- “In most European countries, standards of living almost surely will never reach the level they would have achieved had it not been for the euro…” - Jos. Stiglitz [emphasis in the original]

The economist Joseph Stiglitz (and we are evidently required by international law to mention that he is a “Nobel-prize-winning economist”) has taken a strong stand against the Euro and the Eurozone, which he regards as a dangerous failure, or, worse, practically a crime against the people. Indeed, here he is, several years before Brexit, a prominent left-of-center economist explicitly advocating a break-up of the currency union (unless the EU should accede to his own wide-ranging and politically improbable prescriptions).

In his influential 2016 book, The Euro And Its Threat to the Future of Europe, which is available in French, German, Italian, Portuguese, Romanian, Spanish, Catalan, and Korean (at least), Stiglitz reviewed the sorry state of the Europe’s recent economic performance, and argued that “while there are many factors contributing to Europe’s travails, there is one underlying mistake: the creation of the single currency, the euro.” The book attracted a lot of attention as a battle-cry against the establishmentarian elite in the EU (along with IMF and Stiglitz’ academic adversaries) who have – in Stiglitz’ view – brought a structural catastrophe down upon the heads of European citizens, at least those in the “poor South” (Italy, Spain, Greece, Portugal, and maybe Ireland, too), and stagnation to almost everyone. The misbegotten Euro has (he says) directly fueled the rise of right-wing reactions across the continent.

This is a striking thesis. Stiglitz is a warhorse for the establishment Left in the economic profession (former chief economist of the World Bank and Chairman of Bill Clinton’s Council of Economic Advisors), which makes his position both surprising (for an unexpected negativity towards the European project – he even offers advice on “How to leave the Euro and Prosper” – yes, Brexit avant la lettre) — and unsurprising (for its animus towards the bankers, and the private sector generally). He is in fact entirely prepared to view the Euro in political-conspiratorial terms:

- “There might have been a political agenda — bringing down left-wing governments, teaching electorates the consequences of electing such governments, and making it more likely that a conservative economic and social agenda would prevail within Europe.” [p.21]

His diagnosis is superficial, accurate, as far as it goes, and conventional. The main problem as he sees it is the common currency concept itself: the creation of the euro-zone removed the option of currency devaluation from the policy toolkit of its members states. And so, Greece, or Italy, in the “old days” might have been able to offset trade imbalances and other economic ills (e.g., structurally noncompetitive labor laws) by allowing the currency to devalue, improving global competitiveness, stimulating exports and restraining imports – this is how countries like Japan and lately China have climbed the economic ladder. But Europe’s “losers” can no longer avail themselves of this sort of “automatic stabilizer.” With monetary policy and currency values set at the “federal” level, there is not much that Greece (e.g.) can do — except to “devalue” its real economic output by reducing wages and national income – in short, by going backwards economically, becoming poorer. The result, directly attributable to the common currency (as per Stiglitz), has been a savage and persistent downturn in the South, and sluggishness through the Eurozone – which he documents in some detail.

The loss of the exchange rate mechanism is undoubtedly part of the problem. The diagnosis is superficial, however, in the sense that it doesn’t get to the question of how Greek or Italian non-competitiveness arises in the first place. It just points to the removal of one of the traditional policy instruments for dealing with it.

Beyond the currency question, Stiglitz blames the policy blunders (as he sees the matter) by what he calls the “Troika” – which refers to the IMF (Washington DC), the European Commission (Brussels), and the European Central Bank

Again, this is true enough. German opposition to expanded European federalism is undoubtedly a big part of the impasse. But we knew that too. And it can’t be said that Stiglitz offers any insight into the German position. For him, they are just blockheads... (or, excuse me, poor economists).

Indeed, if there is a root cause in Stiglitz’s model of European dysfunction, it is “neoliberalism” or “market fundamentalism” – which is to say, the theories of economists he disagrees with, who have somehow gained control of the levers of public policy and screwed things up with ideas and policies which are bad, wrong, and plain stupid.

He would also indict the Europeans for “insufficient solidarity” – but this notion is undeveloped (What is “solidarity” exactly, in this context?) It commands much less attention in his book than the rants against the Germans, the Friedman-ite economists, and the bankers.

