Summary: US manufacturing flatlines, China struggles and UK rebounds

Time for a summary after a raft of manufacturing reports from around the world.

In the US, the Markit PMI was revised higher but the Institute for Supply Management’s (ISM) index of US factory activity suggested growth almost ground to a standstill last month.

Employment in the sector fell, according to the ISM survey, prompting some expectations of a gloomy picture when the closely watched non-farm payrolls report on the US labour market is published on Friday. With markets seizing on downbeat news as positive for shares, because it is seen cutting the chances of a US rate hike in December, Wall Street extended gains after the manufacturing report.

October was a mixed month overall for global manufacturing. China’s malaise continued, with activity shrinking for the eighth month in a row. Economists say it means Beijing may need to cut interest rates again soon, to prop up demand.

The UK smashed forecasts, with growth hitting its fastest rate in 16 months. Some analysts couldn’t quite believe the numbers, and argued that the underlying picture was less healthy.

The Eurozone had a rather subdued month - with growth in Germany and Spain slowing, and French factories posting little growth. Italy did surprisingly well, though.

Over in Athens, Greek bank shares jumped after stress tests showed they “only” need €14.4bn in new capital....

...while students are protesting about education cuts.

Britain’s biggest bank, HSBC, noted a reduction in income from overdraft fees as it reported a rise in profits but drop in revenues. The bank also warned it may delay until next a year its decision on whether to remain based in London.

In other banking news, the UK’s high street banks are each in line for multimillion-pound windfalls from the sale of Visa Europe in a deal valuing the credit and debit card company at €21.2bn (£15bn)

And the Turkish stock market and lira have both jumped after Recep Tayyip Erdoğan’s party won last night’s general election. Investors welcomed the decisive result, even though it may lead to more discontent among opposition supporters.

On that note, we’ll close up for the evening. Thanks for all your comments, and we’ll be back again tomorrow.

Obama signs US budget bill

President Barack Obama has highlighted his hope that the US will be spared eleventh-hour government shutdown threats as he signed a new budget bill today.

By signing into law the pact agreed last week by Congress, Obama also averts the threat of a default on US government debt.

The US Congress reached the two-year budget agreement in a rare bipartisan breakthrough. The pact takes volatile issues like the debt limit and government funding off the table until after the 2016 presidential election, thus paving the way for soon-to-be speaker of the House Paul Ryan to ease into his new role as John Boehner resigns from Congress.

Reuters reports that in a brief signing ceremony in the Oval Office, Obama noted lawmakers would still need to pass spending bills, but said he was confident they could get them done on time, and that the bill should free the nation from last-minute government shutdown threats.

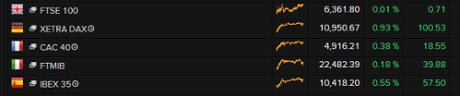

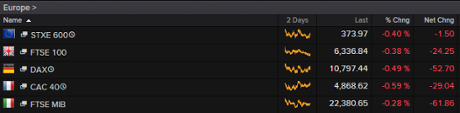

European markets have now closed and most main indices have got off to a solid start to November.

Only London’s FTSE 100 is left behind, flat at 6,362 after gains for banking stocks were offset by weaker miners in the wake of more downbeat manufacturing data out of China.

Here’s how the main indices finished the day:

In the US, stock markets are also higher.

Banks to get Visa Europe windfall

Sticking with financial services, the UK’s high street banks are each in line for multimillion-pound windfalls from the sale of Visa Europe in a deal valuing the credit and debit card company at €21.2bn (£15bn).

Owned by thousands of lenders, Visa Europe is being sold to its one-time sister company, Visa Inc, which was floated on the US stock market in 2008. The UK’s main banks could receive up to £1bn between them, reports Jill Treanor.

She writes:

The deal sparked a flurry of stock market announcements from the lenders that had to reveal their profits. Barclays expects to make £400m and bailed-out banks Lloyds Banking Group and Royal Bank of Scotland £300m and £200m respectively. HSBC’s profit was estimated at £150m.

Chirantan Barua, analyst at Bernstein Research, warned the benefits might not be long-standing: “Although we see this as a positive in the short term for the UK banks as this represents a boost to capital we do not see this as a free lunch. Now that the banks will be ‘external’ to the payment system they will see their fee income margin start to be squeezed and we wouldn’t be surprised if Visa tried to increase the margins in Europe at the expense of the banks.”

Worldpay, the payments company recently floated on the London Stock Exchange, said it expected to receive €1.2bn.

There are more than 500m Visa cards issued across Europe and the deal is being announced – after years of speculation – at a time when new regulations will cap fees that banks can charge retailers for debit and credit card use. A rise in the use of cards is also expected in the years ahead and this would allow Visa to compete more effectively with Mastercard.

The full news story:

Elsewhere in the banking sector, Barclays has agreed to pay out $94m to settle US antitrust lititgation by investors, Reuters reports.

