Over in Greece bankers are saying that the quick formation of a new government will almost certainly lead to the relaxation of debilitating capital controls. Helena Smith reports from Athens:

Since the imposition of capital controls at the end of June, business activity has been brought almost to a grinding halt. Unable to pay suppliers, small and medium sized companies have been hardest hit with exports and imports not only severely curtailed but further exacerbating the country’s economic tailspin. Bank figures show that cash-starved smaller companies have often been forced to make more frequent imports at higher prices – the only way of circumventing the demand of suppliers overseas for large sums up front for merchandise

But bankers are now saying restrictions are likely to be further relaxed – bank transactions abroad were relaxed earlier this month - if Greece moves fast to regain the trust it lost with its European partners (during fraught negotiations over its latest bailout) by forming a reform-minded government after Sunday’s elections. Six months of wrangling with creditors saw a bank run of around €40bn.

“Once banks are recapitalized and deposits flow back, that will lessen dependence on the European Central Bank and make further lifting of the controls easier,’ said one banker. Withdrawals from ATMs – now controlled at €420 a week – may be among the restrictions to be lifted.

But insiders cautioned against speculation that the controls would be entirely removed. “A lot will rest on the type of government that is put in place but even if it is ultimately a government of technocrats, restrictions will be with us for some time yet,” said the banker speaking on condition of anonymity. “Our big fear, central to the controls right now, is the outflow of deposits. Everyone worries that if we lift them altogether people will rush to take whatever they have out with everything that means for a system that is already fragile.”

On that note it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Updated

Grexit "never for real" - ECB vice president

The prospect of a Greek exit from the euro was “never for real”, according to Vítor Constâncio, vice-president of the European Central Bank in an interview this week with Thomson Reuters. Here is the relevant passage. Constâncio said:

We have growth again. We need to strengthen the confidence in peripheral countries. That has to be achieved by deepening integration. The Greek turmoil raised doubts. These doubts have to be now closed by additional institutional reforms.

Q. What doubts were raised about the euro?

It raised doubts for the markets that countries like Greece could cope with the challenges of monetary union. There was never any doubt among the majority of member countries. We maintain that the euro is irreversible. Legally, no country can be expelled. The actual prospect of that happening was never for real.

One #ECB, two words Coeure (June): #Grexit "can unfortunately no longer be ruled out" Constancio (September): #Grexit "was never for real"

— Maxime Sbaihi (@MxSba) September 16, 2015

Updated

European markets jump ahead of Fed meeting

Despite the continuing uncertainty about whether or not the Federal Reserve will raise rates on Thursday, investors were in fairly buoyant mood. The betting seems to be coming down on the side of no move - just about. Meanwhile news of a possible merger between drinks groups SABMiller and Anheuser-Busch InBev saw both companies share prices soar and give a lift to stock markets, notably the FTSE 100. Energy companies were also in demand as crude prices moved higher after an unexpected fall in weekly US inventory data. The final scores showed:

- The FTSE 100 jumped 91.61 points or 1.49% to 6229.21

- Germany’s Dax added 0.38% to 10,227.21

- France’s Cac climbed 1.67% to 4645.84

- Italy’s FTSE MIB rose 0.71% to 22,059.21

- Spain’s Ibex ended 1.99% higher at 9976.8

- In Greece, the Athens market added 1.51% to 692.44

On Wall Street, the Dow Jones Industrial Average is currently 92 points or 0.56% higher.

Thursday’s Federal Reserve decision on interest rates is still too close to call, according to the latest Reuters poll. But the pendulum has swung slightly in favour of the central bank keeping borrowing costs on hold:

45 of 80 economists now calling no Fed move vs slight majority last wk for a hike. Nobody switched to predict a rise https://t.co/9KTGVjgbrX

— Ross Finley (@rossfinley) September 16, 2015

Oil surges after US stocks data

Oil prices are surging after an unexpected fall in US crude stocks last week.

Crude inventories fell by 2.1m barrels, according to the Energy Information Administration, compared to expectations of a rise of 1.2m barrels.

The news has sent Brent crude nearly 5% higher to $50.10 a barrel, with West Texas also on the rise:

Oil now surging 6% http://t.co/U3FGscb0V7 pic.twitter.com/j1b0vi0HCy

— Joseph Weisenthal (@TheStalwart) September 16, 2015

Bank governor Mark Carney said that if wage growth moves about 3% and unit labour costs rise, then a decision on a rate hike comes into sharper relief. (A reminder that average pay rose by 2.9% in the three months to July.)

