The TV debate later may rest more than anything else on swaying women, the vast majority of whom account for the 10% of voters who have declared they are still undecided ahead of Sunday’s elections, says our correspondent Helena Smith. She reports:

In a political culture that is highly influenced by personalities, tonight’s debate could be decisive for either camp. The conservative New Democracy leader, Vangelis Meimarakis, who has worked his way up through the party, at one time heading its youth wing, will make much of his experience. But insiders tonight are also saying the political veteran will have to make a mark on women - and in this regard they are not displaying the optimism with which they have greeted polls in recent days. “If it were up to men we might win it hands down,” one well-placed source has just confessed. “Men back Meimarakis but women just love Tsipras, especially [those] in public sector jobs. And that is going to be hard to beat.”

In private, conservatives also say they fear left-wingers are finally rallying around Tsipras with many privately admitting that Syriza will emerge as the first party which under Greek law will enable it to clinch the 50-seat bonus. “Those who remain undecided are [mostly] women,” said one former female New Democracy MP. “At the end of the day they are going to rally around Syriza because they don’t want the last seven months to be a parenthesis when the left finally got into power and was soon booted out. That, at least, is how a lot of us are feeling but anything could happen in tonight’s debate.”

On that note, it’s time to close up for now, so thanks for all your comments.

A new poll before the Greek election shows Syriza and New Democracy neck and neck:

#Greece poll [MetronAnalysis]: Syriza 24,6 ND 24.6 GD 5.6 ΚΚΕ 4.8 Potami 4.6 PASOK 4.2 LAE 3 EK 3 ANEL 2.3 Undec 9.1 pic.twitter.com/gTUlXxXXem

— Yannis Koutsomitis (@YanniKouts) September 14, 2015

But in terms of the party leaders, New Democracy’s Meimarakis is ahead of Syriza’s Alexis Tsipras:

#Greece poll [MetronAnalysis]: Meimarakis 49 Theodorakis 44 Tsipras 44 Gennimatà 37 Koutsoumbas 29 Kammenos 27 Lafazanis 16 Tsipras 3rd!

— Yannis Koutsomitis (@YanniKouts) September 14, 2015

Updated

European investors nervous after Chinese data

Markets are (mostly) lower following more disappointing Chinese economic figures which cast doubt once more on the outlook for the world’s second largest economy, and sent commodities such as copper and oil sliding again. At the same time there was a great deal of caution ahead of this week’s US Federal Reserve meeting. Until recently traders believed a US rate rise was almost inevitable, but the volatility since China devalued its currency amid the poor data has left investors uncertain about how the Fed will act. And markets hate uncertainty. So the final scores showed:

- The FTSE 100 fell 33.17 points or 0.54% to 6084.59

- France’s Cac closed down 0.67% at 4518.15

- Italy’s FTSE MIB dropped 0.96% to 21,553.80

- Spain’s Ibex ended down 0.43% at 9696.4

- Germany’s Dax was an exception, clinging on to a 0.08% rise to 10,131.74

On Wall Street, the Dow Jones Industrial Average is currently 77 points or 0.47% lower.

Over in Greece the digs are starting even before the TV debate between Syriza’s Alexis Tsipras and Vangelis Meimarakis of New Democracy:

(Ahead of debate) New Democracy's Meimarakis: Syriza is a 3 percent party and it's heading back there #Greece pic.twitter.com/Z6NCZRh4gK

— Derek Gatopoulos (@dgatopoulos) September 14, 2015

US consumer expectations for inflation fell last month to their lowest level for more than two years.

A survey released by the Federal Reserve Bank of New York ahead of this week’s US central bank meeting on interest rates showed inflation expectations to 2.9% for three years hence. That is down from 3% in July, and is the lowest since June 2013. Expectations for inflation a year ahed fell from 3% to 2.8%.

New York Fed survey: Consumer inflation expectations 3 years ahead dip to 2.9% - lowest level since June 2013. pic.twitter.com/NxF0dFlMPk

— Mark Constantine (@vexmark) September 14, 2015

The full report is here.