According to the news service, the UK-listed bank was among 11 banks accused by investors of conspiring to manipulate the benchmark European Interbank Offered Rate (Euribor) and related derivatives. Barclays is the first defendant to settle, according to court papers.

Reuters continues:

Kenneth Feinberg, a prominent mediator who helped broker the accord, said in an affidavit “this first and early settlement with Barclays provides plaintiffs with a precedent and settlement structure that may encourage other interested defendants to settle.”

Barclays’ preliminary settlement requires court approval.

Other defendants include BNP Paribas SA, Citigroup Inc, Credit Agricole SA, Deutsche Bank AG , HSBC Holdings Plc, JPMorgan Chase & Co , Rabobank BA, Royal Bank of Scotland Group Plc , Societe Generale SA and UBS AG. The electronic broker-dealer ICAP Plc is also a defendant.

The full story is here.

HSBC caused a political storm in April when it announced it was considering whether to keep its headquarters in London. Stuart Gulliver, the chief executive, has previously said the decision would be known by the end of 2015 but now it seems the wait may be longer.

My colleague Jill Treanor has been reporting on the bank’s results today and HSBC’s comments that it may delay a decision on whether to remain based in London until next year.

Here is a flavour of Jill’s updated story following HSBC’s delayed conference call.

As the bank announced results for the first nine months of the year, it said a decision might take longer. “An announcement will be made when the board makes its final decision and, if necessary, a further update will be provided at the time of the full year results,” the bank said.

Douglas Flint, the HSBC chairman, said the board had requested additional information as part of the review. He said the decision would be based “on long-term perspectives rather than short-term factors”.

“We take it very seriously and give it the appropriate amount of work,” said Flint, who was speaking from China, where the bank had just sealed a deal to create a securities trading venture in Shenzhen. “We are halfway through.”

The bank has been linked with a series of alternative locations in addition to Hong Kong, including the US and Canada. Since HSBC announced its review, the British government has made changes to the taxation of banks that are regarded as preferable to HSBC. It has also clarified parts of the regulatory regime that had been concerning the bank.

Ian Gordon, an analyst at Investec, said: “We think that HSBC should move ahead with a re-domicile out of the UK as soon as possible.” Despite the reduction in the bank levy announced by George Osborne in July, Gordon said HSBC was still expecting to pay $1.6bn (£1bn) towards the levy, which is based on the size of bank balance sheets in 2017.

The full story:

Shares in HSBC are down almost 1%, or 4.3p, at 503.1p. They are down 17% from the start of the year.

Updated

On Wall Street, traders appear to have latched onto to the downbeat tone of the latest manufacturing report, which pointed to a drop in employment last month.

US non-farm payrolls numbers due on Friday will be all important to how the Federal Reserve judges the state of the labour market but in the meantime, this week reading from an admittedly small sector of the US economy is seen as reducing the chances of a December rate hike.

The Dow Jones industrial average has extended earlier gains to be up around 100 points at 17,764.

The tech-heavy Nasdaq is up 36 points at 5,090.

The S&P 500 is up 10 points at 2,089, having been flat at the open before the manufacturing reports.

In the UK, where a manufacturing report earlier signalled a rebound in output and orders, the FTSE 100 down, but only by one point, at 6360.

Connor Campbell, financial analyst at spread-betting firm Spreadex has been following US reactions:

It appears that investors took the negative news to heart, lifting the Dow Jones to near 3-month highs as November’s first piece of crucial information (in what is going to be a month full of over-scrutinised data) arguably dealt a blow to the Fed’s hopes of raising rates in December. The fervour around US news is only going to increase in importance as the week goes on, with factory orders, Markit and ISM services PMIs, a testimony from Janet Yellen and, of course, Friday’s non-farm jobs report still to come.

The Institute for Supply Management (ISM) highlights various headwinds in its report showing a slowdown in US manufacturing growth in October.

Comments from the panel reflect concern over the high price of the dollar and the continuing low price of oil, mixed with cautious optimism about steady to increasing demand in several industries.”

Reacting to the report, which just beat expectations but showed barely any growth last month, James Knightley, economist at ING Financial Markets says there are possible implications for the closely watched US non-farm payrolls report due on Friday:

The details are very mixed. Both new orders and production improved to stand at 52.9, but employment fell to 47.6 from 50.5. By falling into contraction territory (sub-50) this suggests some downside risk for Friday’s jobs number, although manufacturing is dwarfed by the service sector in terms of overall employment and a stronger non-ISM figure would raise optimism once again.

It is clear that the manufacturing sector is going to continue to underperform non-manufacturing given that dollar strength and external demand weakness are clear drags for the sector. However, we are more hopeful for the service sector while construction spending grew 0.6% month-on-month. As such, the US economy in aggregate should perform better in the fourth quarter than the disappointing third quarter reading of 1.5% annualised. This will keep thoughts of a December Fed rate hike alive.”