If #UK economy grows above trend, has rising core inflation and wages above 3% then the decision on rates comes into sharper relief

— Phillip Inman (@phillipinman) September 16, 2015

#BOE Mark Carney says the "best collective judgement" of the rate-setting committee is that rates will rise in Q2, April to June next year

— Rob Young (@robyounguk) September 16, 2015

Updated

MPC member Ian McCafferty, who voted for a rate rise last time round:

@bankofengland McCafferty says UK manufacturing might be struggling but is only 10% of economy, so not a guide to it's health

— Phillip Inman (@phillipinman) September 16, 2015

More from the UK Treasury select committee quizzing Bank of England governor Mark Carney and members of the rate-setting monetary policy committee (Ian McCafferty, Kristin Forbes, and Martin Weale):

@bankofengland Carney says UK growing above trend and will continue to over next few years. @OECD says 2.3% growth next year. Above trend?

— Phillip Inman (@phillipinman) September 16, 2015

@bankofengland Mark Carney sounds like recent China trip took its toll. Maybe a little bit of a cold and #sinus trouble

— Phillip Inman (@phillipinman) September 16, 2015

BoE’s McCafferty: Could See Faster Pickup Than Expected In Wage Growth $GBPUSD

— Live Squawk (@livesquawk) September 16, 2015

BoE's McCafferty Is Concerned That Inflation Could 'Outpace' Projection $GBPUSD

— Live Squawk (@livesquawk) September 16, 2015

BoE’s McCafferty Says Deflation Risks Are ‘Now Very Low’ $GBPUSD

— Live Squawk (@livesquawk) September 16, 2015

Meanwhile the Bank has released reports to the committee from Mark Carney and Kirstin Forbes.

Wall Street opens higher

Ahead of the all important Federal Reserve decision on interest rates, US markets have joined in the global rally, adding to Tuesday’s gains.

In early trading the Dow Jones Industrial Average is up 29 points or 0.18%. Elsewhere the FTSE 100 is 1.32% higher - helped by the news of a possible merger between drinks groups SABMiller and Anheuser-Busch InBev - while Germany’s Dax is up 0.11%.

The other MPC member at the Treasury Select Committee, Kristin Forbes, is also worried about volatility:

@bankofengland Kristin Forbes says recent financial volatility played a part in her decision to vote against a rate rise

— Phillip Inman (@phillipinman) September 16, 2015

UK rate rise timing clearer at turn of year - Carney

Bank of England governor Mark Carney is up before the Treasury Select committee to discuss the latest inflation report.

On interest rates he said there was “a wide distribution of possible outcomes around any expected path for bank rate.”

He said the timing of a rate rise would be in sharper focus at the turn of the year.

One uncertainty of course has been the recent worries about the outlook for China’s economy. He said there was “downside risk” but not enough to adjust the Bank’s forecasts at the moment.

Monetary Policy Committee member Ian McCafferty said he had moved from believing rates should remain on hold to believing they should rise because he was worried about the prospect for the inflation outlook, notwithstanding any international risks.

But former hawk (although he criticised the term) Martin Weale said it was not appropriate for a rise because of the Chinese slowdown, further recent falls in oil and raw material prices and weak UK productivity.

The US inflation data is likely to add to the chances of the Federal Reserve keeping interest rates on hold on Thursday, said Har Bandholz, chief US economist at UniCredit Research. He said:

Now that the last important economic data releases ahead of tomorrow’s FOMC decision is out, we know as much as before:

The main growth engine of the US economy, the consumer, has been doing well – at least until before the financial market volatility began (we are confident that this improvement has continued and will continue, but the data for this period still has to be released).

The manufacturing sector, on the other hand, still suffers from global headwinds, the stronger US dollar, and – in the short-term –, from an inventory correction. Finally, inflation rates are currently held back by transitory factors. While the core CPI still stands at a relatively solid 1.8% year on year, it has lost some momentum since June, mostly due to the renewed decline in energy prices.

Moreover, the Fed prefers to look at the Personal Consumption Expenditures deflator excluding food & energy, which has slowed in July to 1.2% year on year, the lowest since early 2011.

