A day after the televised debate in Greece between Syriza’s Alexis Tsipras and New Democracy’s Vangelis Meimarakis, the latter has said he would seek a coalition with Syriza if it wins Sunday’s election. Newspaper Kathimerini reports:

“If New Democracy wins the elections, I will first meet with Alexis Tsipras to try to form a government,” Meimarakis said.

Questioned about potential alliances during Monday’s debate, Tsipras insisted that he believed Syriza would win an overall majority but that he would otherwise be prepared to form a “progressive” coalition. He ruled out an “unnatural” alliance with New Democracy, saying “We have radical differences on key issues.”

On that note it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow, counting down the hours until the Federal Reserve rate decision.

European markets move higher ahead of Fed meeting

Despite another bad day on the Chinese stockmarket, European shares managed to gain some ground, spurred by a positive early performance by Wall Street. Traders said the prospect of a rate rise in the UK this year diminished after inflation came in at zero, while uninspiring data from the US seemed to suggest the Federal Reserve may well hold off on raising borrowing costs later this week. However another theory for the rise was that the uncertainty about what the Fed planned to do would be ended if it actually acted and raised rates. So the final scores showed:

- The FTSE 100 finished up 53.01 points or 0.87% at 6137.60

- Germany’s Dax added 0.56% to 10,188.13

- France’s Cac climbed 1.13% to 4569.37

- Italy’s FTSE MIB rose 1.62% to 21,903.63

- Spain’s Ibex ended 0.89% higher at 9782.5

- In Greece the Athens market added 1.36% to 682.17

On Wall Street the Dow Jones Industrial Average is currently 175 points or 1% higher.

Updated

Markets may be moving higher today, but they are stuck in no-man’s land ahead of the US Federal Reserve meeting this week, says Chris Beauchamp, senior market analyst at IG:

Ahead of what looks like the most vital Fed meeting in years, the best thing for markets to do would be simply to sit still and wait for Thursday afternoon. With that being impossible, they have opted for the second choice, namely running around in circles.

A near 150-point range on the FTSE 100 today looks relatively busy, but in fact the index remains stuck within the range that has dominated all September. This is not an environment for long-term decision making, indeed so much is riding on Thursday’s events the market has become even more short-sighted than normal. Nonetheless, the longer the FTSE 100 remains stuck below 6200, the more it seems that the next big move is down. Despite the recovery off the lows of August, the index remains stuck in a downtrend, with so far little sign of a sustained comeback.

Undecided voters are #Greece's third largest party right now, polls show. Their last-minute choice will decide Sunday's election outcome.

— Maxime Sbaihi (@MxSba) September 15, 2015

Back with Greece, and Syriza’s government programme is out (here in Greek), five days before the election.

Updated

Here’s an interesting little graphic from the World Economic Forum:

What the world would look like if countries were the size of their #stockmarkets http://t.co/If6oi7R8rh pic.twitter.com/Bco7Rzcstc

— World Economic Forum (@wef) September 15, 2015

After Monday’s television debate in Greece between Syrza’s Alexis Tsipras and New Democracy’s Vangelis Meimarakis, comes a new ballot showing a marginal increase in support for the latter ahead of Sunday’s elections:

Greece: ND-EPP lead over SYRIZA in latest poll (Data RC). Important because of 50 seats extra for strongest party in #vouli. #debate

— twittprognosis/eu (@twittprognosis) September 15, 2015

Greece, Data RC poll: ND-EPP: 33% ↑ SYRIZA-LEFT: 32% ↓ PASOK-S&D: 7% ↑ XA-NI: 7% ↑ KKE-NI: 6% Potami-S&D: 6% EK-ALDE: 3% ↑ LAE-NI: 3% ↑

— twittprognosis/eu (@twittprognosis) September 15, 2015

Can't see NY Fed's Bill Dudley voting for a rate hike after those Empire Manufacturing numbers. #FOMC

— Michael Hewson (@mhewson_CMC) September 15, 2015

Wall Street has opened higher after the retail sales and industrial production data, but investors remains cautious ahead of the Fed meeting.

The Dow Jones Industrial Average is up 36 points or 0.24% in early trading, while European markets are also heading in the right direction, with the FTSE 100 up 0.3%, Germany’s Dax 0.26% higher and France’s Cac 0.54% better.

Another piece of weak US data, with industrial production falling 0.4% in August, adding to the evidence against a Federal Reserve rate rise.