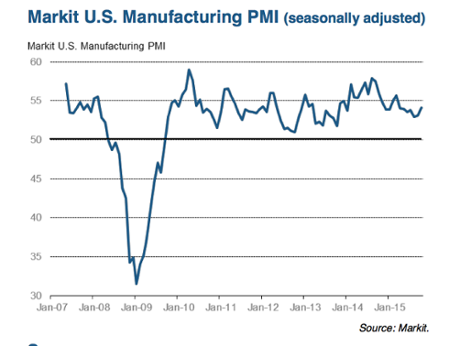

US ISM report points to slower factory growth

Hot on the heels of Markit’s US manufacturing PMI, a separate report paints a somewhat gloomier picture of the sector’s fortunes in October. The Institute for Supply Management’s (ISM) index of US factory activity suggests growth slowed last month, holding at its weakest level since May 2013.

The index dipped to 50.1 from 50.2 in September. That left it only just in expansion territory - as with the PMI, 50 is the dividing line between expansion and contraction. The forecast in a Reuters poll of economists was for 50.0.

The report’s jobs index fell to the lowest level since the downturn days of mid-2009 and at 47.6 was below the key 50-mark for the first time since April this year.

More details and reactions to follow soon...

Updated

US manufacturing PMI rises

Chris Williamson, chief economist at survey compilers Markit says the latest manufacturing report is encouraging after growth slumped in the third quarter of this year.

He notes that companies reported the largest monthly jump in new order inflows since March. Export growth had also revived, suggesting firms were managing to adapt to the stronger dollar, as job creation picked up after slowing in September, he added.

On what it means for US interest rates, Williamson commented:

With the Fed eagerly watching the data flow to see whether the third quarter economic slowdown will intensify, the improvement in the manufacturing sector increases the odds of policymakers voting to hike rates at the FOMC’s December meeting.

“However, with inflationary pressures remaining very subdued and signs of the slowdown persisting into the fourth quarter in the larger service sector, the policy outlook is by no means certain and debate about whether the economy yet needs higher interest rates will no doubt remain intense.”

The Institute for Supply Management’s (ISM) index of national factory activity is out shortly.

Updated

US manufacturing PMI revised higher

US manufacturers enjoyed slightly faster growth in October than previously thought, according to the latest PMI report from Markit.

Its main index of factory performance has been revised up to a six-month high of 54.1 from a previous estimate of 54.0 for October and compared with 53.1 in September. It was well above the 50-mark that separates expansion from contraction.

The survey compilers said the figure represented a “modest rebound in US manufacturing performance”, driven by faster rises in output, new orders and employment levels. The index pointed to the sharpest improvement in overall business conditions since April.

Markit’s press release with more details can be found here, and here’s the pdf.

US stock markets have opened slightly higher, with investors anticipating some weak manufacturing numbers out shortly, which would be seen as cutting the chances of a rate hike before year end. That’s right, as we reported earlier, markets are in one of those bad=good phases when it comes to US economic news.

Whether it works both ways remains to be seen. But there is a fair chance that an upside surprise in one or both of the manufacturing surveys from the US this afternoon will mean shares fall back because the chances of a rate rise are seen to increase.

The Dow Jones industrial average is up 42 points to 17,705, the Nasdaq is up 13 points at 5,066 and the S&P 500 was just 2 points higher at the open at 2,081.

Updated

HSBC has reported its latest financial results today and as we covered earlier Britain’s biggest bank said profits were up because of a fall in fines and legal costs.

But revenues were down and my colleague Jill Treanor has been looking into one of the causes: a reduction in income from overdraft fees.

Jill reports:

Customers of HSBC and First Direct saved $135m (£85m) in overdraft charges after the bank started sending text messages to warn them they were about to go into the red.

The bank started sending texts to its customers a year ago, alerting them when they risked incurring charges for unauthorised overdrafts. In the first month, it sent 1.2m texts and by September this year the number had risen to 1.5m.

The bank found that 72% of First Direct customers sent the alerts were able to avoid fees as were 50% of those of its high street network HSBC.

The bank charges £5 a day for customers with unauthorised overdrafts and caps the monthly fee at £80. This charging structure has been in place for a year and replaced the £25 fee charged each time a customer slides into the red.

The full story:

As ‘manufacturing Monday’ continues, investors are now looking ahead to data due out of the US. The backdrop for numbers is markets in full-on “will they, won’t they” debate over the prospects of a rate hike from US Federal Reserve next month.

The US PMI report by Markit - the group behind the European ones published earlier today is out at 14.45GMT and then the Institute for Supply Management’s (ISM) index of national factory activity is out at 15.00GMT.

The Fed has certainly left the door very much open to a hike while insisting, as usual, that what matters mores than its own guidance is how the data plays out. What that could well mean for markets is that any weaker data is taken as a positive because it reduces the chance of a hike.