Greek newspaper Kathimerini has been looking at the debate later, which will see Alexis Tsipras and Vangelis Meimarakis attempt to sway undecided votes ahead of Sunday’s poll. It reports:

Greece’s two political heavyweights will have undecided voters in their sights on Monday in a final televised head-to-head debate before national elections, both seeking the elusive soundbite that might break a deadlock in opinion polls.

With Sunday’s ballot looming, the leftist Syriza party of former prime minister Alexis Tsipras and the New Democracy conservatives led by Vangelis Meimarakis have been stuck in the same place in the surveys for several weeks - virtually neck and neck and well short of parliamentary majority.

Their respective personal popularity ratings have also stagnated around or slightly below 45 percent.

Both men have so far given loyal voters little reason to switch allegiance, having devoted much of their campaigns to trading accusations over the country’s ailing economy, institutionalized corruption and responses to the refugee crisis.

But voters yet to decide which party to back or intending to abstain altogether - up to a fifth of the electorate according to some polls - offer a clearer target.

“This debate is crucial mainly because of the big number of undecided voters and those who don’t want to vote,” Dimitris Mavros of pollsters MRB said. “The question is who will be more convincing.”

Full report here.

Updated

A lack of data today has seen markets continue to drift mostly lower, Germany’s Dax being a notable exception.

Tuesday sees UK inflation figures, which could see consumer price inflation move back to zero, as well as US manufacturing and retail sales figures. The American data will be closedly watched as the Federal Reserve meets to consider whether or not to raise US interest rates. Connor Campbell, financial analyst at SpreadEx, said:

There was no real news to work with this afternoon, nothing to de-fog the market-confusing mist surrounding the Fed’s current position in regards to a September rate-hike. Tomorrow afternoon could help provide some much needed clarity, as the US releases its Empire State manufacturing index, industrial production and retail sales figures; then again it could not, with analysts expecting another muddled set of numbers.

The Dow is currently 10 points lower, off its worst levels, while the FTSE 100 is down around 11 points. Mining shares have reversed early gains, as copper prices fall in the wake of the earlier disappointing data from China and oil prices slide again. Brent crude is 1.95% lower at $47.20 a barrel.

The Dax is holding onto its gains, up 0.42% but European shares are likely to react on Tuesday to the debate on Monday evening in Greece between Syriza’s Alexis Tsipras and New Democracy’s Vangelis Meimarakis. Campbell said:

The polls suggest the race will go down to the wire, so this final TV debate could provide a decisive moment as Tsipras moves to defend his record as leader.

Ahead of the debate, the Athens market has slipped 0.12% to 673 points.

The Bank of England’s Andy Haldane has finished his twitter Q&A, harking back to the start of the session:

Andy Haldane

— Bank of England (@bankofengland) September 14, 2015

@bankofengland ...couldn't help yourself! ;)

— RANsquawk (@RANsquawk) September 14, 2015

Updated

Back at the Bank of England, Andy Haldane is getting into the swing of Twitter - being careful to ignore those plucky correspondents asking the chief economist outright how he intends to vote on interest rates over coming months.

As a little reminder, Haldane stands out as the member of the nine-person Monetary Policy Committee, who not so long ago warned that hiking rates too soon from their record low 0.5% level could derail the recovery. He even suggested he could vote for a cut. I believe the Twitter hashtag here would be #HowLowCanTheyGo

Those Dovish remarks probably prompted these (unanswered) questions in today’s Twitter Q&A:

If you had to vote for a rate change, would it be for a hike or a cut?! #boeopenforum

— Justin (@Donnie_Eagle) September 14, 2015

In the same #TellUsAboutRates vein:

.@bankofengland Do you agree with BoE Forbes that strong GBP might not have lasting effect on inflation? #BoEOpenForum

— Live Squawk (@livesquawk) September 14, 2015

#BOEOpenForum Considering time lags, do you feel that rates should be raised sooner as opposed to later? 'Normal' monetary policy is no more