This compares to forecasts of a 0.2% decline, and a 0.9% rise in July. Rob Carnell at ING Bank said:

US August industrial production was even softer than consensus expectations, falling 0.4% month on month, with manufacturing down 0.5% month on month (consensus = -0.3%).

Much of the weakness was in the vehicles sector, and when this is stripped out, production was flat on the month - still not great however, and this ex-vehicles segment has been flat, down or very weak for months now. If there are any bright spots, it is in utilities, which rose 0.6%, though mining put in another fall of 0.6%.

All in all, weak, disappointing, and taken together with other data earlier today - retail sales and Empire manufacturing, nudges the argument in the direction of the FOMC doves. With only consumer price inflation left to come before the September 17 meeting, and that likely to be on the low side, the data dependent Federal Open Market Committee might find the pendulum swinging a little more to the “no hike” side.

A no change from the Fed is not a universal opinion however.

Harley Bassman at investment group Pimco argues that the uncertainty of waiting for the Fed to raise rates is worse than the central bank actually lifting them slightly:

There are likely few market watchers who think that a 0.25% hike would have any real economic impact. (In fact, even a 1.0% funds rate would barely affect most businesses’ decision making processes since many commercial loans have a 1.0% floor.) Moreover, it is also clear that the U.S. economy has reached the limits of monetary policy stimulus.

What is unknown is the degree to which “animal spirits” are diminished by the endless drama of guessing when the Fed will finally start hiking.

Think about it: A 0% interest rate likely has little positive value and a 0.25% higher rate has little negative value, but the uncertainty, the anxiety of not hiking is significantly bothersome to all as this topic absorbs all the oxygen in the room – frankly, Hamlet debated less.

The full post is here:

Note to the Fed: Don’t Be Hamlet

Deutsche Bank’s chief US economist also cannot really see the Fed raising rates:

It is very hard to see a dovish #FOMC raising #Fed funds rate in an environment of skittish household and business confidence

— Joseph A. LaVorgna (@Lavorgnanomics) September 15, 2015

The US retail sales figures are among the last significant pieces of economic data before the Federal Reserve meets to decide whether or not to raise interest rates. The decision seems finely poised, with the recent volatility in China seen as a good reason for the Fed to hold off, at least temporarily.

As for the retail sales themselves, Rob Carnell at ING Bank reckons they will not be the evidence that finally decides the Fed to lift borrowing costs:

Though the figures, once adjusted for prior revisions, are roughly in line with consensus, this comes across as a fairly ordinary result, not one that will encourage any wavering [Fed] doves to switch their vote to a September hike.

...This would be a more convincing set of figures if one did not have to exclude all the weak parts to make the number look strong, and we don’t think the [Fed] members will be substantially moved by this data.

Separately, the latest Empire manufacturing survey for the New York region continued to languish at -14.67 only marginally improved from -14.92. Today’s data tally in total is at best neutral for the September Federal Open Market Committee, and probably a slight negative overall.

Updated

The US retail sales figures for August are out. And while they’re a little weaker than expected, they show that consumers are still spending.

Retail sales rose by 0.2% last month, the Commerce Department reports, missing forecasts of a 0.3% rise.

They were dragged down by lower spending at the pumps. Retail sales excluding gasoline rose by 0.4%.

BREAKING: US retail sales up 0.2% in Aug vs 0.3% increase expected http://t.co/h5p4IgiSLn

— CNBC Now (@CNBCnow) September 15, 2015

Updated

Greece election: Polarisation wins the debate

Over in Athens the talk of the town today ahead of Sunday’s general elections is all about last night’s debate between the two men now battling for the post of prime minister.

Our correspondent Helena Smith reports:

Who emerged victorious? Five days before potentially decisive polls for the country’s future, that is the question pundits and much of the Greek media are asking today.

Was it the leftist former prime minister Alexis Tsipras? Or was it Vangelis Meimarakis, the political veteran who has been the surprise winner of these elections so far, unexpectedly leading the pro-business, pro-European New Democracy to within a whisper of Syriza in the polls. Or even the debate itself? A debate that will go down as the tenth to be conducted before a poll, and this time in a way that allowed the protagonists to spar with each other openly (not literally, alas - Ed).

A good part of the media this morning unaminously agreed that it was polarisation – the inability of either the left or right to bridge differences enough to agree on anything substantial.