We had pointed out before that this number is artificially biased downward by low health care costs, but FOMC members still seem to see it as their benchmark measure. Low inflation, in combination with the fact that the risk averse Fed would like to get a better sense about how the latest global developments – read: the slowdown in China, the related stock market sell-off and the renewed decline in oil prices – affect the outlook for growth and inflation, most likely mean that the FOMC will leave rates unchanged at this week’s meeting.

The August US inflation figure will probably not change the Federal Reserve’s decision on interest rates, said Rob Carnell of ING Bank. He expects no change from the central bank although admits a small hike could be on the cards:

US August CPI was the last significant piece of data standing between the Federal Open Market Committee and its rate decision on Thursday, and it came in almost bang on expectations, with the only marginal deviation from expectations being the core inflation rate, which was unchanged at 1.8% year on year - though from an expected 0.1% month on month gain, so almost certainly just a rounding effect.

Headline inflation was unchanged at 0.2% year on year, dragged down by a 2.0% month on month decline in energy prices – not surprisingly.

his result doesn’t even give a directional boost to the hawks, which might have been the case if energy had dragged just a little less. That said, this was never likely to be a decisive piece of data, and the FOMC members will probably go into this meeting already with a good idea of what they want to do. Recent data will have played a minor role in that conclusion. Our base case remains no hike with a strong hint for October, but a small (less than 25 basis point hike) still looks like a strong call to us.

Followers of the eurozone debt crisis should check out this story from Athens, on the worrying rise of Greece’s extremist Golden Dawn party, ahead of Sunday’s elections:

US consumer prices fall

The US monthly inflation rate has turned negative, giving the Federal Reserve another reason to hold off raising interest rates tomorrow.

Consumer prices unexpectedly fell by 0.1% month-on-month in August, mainly due to cheaper gasoline prices. This left the annual Consumer Prices index unchanged at 0.2%.

This is the first drop in the monthly inflation rate since January, defying expectations of a small rise in prices.

Ooops! Consumer Prices in U.S. Drop in August on Plunging Energy Costs http://t.co/Okx9UhWJId pic.twitter.com/pk34kWkx9d

— Holger Zschaepitz (@Schuldensuehner) September 16, 2015

In response, the yield on American government debt has dropped a little, suggesting the Fed is less likely to hike tomorrow.

2-year yield drops back below 0.8000 after CPI. On balance, tame print doesn't put any pressure on the Fed to hike.

— Joseph Weisenthal (@TheStalwart) September 16, 2015

Sterling is continuing to strengthen, as today’s wage growth figures fuels predictions the the Bank of England could raise interest rates sooner than expected.

The pound has now gained a whole cent against the US dollar to $1.5445. It’s also up 1% against the euro to a six-day high of €1.3744, meaning one euro is worth 72.66p.

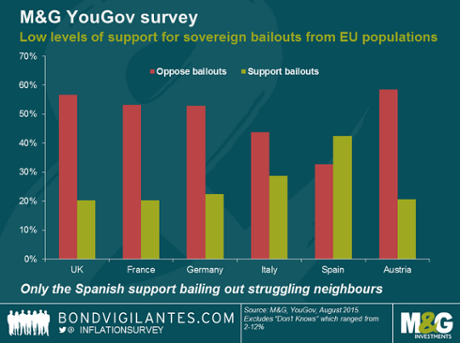

On a different note, a survey from City firm M&G Investments has found little appetite among European citizens for any more government bailouts.

M&G reports that Spain is the only country where a majority of people back the concept (Spain being one country that could have been dragged into the eurozone debt crisis)

Given the mess suffered by Greeks since 2010, it’s perhaps not surprising. But it could make it harder for Europe to grow and drive down unemployment, as M&G’s Jim Leaviss explains:

To become an Optimum Currency Region, the Eurozone needs fiscal transfers between areas doing well, and areas where the economy is weak. The survey data confirm that the majority of the public do not support such transfers. This is perhaps no surprise – we blogged a couple of years ago that some German states are vehemently against fiscal transfers even within Germany itself, let alone to other EU members.

The lack of public support does not mean that there can be no bailouts – we’ve already had sovereign bailout programmes within the EU. But it does mean that they lack democratic support and perhaps also that political parties that reflect the anti-bailout views of voters are likely to do well in the future. It also means that the agents for future bailouts are likely to remain institutions one step removed from the democratic process, such as the ECB and the IMF.