— Admiral Markets (@AdmiralMarkets) September 14, 2015

(That refers to a speech by Haldane’s MPC colleague Kristin Forbes last week, raising the prospect of a rate hike sooner than markets expect)

It is often what central bankers don’t say that is most interesting. But here is a taste of what Haldane is saying:

@bankofengland Are banks' capital requirements high enough? #BoEOpenForum

— Paul Martin (@paul_tweet) September 10, 2015

.@paul_tweet #BOEOpenForum They will be 10x higher than pre-crisis. Should be higher still? Right question for tomorrow. We need that debate

— Bank of England (@bankofengland) September 14, 2015

@bankofengland is financial regulation helping or hindering market liquidity? Is that a good thing? #boeopenforum

— Economist view (@EconomistView) September 12, 2015

.@EconomistView #BOEOpenForum Market itself lowering liquidity, not just regulation. Too far? Open Forum will debate that head on.

— Bank of England (@bankofengland) September 14, 2015

#BoEOpenForum Andy, any concern that low rates limit @bankofengland ability to handle big capital market shocks/housing market corrections?

— Rob Yates (@Robert_A_Yates) September 14, 2015

.@Robert_A_Yates #BOEOpenForum FPC's new set of macroprudential tools aim to keep unruly market forces under control.

— Bank of England (@bankofengland) September 14, 2015

*FPC= Financial Policy Committee

Haldane is taking questions till 3.30pm BST. Wonder what he is making of the whole experience? He asked in a speech earlier this year what Twitter and shorter attention spans told us about changing human brains and the prospects for economic growth.

Markets are likely to remain volatile ahead of the Federal Reserve meeting. Mark Luschini, chief investment strategist at Janney Montgomery Scott, told Reuters:

The uncertainty is so high in regard to the [interest rate] announcement... it leaves investors a little bit paralysed relative to what to do in anticipation.

Wall Street falls ahead of Fed meeting

Meanwhile Wall Street has opened sharply lower, helping to accelerate declines in other markets.

The Dow Jones Industrial Average is currently down 93 points or 0.58%, as investors remain nervous about a slowdown in China and uncertain about the outcome of this week’s US Federal Reserve interest rate meeting.

The Dow’s decline has helped push the FTSE 100 0.7% lower, while France’s Cac is down 0.36%. However Germany’s Dax is just about in positive territory, up 0.02%.

Updated

This is the tweet Haldane is referring to, when the then Shadow Chancellor sent out a tweet with just his own name on it, which subsequently became an internet meme:

Ed Balls

— Ed Balls (@edballs) April 28, 2011

And the Haldane Q&A begins with this:

My first ever tweet. Tempted to just tweet my name, Ed Balls style, to get a day named after me. #TemptationResisted pic.twitter.com/o8fIH5VWIO

— Bank of England (@bankofengland) September 14, 2015

Bank of England policymaker Andy Haldane will shortly be holding a question and answer session on Twitter, details here:

How do we build effective financial markets? Join us for Q&A with Andy Haldane on Monday at 2:30pm #BoEOpenForum

— Bank of England (@bankofengland) September 13, 2015

Apple’s new launches seem to have gone well, according to the company. Reuters reports:

Apple said sales of its new iPhones were on pace to beat the 10 million unit sales it logged during the first weekend of sales last year.

The company did not disclose the specific number of preorders it received. Analysts had expected the company to log about 4.5 million preorders, in comparison with 4 million during the period last year.

The company said demand for iPhone 6S Plus, the larger phone, exceeded its forecasts for the preorder period. The iPhone 6S and iPhone 6S Plus will begin shipping on September 25.

The news has given support to a key supplier to Apple. UK chip designer Arm has seen its shares climb 1.6% on optimism about the new Apple products, pushing it to the top of a faltering FTSE 100, currently down 0.48%.

Updated

The early gains in Europe continue to fizzle out as traders predict an opening dip on Wall Street:

Despite a strong start, European indices failing to hold early gains. $FTSE -0.5% $DAX -0.13%. Calling $DJIA lower by 13 to 16420

— Brenda Kelly (@Brenda_Kelly) September 14, 2015

Updated

Today is the seventh anniversary of the collapse of Lehman Brothers.