Looking ahead to the manufacturing data, Connor Campbell, financial analyst at spread-betting firm Spreadex explains further:

Still to come are the USA’s own manufacturing figures; the official figure is expected at a stable 54, whilst the ISM number is forecast to fall slightly from 50.2 to a teetering even closer to contraction 50. The spectre of a weak number appears to be lifting the Dow, if only just, ahead of the US open, the index edging up by around 12 points. Following the surprisingly hawkish FOMC statement last week US data is arguably back to the old good is bad/bad is good trend that has defined 2015, something that will get a full workout this week as non-farm Friday approaches.

Summary: Chinese manufacturing struggles, but UK picks up

Time for a recap.

October was a mixed month for global manufacturing, according to a flurry of data released this morning.

China’s malaise continued, with activity shrinking for the eighth month in a row. Economists say it means Beijing may need to cut interest rates again soon, to prop up demand.

The UK has smashed forecasts, with growth hitting its fastest rate in 16 months.

Some analysts can’t quite believe the numbers, and argue that the underlying picture is less healthy.

The Eurozone had a rather subdued month - with growth in Germany and Spain slowing, and French factories posting little growth. Italy did surprisingly well, though.

Over in Athens, Greek bank shares have jumped after stress tests showed they “only” need €14.4bn in new capital....

...while students are protesting about education cuts.

And the Turkish stock market and lira have both jumped after Recep Tayyip Erdoğan’s party won last night’s general election. Investors welcomed the decisive result, even though it may lead to more discontent among opposition supporters.

Updated

Greek students have taken to the streets today, to protest against government cutbacks that are harming their education.

These photos just arrived, showing a solid turnout as students shout slogans against the government and its plans to cut the education budget:

The Kathimerini newspaper has more details:

School pupils demonstrated in the central Athens on Monday, demanding improved learning conditions. According to authorities, tensions rose when a group of youngsters hurled stones at police forces.

The rally, which was organized through the Internet, was billed as “warning” action, with youngsters protesting against staff, books and infrastructure shortages, among others.

Also on Monday, the union representing secondary school teachers, OLME, was holding a three-hour stoppage running through 2 pm [local time].

Many schools failed to open for the start of the autumn term, due to staff shortages. One report says Greece needs 21,000 extra teachers.

That could have really serious consequences for young Greeks, who can’t be blamed for any of the country’s deep-seated problems.

Prime minister Alexis Tsipras’s children should be OK, though - their left-wing father recently dispatched them to one of Athens better private schools....

Updated

China’s manufacturing sector passed a significant milestone today - with the unveiling of its first ever homegrown passenger jet.

The C919 rolled smartly off the assembly line in Shanghai, to be admired by the assembled crowd.

The Communist party’s official mouthpiece newspaper, the People’s Daily, declared the accomplishment “an historic breakthrough”, as my colleague Tom Phillips reports:

The development of China’s first large passenger jet has huge symbolic value for the Communist party as President Xi Jinping pursues what he calls the “great rejuvenation of the Chinese nation”.

“A great nation must have its own large commercial aircraft,” Li Jiaxiang, the head of China’s civil aviation authority, told those invited to the plane’s unveiling ceremony, according to Bloomberg. “The air transportation industry of China cannot completely rely on imports,” he said.

However, the twin-engine C919 jet won’t be delivered to airlines for at least another three years, having originally been aiming to hit the skies next year.

Here’s the full story:

Updated

Noted....

HSBC CEO Stuart Gulliver: "For those of you who write diary columns, this was nothing to do with HSBC’s IT"

— Tim Wallace (@Tim_Wallace) November 2, 2015

We’ll have more details from HSBC’s (delayed) call later....

Greek bank shares jump after stress test results

Shares in Greek banks have jumped this morning, after new official tests showed that they needed slightly less new capital than expected.

Eurobank, Alpha Bank and Piraeus Bank are all up over 10% this morning, with Athens traders calculating that the stress test results could have been worse.

The ECB announced on Saturday that Greece’s banking sector needs €14.4bn of fresh funds, to cover a jump in bad loans during this year’s debt crisis.

A serious sum, but below the €25bn allocated to the sector in the bailout deal agreed this summer. This could encourage investors to put money back into the sector.

Piraeus bank was told to raise almost €5bn of new capital, followed by the National Bank of Greece €4.6bn, Alpha Bank €2.7bn and Eurobank €2.1bn.

The clock is ticking -- the banks want to raise this funds before new rules are implemented in 2016, which would allow large depositors to be ‘bailed in’.

And this doesn’t mean that the Greek banking sector is fixed, as analyst Silvia Merler writes for Bruegel:

First, the biggest source of risk for the Greek banks may still be not accounted for. The exercise does not deal with Greek banks’ reliance on sizable Deferred Tax Assets (DTAs). For some banks, these make up about 50% of CET1..

DTAs are by no means used by Greek banks only, and the issue is ultimately rooted in the definition of capital in our regulatory framework, so it would make absolutely no sense for the ECB to change the rule only for Greek banks in this exercise. Rather than solving the problem, this would delay finding a solution.

