflation is muted. The falls in energy prices of the past few months will continue to bear down on inflation at least until the middle of next year.

The Bank now expects inflation to remain at around zero for at least the next two months, before rising to its 2% target at the end of the monetary policy committee’s two-year forecast period, if interest rates are increased in line with the market’s expectations.

That would imply the first rate rise coming in mid-2016, with borrowing costs climbing to 1.5% by the end of 2017, my colleague Heather Stewart reports.

Bank of England votes 8-1 to keep rates at 0.5%

Bank of England policy makers voted 8-1 to keep interest rates unchanged.

Ian McCafferty was the lone dissenter, who backed a quarter-point rate hike to take the base rate to 0.75%.

This came as a surprise to financial markets. The pound dipped to $1.552, from $1.5610 just before the announcement.

Updated

The triple release from the Bank of England is now just over half an hour away.

Updated

Main European stock markets slip; Athens rises 3.2%

On markets, Brent crude has dipped back below $50 a barrel, although it is up 0.1% on the day, amid a supply glut. New York light crude has slipped 0.5% at $44.92 a barrel.

Carsten Fritsch, an oil analyst at Commerzbank, said:

Prices are likely to consolidate or weaken further. The perception is that over-supply will be there for much longer.”

European stock markets are slightly down. Athens is the exception, up 3.2% after heavy losses in the last three days. Some banking shares have bounced back (National Bank of Greece and Attica) while others are still deep in the red (Alpha Bank, Piraeus Bank).

UK’s FTSE 100 index down 0.45% at 6721.85

Germany’s Dax down 0.1% at 1625

France’s CAC down 0.15% at 5188.95

Italy’s FTSE MiB down 0.3% at 23842.43

Spain’s Ibex down 0.07% at 11271.3

Updated

Returning to the Bank of England’s Super Thursday, which kicks off at midday, Keith Froud, partner and markets expert at law firm Eversheds, said:

Concerns around data overload every Super Thursday seem somewhat overstated. The reality is, we now live in a world of instant information. Whilst the intrigue of the MPC minutes will doubtlessly draw its usual attention, one would hope that the market is sophisticated enough to extract the relevant data and sentiment from each of the information sources.”

Greek unemployment falls to 3-year low of 25%

Encouragingly, Greece’s unemployment rate has fallen: to 25% in May from 25.6% the previous month, marking the lowest reading since June 2012, according to statistics agency ELSTAT.

Unemployment has come down from record highs of 27.9% in September 2013 as the economy stabilised last year – but is still more than double the average rate of 11.1% in the eurozone. However, Greece’s economy shrank by 0.2% in the first quarter.

No IMF decision on Greek bailout until autumn, Swedish rep tells paper

Finally, some news on Greece: the International Monetary Fund will not decide whether to participate in a new bailout package for Greece until the autumn, Sweden’s representative to the fund’s executive board told a newspaper.

There is “strong” support at the IMF for joining the third bailout (which could total some €86bn), said Thomas Östros, a director on the fund’s 24-member board – “but it will take time”.

He told Swedish daily Dagens Nyheter:

There is going to be a discussion during the summer and autumn and then the board will make a decision during the autumn.”

He also noted that Greece must adopt wide-ranging reforms first.

It cannot be something that is forced on them [Greece]. Greece must own the problem. The Greek government is not there yet.

They have an inefficient public sector, corruption is a relatively big problem and the pension system is more expensive than other countries.”

House prices in the UK dipped 0.6% in July following a surprise jump of 1.6% in June, according to the Halifax. The annual rate of house price inflation retreated to 7.9% in the three months to July, the lowest since the three months to December 2014, after hitting 9.6% in the three months to June.

Howard Archer, chief UK and European economist at IHS Global Insight, said:

The Halifax data have been notably more volatile than other house price measures in recent months and stronger overall than most. Indeed, despite July’s retreat, annual house price inflation on the Halifax’s measure at 7.9% in the three months to July is still more than double the Nationwide’s rate of 3.5% in July.

This highlights the need to not pin too much weight on one particular house price survey or measure, but to try and take an overall view from the data.”

Other UK data this morning showed British new car sales rose by 3.2% in July year-on-year, with small family cars and super-mini models particularly popular. The Society of Motor Manufacturers and Traders said 178,420 new vehicles were registered.

The industry body forecasts that new car sales will rise nearly 4% this year from last year, hitting 2.57m thanks to a mix of cheap credit and improving confidence among consumers. However, the slower pace of growth in July compared to previous months suggests demand will level off in coming months, after a bumper first half of the year, the SMMT said.

Economists at Royal Bank of Scotland have produced this interesting chart that shows all 15 OECD countries which hiked interest rates since the financial crisis in 2008 have since reversed their decisions.

Raising rates is hard to do. All 15 OECD countries who hiked since 2008 have now reversed #SuperThursday pic.twitter.com/nf2jPurEy9

— RBS Economics (@RBS_Economics) August 6, 2015

British industrial output falls unexpectedly on oil, gas, mining

Britain’s industrial output unexpectedly fell in June as the oil and gas and mining sectors cut back. Official figures showed industrial production dropped 0.4%, disappointing economists who had pencilled in a 0.1% rise, and following a 0.3% increase in May.