Autum 2008 was a truly amazing time, as the titans of Wall Street and the City faced the abyss and the pillars of capitalism wobbled. Seven years on, has much really changed?

No, argues Steen Jakobsen, chief economist at Saxo Bank.

He writes:

We have learned nothing from history. Debt replaced productivity and the banks today have tougher regulations but also unprecedented “free money” from the central banks.

Banks, politicians and central banks have created an unholy trinity where each institution is co-dependent on each other to maintain the power. But no one can afford to face reality and stop the merry-go-round of mal-investment and excessive focusing on monetary policy despite neither history nor practice having any evidence that the trifecta can deal with growth, jobs or productivity. If anything, the proof shows the opposite.

Lehman could have been a “real crisis”, a real turnaround, a proper paradigm shift. But instead we bought time – the one thing we should not buy but use effectively. The past seven years became time wasted as the economy and society went into a standstill.

The elections across Europe are showing us how the social fabric is under attack, and the lack of jobs, innovation and growth are the end score for this experiment in futility.

Jakobsen argues that this post-crisis period is almost over, as the era of cheap money from accomodative central bank ends.

The next seven years will be lean, but positively lean. The cost of capital will rise, removing non-productive investment and probably hurt stock markets, which became safe havens under the fat years or pretend-and-extend squared, but that’s good news.

The absence of much serious news today (alas) is dragging the European stock markets slowly into the red.

The FTSE 100, German DAX and French CAC are all down between 0.2% and 0.4%, as traders prepare to be underwhelmed by the opening of Wall Street in 40 minutes.

Investors seem happy to sit on the sidelines until we hear from the Federal Reserve on Thursday (will they, or won’t they raise rates?).

As Connor Campbell of SpreadEX explains:

The outcome of Wednesday and Thursday’s FOMC meeting is still unclear, leaving investors with the unenviable task of trying to second guess the central bank.

The oil price is dipping today, pushing the price of a barrel of Brent crude down by 1% to $47.58 per barrel.

Today’s weaker-than-expected Chinese factory output and business investment data is fuelling concerns that energy demand is falling.

We still have some way to go to reach Goldman Sach’s prediction of $20 per barrel oil, though.

Some news! Ghana’s central bank has just hiked interest rates, to an eye-watering 25% (from 24%).

Central bank governor Henry Kofi Wampah said the move would fight inflation, which is currently running over 17%.

Ghanaians must hope the move provides some to their currency, the cedi, which has tumbled against the US dollar this year. That’s a major problem for citizens who have taken out mortgages in dollars, and seen their repayments soar.

Chinese investors were unnerved by a new clampdown against suspected market abuse, the Financial Times reports.

That helped to send the stock market down by as much as 4% today, before closing 2.7% lower -- its biggest loss in three weeks.

The FT says:

The China Securities Regulatory Commission late on Friday announced punishments of two wealthy individual investors for manipulating 13 different stocks using fake buy orders to temporarily boost their prices. That sent a chill through short-term speculators on Monday.

“For ‘drive-by money,’ this was a major blow. Now they lack any impetus to go long,” said Zhu Bin, analyst at Southwest Securities in Shanghai. Mr Zhu also said downward momentum increased after the Shanghai Composite broke below the psychologically important 3,200 level. Following the late-day rally, which pushed the index as low as 3,049, the index closed at exactly 3,200.

More here: China stocks’ worst day in nearly three weeks after punishments

Updated

There are four potential outcomes from Thursday’s eagerly awaited Federal Reserve meeting, say analysts at Royal Bank of Canada.

- no interest rate hike/no signal;

- no hike but a signal that, with markets having calmed down since late August, the Fed is ready to hike in Oct or Dec if things remain calm;

- a hike coupled with a signal that rate rises will be extremely slow (a commitment to keep rates on hold for x months or “one and done for now”); and

- a hike indicating the start of a tightening cycle, albeit slower than the ones we have seen in the past.