“The top televised debate rolled with zero consensus between Tsipras and Meimarakis,” Ta Nea proclaimed under the front-page headline “polarisation won.”

“The two political leaders insisted on [maintaining] a line of polarisation despite mention of consensus and collaboration, with the aim of rallying voters in the last stretch to elections.”

In that sense neither won – despite expections that the two-hour chin wag would sway the undecided (at 10% of the electorate, they will ultimately decide the outcome). When taken to task over implementation of the reforms set as the condition for a third EU backed bailout programme, both agreed they would enforce it – postehaste.

If anything, the debate marked the defeat of the anti-bailout front.

But analysts also agreed that in terms of polished performance Tsipras came out on top. “In substance Meimarakis [won], but visually Tsipras was a rock star,” said Dimitris Kerides, who teaches international politics at Panteion University.

Aristides Hatzis, professor of economics and law at Athens University concurred. “I think Tsipras emerged the winner. He unashamedly gave new promises and underplayed his compromises and especially his failures,” he told me, adding:

“Meimarakis put on an OK performance but he looked more uncomfortable especially when it came to criticising his own party.”

Whether Tsipras will be able to win over the young – appalled by the volte-face he has made embracing ‘neo-liberal’ policies – remains to be seen – and the young, along with women, account for most of those who remain undecided and have vowed to abstain from Sunday’s ballot.

Updated

French economists are manning the barricades today, protesting about the decision to appoint François Villeroy de Galhau as the next head of the Bank of France.

Around 150 of France’s finest economic experts have signed a letter arguing that Villeroy de Galhau is unsuitable as he served as co-chief operating officer of BNP Paribas until May.

In the letter, published in Le Monde today, they argue that this creates a serious conflict of interest. President François Hollande could and should have picked someone else.

“It’s not as if the president did not have a choice. It was entirely possible to promote, at the heart of the Bank of France, an internal candidate who is much less exposed to the risk of conflicts of interests.”

European Central Bank official Benoit Coeure was one option, although that would have deprived ECB president Mario Draghi of a key ally.

Draghi, incidentally, worked for Goldman Sachs before becoming Italy’s central bank chief in 2005. Mark Carney, the Bank of England’s governor, is also a Goldmanite. So Villeroy de Galhau won’t be treading a new path when he replaces Christian Noyer in November. But still, it’s an uncomfortable development.

We have a couple of pieces of eurozone data to flag up too.

Employment across the single currency bloc rose by 0.3% in the last quarter, as the region’s slow recovery continues.

Employment rose in 22 EU countries, and fell in just four, according to Eurostat.

Euro area employment +0.3% in Q2 2015, +0.8% compared with Q2 2014 #Eurostat http://t.co/2yfvanqWmd pic.twitter.com/sBHIb8Mq9D

— EU_Eurostat (@EU_Eurostat) September 15, 2015

However, confidence across German investors has shrunk sharply this month.

The ZEW future expectations index slid form 25 in August to 12.1 in September, suggesting pessimism is gripping Europe’s largest economy.

German Investor Confidence Damped by Weaker Emerging Markets http://t.co/5ygzMFPdoy pic.twitter.com/iw4Mjt3NK6

— Bloomberg Markets (@markets) September 15, 2015

Updated

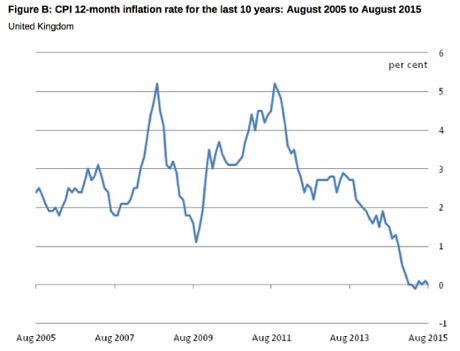

Summary: Fuel pulls UK inflation down to zero

Over to my colleague Katie Allen to round-up today’s inflation data:

Sharp falls in petrol and diesel pulled UK inflation back down to zero last month as tumbling crude oil prices trickled down to households.

Official figures showed inflation on the consumer prices index edged back down to 0.0% in August from 0.1% in July, continuing the trend since the start of this year of virtually no year-on-year rise in living costs. Inflation has been below the Bank of England’s 2% target for the past 20 months.

Economists said the lack of inflation would continue to boost consumer spending, the main driver of economic growth in the UK.