And whilst we can look at these results and tell ourselves that they are an indication that the European project is flawed and broken, we should ask ourselves how Californians would vote if they had a choice about fiscal transfers to Detroit, or if the UK’s Home Counties were asked if they wanted to continue redistributing tax revenues to former industrial areas elsewhere in the country.....

More here:

New M&G YouGov survey: there’s very low support in Europe for sovereign bailouts

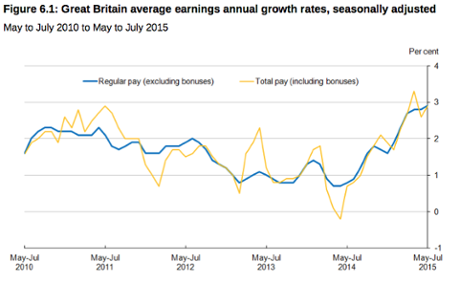

Full story: UK wages rising at quickest rate in six years

The rise in annual wage growth to 2.9% in the last quarter suggests the cost of living crisis is finally easing (although not for everyone, of course).

My colleague Heather Stewart reports:

Pay for Britain’s workers is rising at the fastest pace for more than six years, even before George Osborne’s national living wage is implemented, in a sign that living standards are continuing to rise.

Official figures showed that average pay across the economy increased by 2.9%, when comparing May to July with the same period a year earlier. The growth rate was the same once bonuses were taken into account.

The Office for National Statistics said that was the fastest pace of wage growth since the three months to January 2009 – and with inflation running at 0.1% in July, that suggests the long-running squeeze on living standards has come to an end.

City analysts said the pay data suggested consumer demand, a key driver of economic growth, would be underpinned by the rise in real wages.

Howard Archer, of consultancy IHS Global Insight, said: “July’s marked strengthening in earnings growth coupled with consumer price inflation dipping to 0.0% in August is very good news for consumers’ purchasing power.”

Osborne said the figures were an indicator his economic plan was working. “It is welcome news that pay packets are rising and jobs are being created,” he said. “With wages up 2.9% over the year and inflation low, working people have received the fastest real terms rise in over a decade.”

Here’s Heather’s full story:

Updated

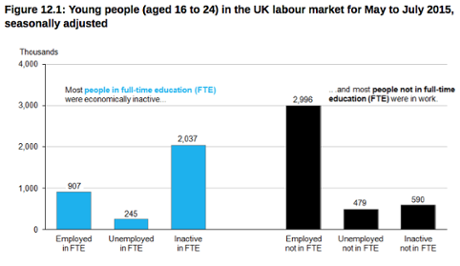

Young people "risk falling behind" in labour market

Britain’s youth unemployment rate is too high, and falling too slowly, warns Lindsay Owen, Deputy Director of Policy at The Prince’s Trust.

She says:

“While overall unemployment continues to fall steadily, there is a real danger that young people could be left behind. Whereas overall unemployment has fallen by 8 per cent over the past 12 months, youth unemployment has only fallen by 1 per cent, barely shifting for a year.

“Such a sustained period of stalling clearly shows there is an ongoing and pressing need for us to help young people develop the skills and confidence they need to move into work and have the best possible chance of building a successful future.”

And here’s some context:

For May to July 2015, for people aged from 16 to 24, there were:

- 3.90 million people in work (including 907,000 full-time students with part-time jobs)

- 723,000 unemployed people (including 245,000 full-time students looking for part-time work)

- 2.63 million economically inactive people, most of whom (2.04 million) were full-time students

Young people continue to get the rough end of the labour market, although the situation is slowly improving.

The youth unemployment rate (for 16 to 24 year olds) was 15.6% in the three months to July, almost three times the overall rate.

It is also:

- lower than for February to April 2015 (16.1%)

- lower than for a year earlier (16.6%)

- higher than the pre-downturn trough of 13.8% for the 3 months ending February 2008

Labour: No room for complacency

Owen Smith MP, Labour’s Shadow Work and Pensions Secretary, is concerned that unemployment rose by 10,000 in the last quarter:

Here’s his response:

“It’s welcome news that workers’ pay packets are increasing after years of stagnating. However, this is now the third consecutive increase in unemployment and Ministers mustn’t become complacent about overall joblessness.