RBC’s official call is still that the Fed will hike rates at the September meeting, but that would be “difficult” as the markets expect borrowing costs to remain on hold.

Sue Trinh of RBC explains:

No hike will look bizarre in the face of what is likely to be an upward revision to the Fed’s 2015 GDP forecast and a downward revision to their unemployment rate projection.

We would expect Yellen to be questioned on that at the press conference, and any commitment to a hike in Q4 would be positive for the US dollar, pushing back on those who don’t believe the Fed will ever raise rates.

The two men battling to lead Greece will go head-to-head in a nationally televised debate at 9pm tonight (7pm BST).

The clash between Syriza’s Alexis Tsipras and New Democracy’s Vangelis Meimarakis will help determine which party comes first in Sunday’s general election. The victor will claim the 50 seat bonus available to the winner (out of 300 MPs), allowing them to either govern alone or lead a coalition.

Tsipras has been hit by a series of defections to the new anti-austerity Popular Unity party, and also faced criticism for taking Greece to the brink of Grexit before signing up to a third bailout.

Support for Meimarakis appears to be rising, though. He’s pledged to work with other parties to rebuild Greece’s economy and implement the new bailout deal.

The race remains very tight, as our Athens correspondent Helena Smith explains:

One survey, conducted by Public Issue and published in the leftwing party’s newspaper Avgi, indicated that the two parties are stuck in a dead heat on 31% each.

Tsipras, however, for whom support has dropped since he signed up to a third, hard-hitting bailout for his country, continued to outpoll his rival on the question of suitability for the post of prime minister.

“The outcome ultimately could be decided by the debate,” said Aristides Hadzis, a political analyst who teaches law and economics at Athens University. “A lot of the 10% who remain undecided are women who come from the Syriza camp and are generally friendlier towards Tsipras.

Here’s Helena’s full take:

This chart puts today’s decent eurozone factory data into context:

CHART: Euro-area industry makes good 3Q start. But output still 11% below pre-crisis levels. http://t.co/nFbviJHBcq pic.twitter.com/pX21UfXMQS

— Maxime Sbaihi (@MxSba) September 14, 2015

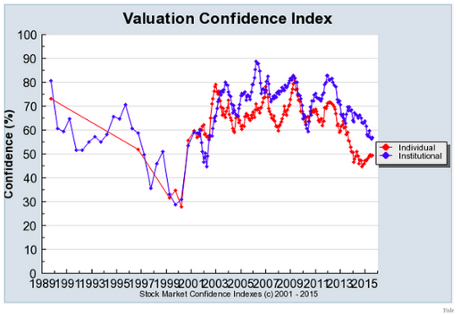

Shiller: US stock market looks like a bubble

Robert Shiller won a Nobel Prize in 2013 for his work on the irrational exuberance that can grip markets. So when he spots a stock market bubble, it’s worth listening.

Shiller, the Yale University economics professor, believes that the US stock market is overvalued, and primed to burst.

He has told the Financial Times that:

“It looks to me a bit like a bubble again with essentially a tripling of stock prices since 2009 in just six years and at the same time people losing confidence in the valuation of the market.”

Shiller has the data to prove his case too -- an index that measures stock market confidence. It is compiled by asking investors if they think the stock market is overvalued, fairly valued, or undervalued.

It’s now heading towards its lowest point since the dot-com bubble ended, in early 2000 (via Business Insider)

Shiller isn’t actually predicting that a huge crash is imminent, though:

“I’m not looking for any big effect....It’s been talked about for so long, everyone knows that it’s coming. It’s just not much of a big deal.”

Bob Shiller tells @johnauthers: worry less about the Fed, more about valuation. US stocks look "a bit like a bubble" http://t.co/cKvAyI3AfI

— James Mackintosh (@jmackin2) September 14, 2015

Eurozone factory output beats expectations

The latest survey of Europe’s factory sector is out, and it’s better than expected.