“This period of noflation or lowflation – whatever you want to call it – has undoubtedly been good news for the UK. The falling price of essentials has come at the same time as a rapid acceleration in wage growth since the start of the year, boosting discretionary spending power,” said Scott Corfe at the Centre for Economics and Business Research thinktank.

The headline figure was in line with the consensus forecast in a poll of economists by Reuters. But some had been expecting cheaper fuel to nudge inflation down to -0.1% or even -0.2% , marking a return to the negative territory hit in April this year when prices fell for the first time in more than 50 years.

As a result, the pound strengthened against the dollar after the data, as some traders wagered it left the door open for the Bank of England to start raising interest rates after more than six years at a record low of 0.5%......

Here’s her full story:

Here’s a handy colour-coded graph showing how UK inflation has fluctuated since the financial crisis began:

0% inflation in the UK in August. Food, transport and more recently clothing have helped drag it down. pic.twitter.com/X8vejuEekc

— RBS Economics (@RBS_Economics) September 15, 2015

The cost of oil and metals has fallen through the summer, as concerns has grown over China’s economic slowdown.

And for that reason, Ranko Berich of City firm Monex Europe fears UK inflation could fall further, especially if the global economy worsens.

He argues:

“The downside risks to inflation are now mounting, with the latest falls in commodity prices adding more volatility to the global economy. The general consensus at the Bank is that energy prices will at least stabilise, so if crude oil prices take another hit the UK economy could be in for a bumpy ride.

With this report showing no sign of labour market gains filtering through to higher consumer prices, the Bank of England’s extreme caution around rates now seems entirely justified.”

Inflation (CPI) up 0% Wages up 2.5% Houses up 5.2%. Can you tell how this ends yet?

— Henry Pryor (@HenryPryor) September 15, 2015

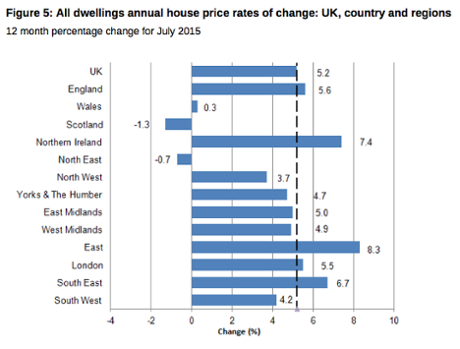

This era of no-flation does not extend to Britain’s housing market.

Property prices jumped by 2% in July alone, meaning house price inflation is running at over 5%.

Money editor Patrick Collinson explains this morning’s data:

The average house price rose by more than £1,000 a week, leaping from £277,000 to £282,000, a new all-time high and 16.7% above the pre-financial crisis peak in 2007.

But on a seasonally-adjusted basis, average annual house price inflation dipped to 5.2% from 5.7%, in part due to price falls in Scotland and the north-east of England.

And here’s the picture across Britain’s regions:

Updated

The British Chambers of Commerce disagrees with the Institute of Directors, and wants the Bank of England to leave interest rates unchanged.

Chief economist David Kerr argues that Britain’s economy isn’t robust enough to handle a hike.

“Low inflation supports living standards by boosting disposable income and will help to sustain the economic recovery. However, last week’s poor trade and manufacturing figures show that the recovery is still fragile, particularly in the face of major global uncertainties.

“The prospect of continuing low inflation and global uncertainty should give the MPC no need to contemplate a premature increase in interest rates. We urge the MPC to keep rates at their current level until well into 2016.”

Updated

TUC: Zero inflation doesn't deliver higher living standards

The TUC’s general secretary, Frances O’Grady, argues powerfully that the Bank of England should not raise interest rates right now.

“Zero inflation is not a route to raising living standards. And with future economic prospects so uncertain, early interest rate rises would bring real risks to households.

“The recovery can’t be taken for granted and we need significant investment in skills, innovation and infrastructure to boost productivity and ensure a sustainable economy that works for the many and not just the few.”

Today’s drop in inflation hasn’t deterred the Institute of Directors from repeating its call for interest rates to rise.

Michael Martins, the IoD’s economic analyst, argues that Britain’s economy looks healthy despite the problems in China and the eurozone. And with inflation at zero, households are benefitting from rising real wages and higher spending power.

Thus, the time to start normalising rates has arrived (even though there’s no immediate need to hike borrowing costs to tame inflation):

Given the strength of the UK economy, pickup in output, tightening labour market, and tentative signs of productivity increases, the Bank of England must be prepared to follow the Federal Reserve if it raises rates on Thursday.