“With such low levels of productivity persisting in the workforce and high levels of youth unemployment, the Government must do more to bring about an increase in the number of secure jobs in the British economy.

“Rather than stripping workers of their employment rights and taking thousands of pounds a year out of the pockets of millions of working families across the UK, the Government should be backing British workers to bring confidence and optimism back into our workforce.”

Updated

Another reason for caution. The number of women classed as unemployed spiked by 23,000 in the three months to July.

The number of unemployed men fell by 13,000, though, meaning the unemployment total rose by 10,000.

#Breaking Unemployment rose by 10,000 between May and July to 1.82 million, official figures showed today

— Press Association (@PA) September 16, 2015

That’s compared to the February-April quarter.

Updated

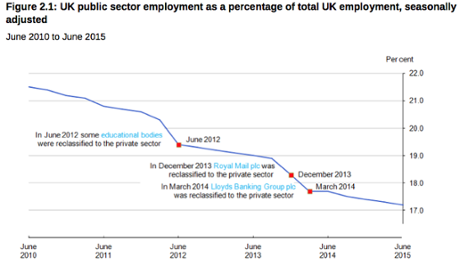

Today’s labour market report isn’t all good news, especially for those already employed in the public sector or looking for work.

Dr John Philpott, director of The Jobs Economist, explains:

“It’s now fairly clear that the UK labour market recovery changed tack in the first half of the year. The previous and prolonged ‘jobs-rich/pay-poor’ trend appears, at least for now, to have gone into reverse, with the headline unemployment rate static at 5.5% since the spring while the rate of pay growth has risen to 2.9%.

The good news is that this provides further evidence that the much needed improvement in labour productivity may at last be underway. However, while this will be welcomed by employers, wage earners and economic pundits, the news is not so good for jobseekers because it now looks as though it will take a little longer than previously expected for unemployment to fall back to the pre-recession rate.

“Public sector workers will also be feeling less than chipper. Their pay is rising at a rate of 1.3%, almost three times slower than the average rate of pay growth in the private sector, while the first half of the year saw an underlying fall (adjusting for statistical reclassification effects) of 22,000 in the number of people employed in the public sector.”

And this graph shows how the public sector workforce has shrunk on David Cameron’s watch:

This chart explains why S&P have downgraded Japan:

S&P: #Japan govt's strategy to revive econ growth & end deflation appears unlikely to reverse fiscal deterioration. pic.twitter.com/G6qAlggfoD

— Holger Zschaepitz (@Schuldensuehner) September 16, 2015

It shows that country’s national debt is expected to keep rising until the 2020s, to 250% of GDP.

Just in - Standard & Poor’s has hit Japan with a credit rating downgrade, warning that prime minister Shinzo Abe’s attempts to stimulate growth is faltering.

Here's S&P's downgrade of Japan. http://t.co/si1NNat2ru And here's the summary: pic.twitter.com/pkO7M4GcEv

— Joseph Weisenthal (@TheStalwart) September 16, 2015

S&P has cut Japan’s rating from AA- to A+, which is only the fifth highest rating.

S&P downgrades Japan. AA- to A+. Very retro.

— Burnett Tabrum (@BTabrum) September 16, 2015

It’s still one notch higher than Fitch, who cut Japan to A in April.

Updated

Andy Scott, economist at HiFX, has explained why today’s data sent the pound jumping this morning:

Average earnings rose at their fastest pace in six years in July, showing that the improving labour market is feeding increased wage demands – a sign that employers are willing to pay more to keep existing, or hire new workers.

“The news of individuals seeing strong pay growth in real terms should continue to support domestic demand and economic growth, all the more important when the global growth outlook is weakening. This also tallies with consumer confidence which has recently been at a 15-year high, as people’s improving financial position boosts sentiment.

“Sterling rose more than half a percentage point against the dollar to 1.54, and by the same against the euro to 1.37 as the news supports those at the Bank of England who are signalling rates will need to rise “sooner rather than later.”...

The pound has jumped half a percent against the US dollar, on the back of today’s labour market report.

Traders are calculating that Britain’s rising wage growth means the Bank of England may raise interest rates sooner.