NEW | @SMerler on the results of @ECB stress test of major #Greek banks https://t.co/TPVbjmegZ6 pic.twitter.com/aJ4Wi7iEGJ

— Bruegel (@Bruegel_org) November 2, 2015

The slump in Greece’s factory sector has almost bottomed out, according to today’s data from Markit.

The Greek manufacturing PMI jumped to 47.3 last month, a five-month high, having slumped to almost 30 this summer.

Greece's manufacturing PMI has now totally erased the big plunge from this summer's events. pic.twitter.com/AOabKPSj5G

— Joseph Weisenthal (@TheStalwart) November 2, 2015

But although the downturn eased, Greek manufacturing did still deteriorate further.

Firms reported that new orders were down again, while job cuts continued.

Not a surprise, given capital controls make it hard for companies to trade abroad:

HSBC has suffered a nasty attack of gremlins.

The banking giant is due to be holding a conference call with investors and analysts now, to discuss its latest results.

But the call has been stricken by a technical glitch that has stopped anyone - including the bank itself - from dialling in.

Suspect HSBC will be looking for a new conference call provider as everyone, including HSBC, is locked out of their Q3 media results call

— Tim Wallace (@Tim_Wallace) November 2, 2015

Those results showed a 32% increase in profits in last quarter, to $6.1bn, mainly due to smaller bill for compensation and fines (welcome to modern banking!)

There’s also no progress on whether HSBC will move its headquarters out of London, as our City editor Jill Treanor reports:

HSBC has warned that the outcome of its review of whether to remain based in London could be delayed beyond the end of this year, as it reported a rise in profits because of a fall in fines and legal costs.

Britain’s biggest bank caused a political storm in April when it announced it was considering whether to keep its headquarters in London, where it moved to in 1992 from Hong Kong to facilitate the takeover of Midland bank. Stuart Gulliver, the bank’s chief executive, later said the decision would be known by the end of 2015.

But, as the bank announced its results for the first nine months of the year, it said a decision might take longer....

HSBC decision on whether to stay in London could be delayed https://t.co/6ie3LKawES

— Jill Treanor (@jilltreanor) November 2, 2015

Mike Rigby, head of manufacturing at Barclays, is also a little sceptical about the PMI report.

He’s surprised that UK factories would have enjoyed such a strong October, given the ongoing weaknesses in Europe and the strength of the pound:

“Though much-needed, after three consecutive quarters of falling output, many will find October’s rebound in manufacturing numbers a tad surprising and will eagerly await November’s figures to see how sustainable the bounce back is.

Buoyant as orders from some exports markets may have been, the appreciation of sterling and the impact this has on competitiveness within our main export market, the Eurozone, continues to test UK manufacturers.”

This chart from Berenberg underlines how the UK factory PMI has bucked the recent downward trent...

Berenberg Bank’s Kallum Pickering also urges caution over the UK factory PMI report.

He points out that it shows one of the best monthly improvements in recent history, surprising economists who expected a slight deterioration:

Monthly data can be volatile, and often survey data is at best loosely related to the underlying trend in the official data. Therefore, it is important to see this trend both established over an extended period and reflected in the underlying data before claiming victory.

Still, the 3.7 point monthly gain to 55.5 is one of the steepest in the surveys history and was significantly above both the market consensus of a slight decline and our above own optimistic view of unchanged on the month.

Samuel Tombs, chief UK economist at consultancy firm Pantheon Macroeconomics, isn’t convinced by this UK PMI report.

He calls it a ‘striking outlier’, given that the UK manufacturing sector is currently in recession (according to the official GDP figures).

Tombs writes:

In one line: Take with a pinch of salt.

He adds that:

We doubt that exports will see sustained growth, given that they are uncompetitive at the current exchange rate. And domestic demand growth is likely to weaken too as consumers’ real income growth slows as inflation rebounds and job gains slow. So to us, this doesn’t look like the start of a manufacturing resurgence.

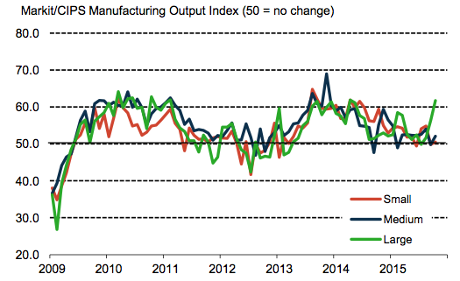

Large UK factories led the revival last month, rather than smaller manufacturers, according to Markit:

David Noble, CEO at the Chartered Institute of Procurement & Supply, explains why:

“The sector rode on the crest of an exports market wave taking full advantage of the opportunity to create a surge of output growth and new orders.

“Though domestically orders were still strong, it was export orders primarily from the Middle East, East Asia and the USA, that supported this expansion of work. Larger corporates were the overall winners more able to meet the demands of the overseas markets and employing more staff, as SMEs lagged behind with little change.

It’s all quite surprising, given the recent warning signs from across the global economy...

James Knightley of ING says the revival of UK manufacturing last month is “very impressive given the strength of sterling and external growth worries”.