I suspect the IoD are ahead of the curve on this one, with most City economists predicting rates will remain low until 2016. But we shall see....

Updated

The Treasury: Zero inflation is good news

The government has welcomed today’s inflation report, even though it shows the Bank of England is failing to hit the 2% target.

A Treasury spokeswoman says:

Today’s inflation figure means a real boost for working people and family budgets across our one nation, with prices essentially frozen compared to last year while wages continue to rise.

This is a reminder that we must continue to work through our long term plan to build a resilient economy – delivering the economic security of a country that lives within its means, financial security of lower taxes and a new National Living Wage, as well as national security of a Britain that defends itself and its values.”

It’s a bit of a leap from cheaper petrol prices to the Security of the Nation. But this is now one of the government’s new attack lines at Labour’s leader, Jeremy Corbyn.

Inflation is expected to remain flattish for the next few months.

Consumer price inflation will likely continue to hover around zero in September & October but still looks likely to then trend up gradually

— Howard Archer (@HowardArcherUK) September 15, 2015

Not quite back to deflation but inflation at zero and likely to stay close to there for a while.

— David Smith (@dsmitheconomics) September 15, 2015

Analyst: it's no-flation, not deflation

This latest drop in inflation is due to “the slump in the oil price, a washed out summer keeping shoppers away from the high street, falling sea fares and the ongoing supermarket price wars”.

So says Maike Currie, associate investment director at Fidelity Personal Investing, who isn’t too worried about the deflation threat.

“It is important to distinguish between disinflation - a slowdown in the rate of inflation; and deflation – a persistent and ongoing fall in prices. The two are not the same thing.

Both food and fuel - the main drivers of the historically low inflation numbers we are seeing - are two essential items. No-one is going to delay their weekly trip to the supermarket or stop filling up their car’s petrol tank, because they expect prices may fall next month.

Deflation is dangerous because it causes companies and consumers to do the exact thing that causes more deflation – delay spending in the hope of further price falls in the future.”

Inflation has now been flat or negative for five out of the past seven months, far from the Bank of England’s 2% inflation target.

The BBC’s economics editor, Robert Peston, wonders if Britain is entering a protracted period of very weak inflation, or worse....

Since February, inflation has been 0%, 0, -0.1, 0.1, 0, 0.1,0. When is it reasonable to worry that deflation is a genuine threat?

— Robert Peston (@Peston) September 15, 2015

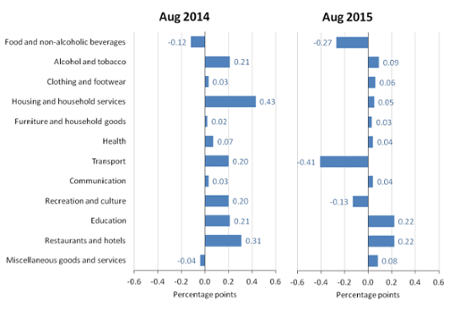

UK inflation, the key chart

This chart confirms that cheaper food and transport costs kept inflation pegged at zero over the last year.

Although Britons did benefit from a smaller rise in clothing prices in August, that’s partly because shops offered less generous discounts in the July sales.

The ONS says:

Clothing prices, overall, rose by 1.5% between July and August this year compared with a rise of 2.6% between the same 2 months a year ago. Prices of clothing and footwear usually rise between July and August as autumn ranges start to enter the shops following the summer sales season.

The smaller rise this year follows a sales period in which prices fell by less than a year ago. The downward contribution came from price movements across a range of garments but particularly from women’s outerwear.

Food prices across the UK have fallen by 2.8% over the last year, according to today’s inflation report, while motor fuel is 12.9% cheaper.

The Bank of England is probably relieved that UK inflation didn’t turn negative for the second time this year.

Did I hear a big sigh of relief by the Old Lady on Threadneedle St? #boe #cpi

— Mike van Dulken (@Accendo_Mike) September 15, 2015

UK core inflation in line at 1%. So nothing in inflation to adapt #BoE wait and see stance....

— Joshua Raymond (@Josh_RaymondUK) September 15, 2015

Inflation in the UK was held back by clothing prices, which rose at a slower pace this summer.

The Office for National Statistics says:

A smaller rise in clothing prices on the month compared with a year ago was the main contributor to the slight fall in the rate. There were also downward effects from changes in motor fuel prices and sea fares. Rising prices for soft drinks and for furniture and furnishings partially offset the fall.