Manufacturers, however, increased production by 0.2%, following a 0.6% decline in May.

The Office for National Statistics said oil and gas production fell by 5.8%, the biggest monthly drop since January 2014, partly due to maintenance in a major oil field.

Paul Hollingsworth, UK economist at Capital Economics, said:

June’s industrial production figures highlight that the strong pound and weak overseas demand held back the manufacturing sector’s recovery in the second quarter.

Given that the oil price has fallen by 19% since the end of Q2, it looks unlikely that oil and gas extraction will make another punchy contribution to overall production in Q3. What’s more, with the pound having risen further recently and overseas demand still weak, it is doubtful the manufacturing sector will pick up the slack. Indeed, business surveys such as this week’s Markit/CIPS PMI suggest that the sector saw continued contraction at the start of Q3.

Thankfully, however, the services sector is still performing strongly, so we expect the economic recovery to maintain a healthy degree of momentum over the rest of this year and forecast GDP to rise by 2.7% or so.”

Pfizer under fire from competition watchdog over epilepsy drug

Pfizer has come under fire from Britain’s competition watchdog, which said the US company breached UK and EU competition law by ramping up the cost of an epilepsy drug that is used by more than 50,000 British patients.

The Competition and Markets Authority said its provisional view was that Pfizer, which makes Epanutin capsules, and Flynn Pharma, which distributes the drug, abused their dominant position by charging “excessive and unfair” prices.

Pfizer – which made an unsuccessful, hugely controversial takeover bid for Britain’s AstraZeneca last year – said it was cooperating fully with the CMA and noted that the watchdog had not yet made a final ruling.

You can read the CMA’s statement in full here.

Athens stock market rises 0.9%; banking shares recover

The Athens stock exchange has opened higher, bringing some relief after three days of losses. Banking shares took a further tumble but are now now up, mostly.

The Greek market has gained 0.9%. The banking sector index, which lost 63% in the past three days, fell a further 7.8% before recovering and is now trading 2.8% higher.

The country’s biggest bank, National Bank of Greece, has bounced back 14% while Attica Bank is 19% ahead. By contrast, Alpha Bank is down nearly 17% and Piraeus Bank has lost 11.6%.

The pound has climbed 0.15% to $1.5628 this morning and is trading at 69.75p against the euro, close to a two-week high, amid expectations that UK interest rates will go up soon from their record low of 0.5%. The Bank of England’s triple data release from midday will set out the central bank’s thinking on the state of the economy.

German factory orders rise sharply

German industrial orders have come in much stronger than expected thanks to strong demand from abroad.

Contracts for German goods rose 2% in June, Germany’s economy ministry said, versus expectations of of a 0.2% gain. German factories received 4.8% more orders from abroad, while domestic orders fell 2%.

RSA boss chipper as insurer beats forecasts while suitor Zurich disappoints

In the insurance world, RSA boss Stephen Hester said the ball is in Zurich’s court as far as its potential bid for the UK insurer is concerned.

RSA, which owns the More Than brand, reported better than expected half-year results, which contrasted with the disappointing numbers released by its Swiss suitor Zurich on Thursday. Europe’s third-largest insurer said last week that it was considering making a bid for RSA but is yet to put a formal offer on the table. The news sent shares in RSA up 18% to 518p, and they maintained this level until Thursday.

Shares in Zurich fell nearly 4% in early trading. The Swiss company’s comments that it won’t overpay for RSA sent the UK insurer’s shares down 1.3% to 517p.

Analysts think a bid will come in at about 550p a share, valuing RSA at £5.5bn. The Daily Telegraph reported that Zurich could be planning to lower its bid to about 525p a share.

Panmure Gordon analyst Barrie Cornes says:

Whilst we think that an offer by Zurich is likely, given comments by Zurich today that any offer would have to meet its investment hurdle rates, we believe that it would be prudent to tactically ‘take some money off the table’ in case a deal is not agreed.”

You can read the full story here.

Another big insurance company, Aviva, which bought Friends Life in the spring, beat City forecasts with half-year profits. Chief executive Mark Wilson said the company is now in a “transforming and growing phase”.

The news sent the shares 1.3% higher to 534.3p, making Aviva one of the top gainers on the FTSE 100 index.

Updated

We have done a Q&A that helps explain why Super Thursday is important.

Updated

Both the US Federal Reserve and the Bank of England are on the cusp of raising interest rates for the first time in almost a decade, and the Fed is widely expected to go first, possibly in September.

Another thing to look out for on Super Thursday are the Bank’s famous fan charts on the inflation and GDP growth outlook two years out. Inflation, which has dipped to zero, has been well below the Bank’s 2% target for some time.

You could be forgiven for being a bit puzzled: why should rates go up when there’s no inflation? The argument has been that low inflation is temporary and that is has been artificially depressed by the crash in energy and raw materials prices late last year. But it now looks as though low headline inflation could persist for some time.