Update. The Treasury have amended George Osborne’s comments:

Great Treasury comms cock-up. Spot the difference between the initial quote emailed to journalists, and the second: pic.twitter.com/6T9CwIfVe7

— Mike Bird (@Birdyword) September 16, 2015

'Ah shit no, privatisation's the good one! Don't send, don't send!'

— Mike Bird (@Birdyword) September 16, 2015

Breaking away from unemployment....the OECD has just issued a new report, warning that the world economy is slowing.

It has cut its forecast for global growth from 3.1% to 3.0%, and trimmed China’s from 6.8% to 6.7%. More here:

Osborne: it's welcome news

Chancellor George Osborne has hailed the rise in wage growth, and taken a swipe at new Labour leader Jeremy Corbyn (although not completely successfully).

Here’s the statement:

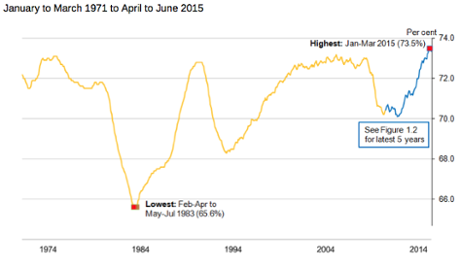

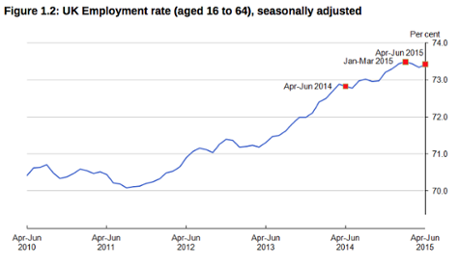

“It is welcome news that pay packets are rising and jobs are being created. With wages up 2.9% over the year and inflation low, working people have received the fastest real terms rise in over a decade. At 73.5%, the employment rate is the highest it has been.

But we still face risks both from the global economy and from those at home who would undermine our economic security, hike taxes and privatise industry. This government will continue to support firms, increase training and provide more free childcare for working parents, as well as introducing a National Living Wage.”

I think he means ‘....and nationalise industry’....

Whoops! Osbo statement on jobs warns of risk of "those at home who would undermine our economic security, hike taxes and privatise industry"

— Heather Stewart (@heatherstewart3) September 16, 2015

Updated

Here’s some instant reaction to today’s UK labour market report, focusing on the news that wage growth is running at its fastest rate since 2009.

U.K. wages grew at fastest pace in 6 years; unemployment rate unexpectedly fell - are inflationary pressures building in the labor market?

— Francine Lacqua (@flacqua) September 16, 2015

Overall labour market picture: employment gains topping out, wage growth picking up, hopeful signs on productivity.

— Duncan Weldon (@DuncanWeldon) September 16, 2015

UK real earnings growth up to territory more familiar in the pre-crisis years. Needs productivity growth to sustain. pic.twitter.com/hX3AWS7hrm

— RBS Economics (@RBS_Economics) September 16, 2015

Unemployment report: the key points

You can download a pdf of today’s unemployment report here.

Here are the key points:

- There were 31.09 million people in work, 42,000 more than for February to April 2015 and 413,000 more than for a year earlier.

- There were 22.74 million people working full-time, 361,000 more than for a year earlier. There were 8.36 million people working part-time, 52,000 more than for a year earlier.

- The employment rate (the proportion of people aged from 16 to 64 who were in work) was 73.5%, little changed compared with February to April 2015 but higher than for a year earlier (72.8%).

- There were 1.82 million unemployed people (people not in work but seeking and available to work), 10,000 more than for February to April 2015 but 198,000 fewer than for a year earlier.

- The unemployment rate was 5.5%, unchanged compared with February to April 2015 but lower than for a year earlier (6.2%). The unemployment rate is the proportion of the labour force (those in work plus those unemployed) who were unemployed.

- There were 8.99 million people aged from 16 to 64 who were economically inactive (not working and not seeking or available to work), 24,000 fewer than for February to April 2015 and 65,000 fewer than for a year earlier.

- The inactivity rate (the proportion of people aged from 16 to 64 who were economically inactive) was 22.1%, little changed compared with February to April 2015 but down slightly from a year earlier (22.3%).

- Comparing May to July 2015 with a year earlier, both total pay (including bonuses) and regular pay (excluding bonuses) for employees in Great Britain increased by 2.9%.