UK inflation hits zero

The UK’s annual inflation rate, the consumer prices index, has fallen back to zero.

That’s down from 0.1% in July.

The cost of living was pulled down by lower oil prices, the Office for National Statistics reports.

Prices were 0.2% higher in August than in July, but unchanged compared with August 2014.

And the core inflation rate, which strips out volatile factors such as energy and food prices, has dropped to 1% from 1.2%.

More details and reaction to follow

Updated

Europe’s stock markets are following China’s lead lower.

After a solid start, the FTSE 100 has now shed 52 points or almost 1%. Commodity firm Glencore is the biggest faller, down 6.3%, tracking a drop in metals prices.

#FTSE really tanking now as metals prices fall. TM pic.twitter.com/J1z56VMhoG

— IGSquawk (@IGSquawk) September 15, 2015

More on this after the UK inflation data.....

It’s nearly time for the main economic data of the morning, the UK inflation figures for August.

Analysts, economists and investors are all watching closely, to see how the consumer prices index changed last month.

Tony Cross of Trustnet explains:

These numbers have the ability to influence interest rate decisions – expect the Bank of England to be looking at the core rate excluding food and fuel prices

Today’s selloff suggests Chinese investors aren’t confident that Beijing can successfully stimulate its economy, and pump up the stock market boom again.

IG’s market strategist Bernard Aw says:

“Normally, expectations of more growth boosting action would lead to demand for smaller and speculative stock, like the ChiNext or Shenzhen Composite Index, but today, market participants were probably not convinced that there will be a big plan in the pipeline.”

Chinese authorities may be relieved that the Shanghai stock market didn’t finish the day below the 3,000 point mark today.

At one stage, the Shanghai Composite hit 2,984 before struggling back. Perhaps with some assistance?...

China shares fell again today with the Shanghai Composite falling 3.5% to 3004. The Plunge Protection Team held 3000 just!

— Shaun Richards (@notayesmansecon) September 15, 2015

Shanghai Comp. falls below 3,000; -4%; 14 stocks fall for every 1 that's up

— David Ingles (@DavidInglesTV) September 15, 2015

Updated

Shanghai stock market tumbles 3.5%

Back in China, the stock market has posted its biggest two-day fall in three weeks.

The Shanghai Composite Index closed for the day down 3.5% at 3004 points, meaning it has now lost 7% of its value this year.

Commodity producers and technology companies led today’s selloff, which takes the index back towards the eight-month low reached last month.

Economists are concerned that the Chinese economy is weakening rather faster than the official data, which shows growth of around 7% this year .

Energy consultancy Wood Mackenzie says its research suggests the Chinese economy grew at an annual rate of 5.3% in the second quarter of 2015, and just 4.5% in Q3.

There is also concern that recent interventions by Bejing have not revitalised the markets.

As Zhang Haidong, chief strategist at Jinkuang Investment Management, put it:

“The economy has not shown signs of a pick up after a series of cuts in interest rates and reserve requirements, while expectations about yuan depreciation are still there.”

BMW has now told reporters that CEO Harald Krüger has seen a doctor and is recovering well.

The company added that this morning’s moment of dizziness follows a recent trip abroad.

Updated

Here’s Bloomberg’s early take on events in Frankfurt:

BMW AG suspended a press conference at the Frankfurt International Motor Show after Chief Executive Officer Harald Krüger collapsed on stage.

The CEO, 49, was escorted offstage by two assistants after the incident. The event was Krüger’s first appearance at the Frankfurt show as BMW’s chief. He took the top post at the Munich-based carmaker in May.

DEVELOPING: BMW suspends news conference at Frankfurt Motor Show after CEO Harald Krueger collapses http://t.co/pOIYeJbaRX #IAA2015

— Bloomberg Business (@business) September 15, 2015

Updated

BMW boss collapses at Frankfurt Motor SHow

There’s drama over in Frankfurt, where the CEO of German carmaker BMW has just appeared to faint during a presentation at the Motor Show.

A planned press conference was cancelled after Harald Krüger fell to the ground during a presentation on stage. He did then walk away after being helped to his feet, so hopefully he’s OK.

Reuters has the story:

German luxury carmaker BMW’s new chief executive, Harald Krüger, fainted on stage at the Frankfurt auto show on Tuesday, a Reuters witness reported.