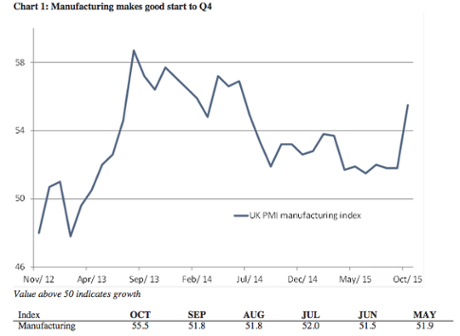

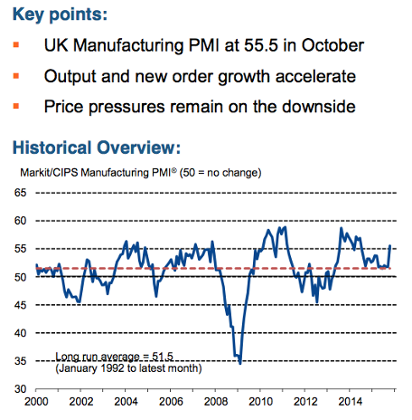

Markit: UK manufacturing growth regains momentum in October

The British economy may grow by as much as 1% in this quarter, if the strong factory growth recorded last month persists.

That would be twice as fast as in the third quarter of 2015.

Output and new orders both accelerated last month, pushing Markit’s UK manufacturing PMI up to 55.5, from 51.8.

That’s a significant acceleration in growth. It was mainly due to strong domestic demand, although overseas sales also picked up.

Markit’s Rob Dobson says:

Based on historical comparisons, the survey is consistent with a quarterly rate of growth of around 1%, a vast improvement on what we have seen in recent months. The big question now is whether this bounceback is a one-off or the start of a sustained re-emergence from recession.

“The ongoing strength of the domestic market and a welcome improvement in new export orders led to a broad-based upturn in production of consumer, intermediate and investment goods.

And here’s the key points from the report (online here)

Updated

Delighted to report that Guardian Towers has not burned down, and we’re allowed inside again.

Updated

The pound has jumped against the US dollar on the back of that strong manufacturing report.

BREAKING UK Manufacturing PMI October 55.5 Vs est 51.3 #GBPUSD pic.twitter.com/zeGKPa6TRJ

— Jonathan Ferro (@FerroTV) November 2, 2015

An early interest rate rise just became a little more likely....

UK manufacturing growth hits 16-month high

Wow. UK factory output smashed forecasts last month, with much stronger growth than expected:

UK Manufacturing PMI (Oct) 55.5 versus 51.3 expected, previous 51.5 revised to 51.8 - Highest since June 2014

— Sigma Squawk (@SigmaSquawk) November 2, 2015

That’s pretty encouraging at first glance, suggesting fears over the British economy may be overdone....

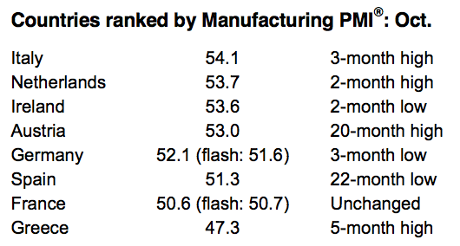

Howard Archer of IHS Global Insight has analysed today’s eurozone PMI reports (presumably from a nice warm office, the lucky blighter).

He says that they show modest improvement:

On the positive side, overall export growth was reported to have improved to a four-month high in October. While this includes intra-regional trade, it lifts hopes that the Eurozone is so far not being significantly hit by weakened growth in China and the Emerging Markets. Total orders growth improved in October to be at the best level since April 2014, which supports hopes that manufacturing activity cab see further modest improvement over the final two months of 2015.

Among the individual Eurozone countries, manufacturing expansion encouragingly clearly accelerated in Italy (up to 54.1 from 52.7) while there was also improvement in the Netherlands (up to 53.7 from 53.0) and Austria (up to 20-month high of 53.0 from 52.5).

Meanwhile, France managed to eke out a second successive month of modest expansion in October as its index was unchanged from September at 50.6.

However, German manufacturing growth slowed slightly in October (down to 52.1 from 52.3 in September), while Spanish expansion notably slowed to a 22-month low (down to 51.3 from 51.7). There was also slower manufacturing growth in Ireland (down to 52.6 from 53.8).

Finally, the contraction in Greek manufacturing activity moderated in October to the slowest rate since May (up to 47.3 from 43.3 in September and a record low of 30.2 in July).

Good news: I’ve set up a mobile hotspot outside our local pub.

Bad news, it’s closed....

Gosh it’s cold outside this morning.

Anyway, it takes more than a fire alarm to stop this blog - so here’s a chart showing how the Big Four eurozone countries performed last month:

Mamma mia. Italy manufacturing PMI the standout today. Real change to be in the lead. https://t.co/wjgRv2ctrQ pic.twitter.com/184O0iUAyd

— Ross Finley (@rossfinley) November 2, 2015

Fire alarm: great way to start a Monday morning. In the fog.