UK wage growth hits six year high

Wages across the UK have risen at their fastest pace since 2009.

The ONS reports that average pay rose by 2.9% in the three months to July, compared to a year ago. That’s the strongest growth rate for regular pay (excluding bonuses) since 2009.

That’s an encouraging sign, suggesting that the recovery is feeding through to pay packets. And with inflation at zero, it means real wages are running at a pretty decent rate.

But it also raises the chances of an earlier interest rate rise, if the Bank of England concludes that inflationary pressures are building.

Today’s report also shows a drop in the total hours worked.

Total hours worked down on the quarter, whilst GDP growing. Evidence that UK productivity is picking up.

— Duncan Weldon (@DuncanWeldon) September 16, 2015

The number of people in work across Britain rose by 42,000 quarter-on-quarter to 31.09 million.

That leaves the employment rate little changed at 73.5%, a record high.

Speaking on Sky News right now, employment minister Priti Patel says:

The economy is still growing, with more people in work than ever before.

Updated

Today’s report shows that there were 1.82 million unemployed people in Britain in the three months to July.

That’s 10,000 more than in February to April, but it’s also lower than the 1.85 million recorded a month ago.

UK unemployment data released

Here comes the UK unemployment data.

And the top line is that the jobless rate has fallen back to 5.5% in the three months to July, compared to 5.6% in the three months to June. That’s better than expected.

Lots more to follow....

UK unemployment data out in 10 mins. Should see jobless rate hold at 5.6% and average earnings nudge higher. #GBP #FTSE

— Joshua Raymond (@Josh_RaymondUK) September 16, 2015

Economists will scrutinise today’s unemployment data for signs that the labour market is weakening.

These charts, from last month’s jobless report, show how the UK employment has dipped recently, after hitting a record high in the spring.

Updated

China’s late surge is helping to keep shares up in Europe, but that rally could fade away if the UK jobless data (due in 40 minutes) is weak.

Conner Campbell of SpreadEx explains:

Wage growth is expected to see a mild increase, from 2.4% to 2.5% (though the figure has missed estimates for the past 2 months), whilst the claimant count change is forecast to decrease by 5.1k against the 4.9k drop announced in August.

The unemployment rate, meanwhile, is expected to remain at 5.6% after unexpectedly creeping up from 5.5% in July. In anticipation of these results the FTSE was up by around 30 points, though that increase is lower than its initial 50 point high.

China's stock market in late surge

There’s excitement in China right now where the stock market has surged by almost 5%.

After a subdued start, the Shanghai composite index leapt in late trading to close 147 points higher at 3,152. That reverses two days of losses, which were blamed on rising worries over the Chinese economy.

And it happens again...sudden rally in #China stock market +5% last hour of trade pic.twitter.com/2yygLdY5ED

— Caroline Hyde (@CarolineHydeTV) September 16, 2015

A few theories are circulating to explain today’s recovery.

One is that Beijing authorities intervened, again, to get the index back over the 3,000 point mark.

Another is a rumour that Global index compiler MSCI is going to include the Shanghai market in its global index.

A third is that traders are optimistic that the Fed will sit tight tomorrow, and leave US interest rates unchanged.

But sometimes, you’ve got to admit that there’s no easy answer:

Late surge in China. This time led my small caps. Don't trust anyone who says they know why. http://t.co/FkaZpIDnEV pic.twitter.com/jevrqXrTox

— Patrick McGee (@PatrickMcGee_) September 16, 2015

Glencore shares jump after share placement lifeline

Commodity trading giant Glencore is leading the FTSE 100 risers this morning, up over 4%, after raising $2.5bn through a share placement last night.

Glencore certainly needs the money. The slump in commodity prices has left the Swiss based firm with a $30bn debt mountain, which will be trimmed to $20bn once the rescue plan announced last week is implemented.

Shares had hit a new record low last night, having shed around three quarters of their value since it floated just four years ago. A blow to millions of Brits whose pension funds hold Glencore shares, although at least billionaire founder Ivan Glasenberg and top colleagues are sharing the pain (and investing more money via this placement).