Industrial production across the eurozone increased by 0.6% year-on-year in July, twice as fast as economists expected. That extends the recovery that began around two years ago:

Euro area industrial production +0.6% in July 15 over June 15, +1.9% over July 14 #Eurostat http://t.co/kaF61GnalL pic.twitter.com/sujEr1KbC8

— EU_Eurostat (@EU_Eurostat) September 14, 2015

Italian factories performed particularly well, with output jumping 1.1% month-on-month, and Ireland had a stonking month, up over 7%. France, though, suffered a 0.8% decline.

#Euro-zone ind. production solid at +0.6%m/m in July. But boosted by 7.2% m/m jump in Ireland. Underlying picture still one of soft growth.

— Capital Economics (@CapEconEurope) September 14, 2015

Howard Archer of IHS Global Insight says:

There was a particularly encouraging jump in Italian production while growth was decent in Spain and Germany.

However, a sharp drop in French production fuels concerns over the economy’s potential to bounce back in the third quarter after GDP stagnated in the second quarter.

It’s worth remembering, though, that China’s factory sector is growing around three times as fast (6.1% year-on-year).

Updated

The stock market in China’s Shenzhen, which is heavy with tech stocks, had a particularly bad day:

Shenzhen Composite index down 6.7%.

— Morris Cabrioli (@insidegame) September 14, 2015

Updated

Here’s some more reaction to the latest Chinese data, and today’s drop in the stock market, from Reuters.

Zhou Hao, senior economist at Commerzbank AG in Singapore:

“Overall, the economy is very weak and the central bank may have to continue cutting interest rates and banks’ reserve requirement.”

Gu Yongtao, strategist at Cinda Securities:

“China’s economy faces relatively big downward pressure, so investor sentiment remains weak.”

European stock markets have risen in early trading, as investors resist the temptation to panic over China.

The FTSE 100 is up 46 points, or 0.75%, at 6163, reversing Friday’s dip.

Trading floors are primarily concerned with Thursday’s Federal Reserve meeting, and the possibility of interest rates being raised.

A hike seems unlikely in the current climate, with emerging markets such as China struggling.

Mike van Dulken of Accendo Markets explains:

As always, a decision on a US interest rate rise is expected to come down to the wire, but it’s not the type of decision to be made either hastily or in the absence of majority consensus within the US Central Bank, and therefore a delay until at least the next meeting (October) seems probable (maybe even December).

The markets have woken up to another morning of woes over the China economy, says FXTM Research Analyst Lukman Otunuga.

Most market participants were already concerned about the slowing rate of growth in the world’s second largest economy, and the annualised Industrial Production data failing to meet expectations will further concerns.

Not only was the figure at 6.1% lower than expected, but growth in fixed-asset investment is now reportedly at its weakest in 15 years. With such weakness being seen across large sections of the Chinese economy, the China markets are going to remain exposed to pressures and it is likely the government will remain on high alert to relieve pressures and induce stability in the domestic markets.

Although Premier Li Keqiang remains defiant that expectations of a 7% growth rate for China is achievable, the recent data from China has outlined nothing other than a deep economic downturn and there are already fears that the China data is much weaker than official statistics illustrate.

Today’s selloff was mild, compared to the drama of August.

But it has still pushed the Chinese stock market down towards an eight-month low:

Chinese markets post biggest fall since August 25th

China’s stock markets have just posted their biggest falls since the last week of August, despite a late (and somewhat suspicious) rally.

The benchmark Shanghai Composite shed 2.7%, having been down 4% in late trading, as traders reacted to the slowdown in business investment, and subdued factory growth, in August.

This latest data follows a 13% tumble in imports last month, adding to concerns that the Chinese economy is softening fast.

Analysts at Mizuho Bank reckon the slowdown could encourage the US Federal Reserve to leave interest rates on hold this week:

“Further deceleration in investments and imports plunge remain worrying.

This ups the likelihood of more China stimulus, but dampens the Fed jumping the gun.”

Updated

Russia’s largest port operator has just reported a sharp fall in profits and revenues, highlighting its weak econony.

Pre-tax profits at Global Ports halved in the first six months of 2015, as revenue shrank by 25%.