However, both the Fed and the Bank of England are eager to ‘normalise’ interest rates, as the economic recovery gathers steam. The Bank will point to the outlook for inflation two years out. Inflation expectations have risen among households and in financial markets and are above the 2% target further out.

As usual, the tone of Carney’s comments at the press conference will be just as important as the voting outcome of the policy meeting. Analysts at Capital Economics say the Bank’s governor may steal the hawks’ limelight on Super Thursday:

Although another no-change decision is likely, we expect the minutes to reveal that at least two of the nine Committee members have begun to vote to raise rates. The minutes of July’s meeting showed that a number of members thought that the risk that CPI inflation would overshoot its 2% target in the medium term was growing and suggested that only the Greek crisis was holding them back from switching their votes. Last week’s news that GDP growth sped up from 0.4% in Q1 to 0.7% in Q2 is likely to have reinforced these members’ concerns about the medium-term inflation outlook.

We would, however, caution against placing much weight on the minutes until the governor has commented at the subsequent Inflation Report press conference at 12.45 BST. While he is just one member among nine, governors have rarely been outvoted in the past and internal members of the MPC often take their steer from him. And we think that he is likely to sound quite dovish again.

In his speech last month, the Governor outlined three developments that he would like to see before raising rates – above trend GDP growth, a pick-up in core inflation and stronger growth in unit wage costs. The last two criteria have not been met yet and we doubt they will before the end of the year. The recent appreciation of sterling is likely to keep core inflation below 1% until next year. Meanwhile, wage growth has picked up, but it has still not recovered to rates that would push annual growth in unit wage costs back towards 2% since productivity growth has also risen.

Accordingly, we think that markets are right to think that there is less than a 50% chance of a rate rise this year. Indeed, since CPI inflation is likely to remain below 1% until the spring, we concur with the markets that the first rate rise is not likely to come until the second quarter of next year.

Updated

Angus Campbell, senior analyst at UK online broker FxPro, thinks the ‘data dump’ could lead to more volatility for the pound.

Today is likely to mark the first steps towards the commencement of the interest rate tightening cycle for the Bank of England. The markets can rest assured there won’t be any rate hike at this meeting and in the past we would not know how the MPC had voted for another two weeks, but going forward those minutes and voting patterns will be released along with the decision.

Whilst the premise of this change to the BOE’s procedures may have good intentions, it could lead to greater short term volatility both over the release and after it, before investors have enough time to absorb all the information and get a better understanding of what the BOE’s thinking is. Throw into the mix the Inflation Report and sterling could see considerable volatility. This morning sterling is a little higher against the dollar at $1.5635.

But today’s meeting could be academic as the BOE is highly unlikely to move before the US’s Federal Reserve. Whilst it will be important to see the latest two year inflation projections and decipher whether Mr Carney is edging towards a move hawkish stance, really the bigger question remains if the FOMC will move in September, November or December, with the market pricing in a higher chance of a September rate hike following hawkish comments from Fed voting member Lockhart earlier in the week.”

Investors continue to expect the U.S. Federal Reserve to raise rates before the Bank of England. (via BBG) pic.twitter.com/qxaiD8DxUJ

— Holger Zschaepitz (@Schuldensuehner) August 6, 2015

Updated

Super Thursday: Bank of England transparency or information overload? asks the Guardian’s economics editor Larry Elliott.

Instead of the previous drip-feed of information, there is now going to be a data dump... This looks suspiciously like a super-charged version of forward guidance, the big initiative of Mark Carney when he became the Bank’s governor two years ago. Forward guidance proved to be a bit of a dud, not because of the way it was communicated but because of the Bank’s inability to forecast the economy accurately.”

Updated

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Super Thursday has arrived – the day when we get three big releases from the Bank of England that will shed light on its thinking on the state of the economy. For the first time in its 321-year history, the central bank will announce its monthly decision on interest rates, publish the minutes of its policy meeting where the decision was made, and present the quarterly inflation report at the same time.

The idea is that bundling everything together will make the Bank’s decision-making process more transparent and predictable, helping households and businesses to plan ahead.

The Bank of England releases are due at noon, and governor Mark Carney will hold a press conference to explain the Bank’s policy stance at 12.45 BST.

While we aren’t expecting any change to rates from the Bank today, we will get the minutes of the meeting immediately, rather than having to wait two weeks for the voting outcome and details of the discussions.

Markets are expecting a shift from the 9-0 unanimity seen on the monetary policy committee since the start of this year, with at least two members (Martin Weale and Ian McCafferty, who both supported higher rates last year) likely to call for a small rise in the base rate. It is possible that a third member, for example David Miles, may join the hawkish camp. This should give a further boost to the pound, which has been strengthening lately on mounting expectations of a rate hike.

Michael Hewson, chief market analyst at CMC Markets UK, asks:

Will governor Carney be as adept at managing market expectations about the potential glide path of rates, as ECB President Mario Draghi has proved to be in his tenure as head of the ECB, or will he live up to his moniker as the “unreliable boyfriend?”

Updated