Glencore prices share sale at 125 pence a share - 2.4% discount to yesterday close - raising $2.5bln pic.twitter.com/S25R4zKdYn

— Jesse Riseborough (@JP_Riseborough) September 16, 2015

Today’s rally shows relief that one hurdle is cleared. But two more remain, as my colleague Nils Pratley explains:

The first is Glencore’s vulnerability to more falls in the prices of copper and coal. The former has shown signs of stability in the last week, partly because Glencore itself is shutting a couple of mines, but coal shows no hint (yet) of reaching a trough. After the fundraising, Glencore is less indebted than it was but, remember, the starting point was borrowings of $30bn.

The second factor can’t be measured so precisely. It is the damage to Glasenberg’s reputation for reading the market. Last year’s $1bn share buyback – at an average of roughly 300p a share versus 128p now – was plainly a mistake, born of over-optimism.....

More here:

Europe’s stock markets are opening now, and shares are rising.

In London, the FTSE 100 is up 41 points or 0.7% at 6167. The pound is flat, as traders await the jobless data.

The German DAX, Spanish IBEX and Italian FTSE MIB shares indexes have all gained 1%.

Traders may be less worried about tomorrow meeting of the Federal Reserve, where policymakers will decide whether or not to hike interest rates.

Mike van Dulken of Accendo Markets explains:

Is fear receding ahead of tomorrow’s Fed decision? Are markets less worried about a hike or more convinced of no change?

Consensus remains divided after the latest US data.

The employment data may also show that average earnings rose over the summer.

CMC’s Michael Hewson explains:

Today’s average earnings data are expected to continue to contribute to a rise in disposable incomes with a rise from 2.8% to 2.9% for the three months to July, excluding bonuses.

The ILO unemployment rate for July is expected to remain stable at 5.6% with August jobless claims set to decline by 5k.

The Agenda: UK unemployment, US and euro inflation.....

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Today we discover if Britain’s employment market is weakening, when the latest jobless data is released by 9.30am.

The figures will show the unemployment total in the three months to July, and also how many people claiming jobless benefits in August. We’ll also see whether wages picked up.

After a solid run recently, the last two months’ data have been unexpectedly weak. UK unemployment rose by 15,000 in the three months to May, for the first time in two years. That trend continued the next month, with an extra 25,000 people out of month in the quarter to June.

Economists predict that the jobless rate will remain unchanged at 5.6%, and that the claimant count will dip by around 5,000. We’ll find out soon.

The unemployment data will be scrutinised in Westminster, as well as the City, as Labour’s new leader Jeremy Corbyn faces David Cameron at Prime Minister’s Questions at noon. Get the popcorn ready.

Yesterday we learned that Britain’s inflation rate has fallen back to zero, as weak energy and lower food prices keep the cost of living pegged back.

At 10am it’s the eurozone’s turn to report inflation data. Economists expect an annual rate of just 0.2%. Anything weaker will put more pressure on the European Central Bank to consider fresh stimulus measures.

Then at 1.30pm BST we get America’s August inflation report, which is the final clue to how the Federal Reserve might act at Thursday’s FOMC rate-setting meeting.

Big data day ahead pre #FOMC Key data: #UK unemployment at 09:30 #EURO CPI at 10:00 #US CPI at 13:30 #USD #GBP #EUR

— IGSquawk (@IGSquawk) September 16, 2015

We should also hear from Bank of England governor Mark Carney this afternoon when he, and senior colleagues, testifies to the Treasury select committee on the latest inflation report. Kickoff is 2.15pm.

CArney in front of TSC at 2.15pm being questioned by MPs on latest inflation report: http://t.co/DXIZ4EtgU5

— Louise Cooper (@Louiseaileen70) September 15, 2015

Not much corporate news to entertain us, although JD Sport is reporting results this morning and trainmaker Hornby has warned that revenues will be weaker than expected this year.

And there’s just four days to go until the Greek general election. Excitement isn’t exactly at fever pitch yet, though. The latest poll puts the conservative New Democracy (ND) party slightly ahead of Alexis Tsipras’s Syriza:

#Greece poll [Pulse/@action24_]: ND 27.5 Syriza 27 GD 6.5 PASOK 6.5 Potami 5 KKE 5 LAE 3.5 EK 2.5 ANEL 2 pic.twitter.com/pGG1Ou9FUD

— Yannis Koutsomitis (@YanniKouts) September 15, 2015

We’ll be tracking all the main developments through the day...