— Jonathan Haynes (@JonathanHaynes) November 2, 2015

Eurozone factory growth picks up

The upshot of today’s PMI reports is that growth in the eurozone manufacturing sector ticked higher in October.

Markit’s final Eurozone Manufacturing PMI has just been announced, at 52.3 in October, up from 52.0 in September.

The final PMI data for output, new orders and employment all came in stronger than the earlier flash estimates.

And with that, the fire alarms are going off here. Back soon (hopefully)....

Now for Germany.....and growth in its factory sector has hit a three-month low in October.

The German factory PMI has dipped to 52.1 last month, from 52.3 in September.

It’s too early to say if that means the economy is actually weakening, or merely entering a ‘soft patch’.

Oliver Kolodseike, economist at Markit, says there are some “warning signs” in the data set.

In particular, stocks of finished goods rose for the first time in a year, suggesting that a future rise in demand could be satisfied by using existing stock, rather than scaling up production levels.

“Moreover, growth was largely consumer-led, with the strong performance of the sector sitting in stark contrast with a contraction in the intermediate goods sector and only modest growth at investment goods firms.

France’s factory sector has posted modest growth again, lagging behind Spain and Italy:

France Manufacturing PMI (Oct) comes in at 50.6 exp: 50.7

— Michael Hewson (@mhewson_CMC) November 2, 2015

Italian factory PMI shows growth picked up

Good news from Italy!

The Italian manufacturing PMI rose to 54.1 in October, up from 52.7 in September. That means the sector expanded for the ninth month running, and at the fastest rate since July.

Italian firms told Markit that output and new orders both rose at accelerated rates last month, meaning they continued to hire more staff.

Phil Smith, Economist at Markit, adds:

Encouragingly, according to panel member reports sources of growth were both domestic and international, boding well for the sustainability of the recovery.

China’s lacklustre factory growth has helped to push Europe’s stock markets down in early trading.

Conner Campbell of SpreadEx explains:

Any signs of improvement from China are a bonus; however, the markets haven’t exploded into life in light of that better than expected Caixin figure largely because in its pre-50 form it still signals the 8 consecutive month of manufacturing contraction in the country.

Spanish factory growth hits 23-month low

Spain’s economic recovery appears to have come off the boil last month.

Growth in the Spanish manufacturing sector has hit its lowest rate since December 2013, according to Markit’s monthly healthcheck.

Firms reported that production growth slowed, due to weaker demand from clients. However, they also reported a pick-up in export orders, suggesting the sector is still quite robust.

Economic growth in Spain could be pegged back until the country had voted in December’s general election.

Andrew Harker, senior economist at Markit, explains:

“It’s looking like a low key end to the year for the Spanish manufacturing sector as growth rates for output, new orders and employment have all slowed to a crawl in recent months.

The forthcoming election is likely resulting in some caution among firms and clients alike as they wait to see the outcome of the December vote.

Ireland’s manufacturing PMI has fallen to 53.6 in October, down fractionally from 53.8 in September. That still shows robust growth, thanks to a rise in new business.

Philip O’Sullivan, Chief Economist at Investec Ireland, has the details:

“There was a welcome quickening (to a three month high) in the rate of expansion in New Orders in October.

A key factor behind this improvement was the ongoing substantial growth in New Export Orders, with a number of panellists reporting higher new business from clients in the US and UK.

Once Erdoğan has finished celebrating his election win, he can turn his attention to Turkey’s struggling economy.

And the latest PMI report, just released, shows that its factory sector shrank again last month, although at a slower pace.

The Turkish factory PMI rose to 49.5, up from 48.8 in September, showing a “marginal deterioration in Turkish manufacturing business conditions”. Output and new orders both fell, but exports and job levels rose, indicating a turnaround may be close.

Trevor Balchin, Senior Economist at Markit, said:

“Turkey’s manufacturing malaise continued in October, although the latest survey results suggest that the extent of the downturn remains modest.

Turkish shares and lira leap after election results

Investors have welcomed the news that Recep Tayyip Erdoğan secured a decisive win in Sunday’s general election.

Shares on the Turkish stock market are rallying in early trading, up over 5%, and the Turkish lira has strengthened against the US dollar:

#Turkey stocks jump >5% in tandem w/ Lira as AK Party win ends deadlock. https://t.co/c4uiykaQo3 pic.twitter.com/tZaxYE4aAe

— Holger Zschaepitz (@Schuldensuehner) November 2, 2015

Turkish lira rallies most since '08 after surprise AK Party win. $ down 4.6% vs Lira #TurkishElections pic.twitter.com/OgFpOLxXId

— Caroline Hyde (@CarolineHydeTV) November 2, 2015

Erdoğan’s campaign was based on the message that only his conservative, Islamic-leaning AKP could guarantee stability in Turkey. The country is facing the overspill of turmoil in the Middle East, the refugee crisis, and its own economic problems.