The company warned that consumer demand had been hit by Russia’s “challenging” macro-economic backdrop; ie, people are buying less stuff because the country is in recession.

Tiemen Meester, chairman, added:

Looking ahead to the second half of the year, we expect that the market will remain difficult.

Russian cargo firm Global Ports: "throughput -32% yoy in 1H.. revenue -25%.. economic backdrop in Russia challenging"

— Louise Cooper (@Louiseaileen70) September 14, 2015

Fears over China’s economy, and the prospect of a US rate rise, have hit Japan’s stock market too.

The Nikkei fell 1.6% by the close, amid small losses in Hong Kong and Seoul too.

Asia starts the week in the red after soft data from #China. Industrial economy continues to show signs of weakness. pic.twitter.com/us8norz424

— Holger Zschaepitz (@Schuldensuehner) September 14, 2015

Last weekend’s disappointing Chinese factory output and investment data have raised the pressure on Beijing to launch more stimulus measures.

There was one bright spot - retail sales beat forecasts with a 10.8% jump, suggesting some success in rebalancing the economy.

Angus Nicholson of IG says China is now exhibiting a “divergent two-speed economy, as consumption continues to do well while industrial production and investment slow.”

He adds:

It is thought that factory shutdowns surrounding the World Athletics Championship and WWII commemoration may have affected output somewhat. Nonetheless, the data is still pretty disappointing considering there have been frequent statements by the government, plus expectations in the market that investment would start to pick up in the second half of the year.

Weak Chinese data fuels slowdown fears

China’s stock market is heading for its biggest loss in several weeks, after fresh, disappointing, economic data shows that the country’s economy is slowing fast.

The Shanghai index has shed 4% in late trading today, in a new bout of angst. The market close in about 30 minutes.

Chinese #stocks sell-off back on...$87b lost in market value today...but volumes lower than average pic.twitter.com/bNiLTlZLeb

— Caroline Hyde (@CarolineHydeTV) September 14, 2015

The selloff is triggered by the news that China’s factory output grew by just 6.1% year-on-year in August, below expectations of a 6.4% rise.

And fixed-asset investment, which tracks business spending on new machinery and plants, grew by 10.9%. That’s the weakest rise since 2000.

Economists say that it shows the Chinese economy is weakening, putting the target of 7% growth this year at risk.

Updated

Introduction: Fed meeting and Greek elections loom

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

It’s going to be an exciting week. Economists and investors are already looking towards Thursday’s Federal Reserve meeting, when America’s interest rates could be raised for the first time since the crisis began.

On balance, the Fed is expected to sit tight again, given the recent ructions in the global economy, but no-one knows for sure.

Alastair Winter, chief economist at investment bank Daniel Stewart, argues that the time isn’t right for a hike:

Were it not so serious, it would be funny that, having hitherto taken enormous risks with expansionary monetary policy that is clearly no longer working, the FOMC might go ahead and tighten just at the point when further delay could be justified.

The US economy may be more self-contained than most but it too is participating in the slowdown in global growth and deflationary pressures.

And once the Fed meeting is over, we get Sunday’s Greek general election.

Tonight, former prime minister Alexis Tsipras of Syriza will debate the leader of the right-wing New Democracy party, Vangelis Meimarakis. Recent polling has shown the two parties neck-and-neck.

Six polls published today show a narrow lead of 0-0.7 pp for #SYRIZA over New Democracy, G Dawn in the 3rd place (>6%). #Greece #ekloges2015

— Manos Giakoumis (@ManosGiakoumis) September 13, 2015

Having said that, there’s not too much on the agenda today.

The only economic data of note is the latest eurozone industrial production survey, for July, at 10am BST. Economists predict monthly growth of 0.3%.

And Europe’s stock markets are expected to rise by close to 1%, having lost ground on Friday.

Our European opening calls: $FTSE 6172 up 54 $DAX 10217 up 93 $CAC 4590 up 41 $IBEX 9824 up 86 $MIB 21924 up 161

— IGSquawk (@IGSquawk) September 14, 2015

I’ll be tracking all the main events through the day.....

Updated