Krueger collapsed as he was commenting on BMW’s latest models during a news conference. Two men escorted him off stage. Kruger was able to walk.

A BMW spokesman said over the public address system: “I’m a bit lost for words. BMW will try to redo the press conference at a later stage.”

Automotive journalist Jonathan Brownfield is there, and confirm that the press conference is off:

First stop was #BMW. Unfortunately, the CEO fell during the first part of the conference, so the rest was canceled. #IAA2015

— Jonathan Brownfield (@JonathanReviews) September 15, 2015

Updated

Quiet session in the US last night, dull markets ahead of the Fed on Thursday means FTSE forecast to start broadly unchanged at 6085

— David Jones (@JonesTheMarkets) September 15, 2015

The recent drop in the oil price probably helped to keep the cost of living pegged in August.

My colleague Katie Allen explains:

The headline inflation rate is forecast to edge down to zero for August from 0.1% in July, according to the consensus in a Reuters poll of economists. Some even see inflation on the consumer prices index (CPI) measure turning negative again after a sharp fall in crude oil prices and a supermarket price war cut the cost of petrol and diesel.

“Our forecast for August is that the headline measure of CPI inflation fell back to 0.0%, but there is a significant risk that it heads back into negative territory,” said Philip Shaw, economist at Investec.

Here’s Katie’s preview of the data, due at 9.30am BST:

BAML also found that few investors expect the Federal Reserve to announce an interest rate hike this week.

A majority expect the Fed to act before the end of the year, though.

Rate hike expectations have shifted to 4Q (BAML FMS) pic.twitter.com/XqFdgUfWW6

— Lady FOHF (@LadyFOHF) September 15, 2015

Chinese recession is top 'tail risk'

City investors are increasingly concerned about the possibility that China’s economy falls into recession, according to the latest survey by Bank of America Merrill Lynch.

They’ve stopped fretting about the eurozone, though.

China recession and EM debt crisis viewed as the biggest tail risks (per BAML) pic.twitter.com/ziTAVf9B7W

— Lady FOHF (@LadyFOHF) September 15, 2015

China’s stock market is on track for its worst two days since the drama of late August.

Another wave of selling has swept through the country’s trading floors today, as investors fret about recent disappointing economic data.

This has send the Shanghai composite index down by over 3% in late trading, adding to yesterday’s 2.7% decline. There’s still around 30 minutes left, though, so we could see the authorities intervene to prop up shares.

Shanghai is having another tough session. It's the biggest 2 day drop in 3 weeks. pic.twitter.com/kHNnCe5Gjf

— Guy Johnson (@GuyJohnsonTV) September 15, 2015

Updated

Introduction: UK inflation likely to be weak

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Inflation is one of the issues of the moment, as central bankers in Britain and America ponder whether it’s safe to end the long period of cheap money and start raising interest rates.

And we get a new healthcheck on the UK situation today, when the latest consumer prices index (CPI) is released.

Economists reckon that inflation could fall back to zero, from just +0.1% in July. It could even be negative.

Latest UK inflation figs out at 09:30 and we might be back in deflation territory. The gap between wages and prices still widening. Hurrah

— Johny (@johnycassidy) September 15, 2015

Michael Hewson of CMC Markets predicts that today’s inflation report will give little support to those who favour hiking borrowing costs soon:

August inflation is set to remain weak with annual CPI set to fall back to 0% from 0.1% in July. Even more importantly core CPI inflation is also expected to fall furtherfrom 1.2% in July to 1%.

Retail prices (RPI) are also set to decline further as well, below the 1% level to 0.9% as lower fuel and clothing prices weigh on prices.

Good news for UK consumers, if so.

Here’s today’s economic calendar:

-

9.30am: UK inflation data

-

10am: German ZEW economic sentiment survey

-

10am: Eurozone Q2 unemployment survey, and trade balance for July

- 1.30pm: US retail sales for July

Spread-betters are predicting a subdued start to trading in London:

Our European opening calls: $FTSE 6100 up 16 $DAX 10166 up 34 $CAC 4540 up 22 $IBEX 9725 up 29 $MIB 21607 up 53

— IGSquawk (@IGSquawk) September 15, 2015

Companies reporting results this morning include online supermarket Ocado, and the DIY chain Kingfisher.

And we’ll be keeping one eye on Greece, ahead of Sunday’s general election, and other events through the day....

Updated