This unexpected victory gives Erdoğan’s renewed influence over the Turkish parliament, although he’s not got the ‘supermajority’ needed to reshape the political landscape into a US-style presidency.

Desicisive win for AKP in #Turkey but at least can’t change constitution. Worries about authoritarianism trumped by dislike of coalitions

— Robin Bew (@RobinBew) November 2, 2015

The result could also exacerbate divisions Turkey, as we reported overnight:

The prime minister and AKP leader Ahmet Davutoğlu tweeted simply “Elhamdulillah,” or “Thanks be to God,” before emerging from his family home in the central Anatolian city of Konya to tell crowds of cheering supporters that the win was “a victory for our democracy, and our people”.

Describing the results as a disaster, the main secularist CHP opposition saw its share of the vote slip to 25.4%, some 134 seats, while support for the nationalist MHP party fell sharply to 12% or about 40 seats, compared to 80 in June’s election.

Updated

Angus Nicholson of IG argues that today’s Caixin PMI manufacturing report is encouraging for China, even though it showed that activity contracted in October.

[It is] noticeably above expectations for 47.6 at 48.3, its highest since the stock market collapsed in June.

Caixin is usually more associated with smaller private sector firms, so to see such a big jump from the multi-year low the previous month is certainly a positive.

But Asia’s main stock markets have still fallen today:

China’s factory decline helps to explain why Beijing lowered interest rates last month.

So say analyst at ING, who believe further cuts will be needed:

“The data reinforce our view that the last PBOC interest rate cut (announced on Oct 23) was to preempt weak October activity data.

“In addition to setting global investor sentiment to risk-off, we think they will raise the consensus forecast for PBOC rate cuts.”

(via Reuters)

European markets are expected to fall this morning, as investors digest the news that China’s factory sector shrank again in October.

Our European opening calls: $FTSE 6328 down 33 $DAX 10776 down 74 $CAC 4857 down 41 $IBEX 10281 down 80 $MIB 22324 down 119

— IGSquawk (@IGSquawk) November 2, 2015

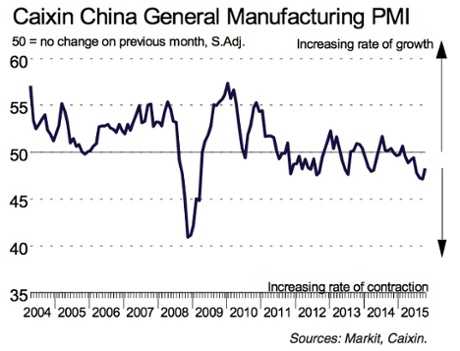

Chinese manufacturing activity shrinks for 8th month running

China has got PMI Day up and running, by reporting that activity across its factory sector shrank again last month.

But this year’s slump might soon be over.

The Caixin/Markit China Manufacturing Purchasing Managers’ Index(PMI) edged up to 48.3 in October from 47.2 in September.

This is the 8th month running that the PMI has been below 50 - which is the cut-off point between expansion and contraction.

And the report shows that conditions in the Chinese factory sector were tough. Total new business fell again, pushing down total output and employment levels.

But there is a glimmer of hope -- export orders rose last month.

Here’s the key points:

- Production falls at the weakest rate in four months

- Total new work contracts at slower pace amid improvement in new export order intakes

- Input costs and output prices continue to decline at marked rates

Dr. He Fan, chief economist at Caixin Insight Group, argues that the sector may be benefitting from recent stimulus measures from Beijing:

The slight upswing shows the manufacturing industry’s overall weakening has slowed down, indicating that previous stimulating measures have begun to take effect.

Weak aggregate demand remained the biggest obstacle to economic growth, and the risk of deflation resulting from the continued fall in the prices of bulk commodities needs attention.

This is the second survey of Chinese manufacturing. On Sunday, the official PMI came in at 49.8, matching September’s reading. Better than Caixin, but still a worry:

Updated

The Agenda: It's PMI Day

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

It’s a new month, which means a new set of data showing the health of world’s factory sectors.

A rash of “PMI” reports are due today from the eurozone, the UK and America, which will show whether the recent manufacturing slowdown continued in October.

These Purchasing Managers Indices show whether activity, output and experts speeded up or slowed down last month, and whether firms took on or laid off staff.

- Spain: 8.15am

- Italy: 8.45m

- France: 8.50am

- Germany: 8.55am

- The Eurozone: 9am

- UK: 9.30am GMT

-

US: 2.30pm GMT.

A poor set of figures may add weight to fears that the global economy is ending the year in poor shape.

CMC Markets Michael Hewson has rounded up the expectations:

Expectations are for Italy and France manufacturing to improve to 53 and 50.7 respectively, while German manufacturing PMI is set to slip back to 51.6.

Also coming up today.... investors will be chewing through financial results from banking giant HSBC and budget airline Ryanair.

We’ll also be watching the financial reaction to last night’s Turkish election (won by Recep Tayyip Erdoğan), and the stress tests which show Greek banks must raise €14.4bn in new capital by Friday.

Updated