What About the American Model? (Among Others)

What is missing from this analysis is a meaningful explanation of just why this currency union doesn’t work. The obvious counter-example is the United States, where the common currency works just fine, where a transfer union functions easily, automatically, without anyone even thinking about it, and where despite the long history of tension between federal and state policy –– the “states rights” argument in all its manifestations, from the Tenth Amendment to the Constitution down to the current disputes over voting procedures in Atlanta (e.g.) – despite that history, the U.S. has put in place almost all of the positive proposals that Stiglitz would like to see the Europeans adopt, including

- a “banking union” – by which Stiglitz means (1) a common regulatory framework for the banking industry, (2) federal deposit insurance, and (3) federal-level procedures for dealing with banks in trouble, which he calls “common resolution”

- federal-level welfare or transfer payment programs (like Social Security, or Food Stamps)

- a Central Bank endowed with a dual mandate, to balance policies aimed at controlled inflation with those focused on promoting full employment

- stronger corporate governance

- more liberal immigration policies, enforced at the federal level…

And so on. The point is — in a federal system, the dollar works. But the question of how the U.S. ever managed to “cross over” – psychologically and culturally – to a successful federal modus operandi and common currency is not developed much in Stiglitz’ analysis. He admits that the Eurozone “falls far short of the degree of economic and political integration that defines the United States” and admires American inter-regional solidarity (“there is no distinction between a native Californian and an ‘immigrant’ from South Dakota”) – but as to why it is so, and what to do in Europe, his answers are the conventional left-anodyne recommendations – higher taxes, “better” regulation, and more government. Smarter economists. (Like him.)

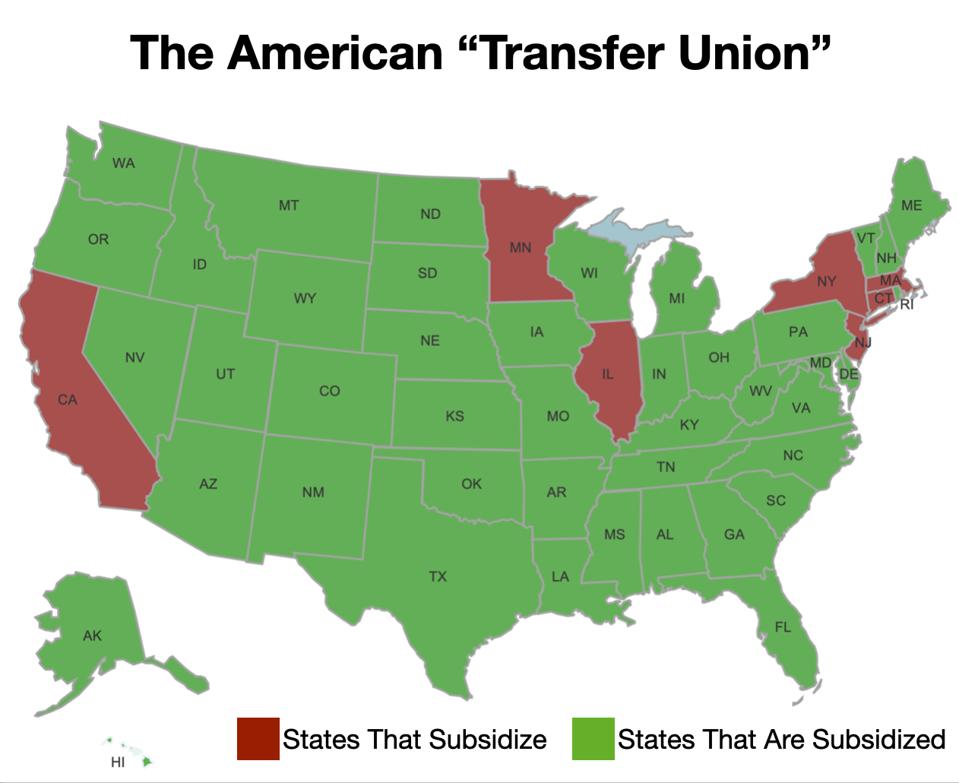

The American transfer union is remarkable. Consider.

The red states are America’s Germanys — the subsidizers – and the Green states are the Italians and the Greeks, the recipients of the subsidies. The system just works, without any real political or cultural angst, almost (we might say) invisibly.

A similar map of the 23 provinces, 5 autonomous regions, and 4 municipalities in China would show similar transfers from richer to poorer regions.

There are in fact plenty of historical examples of successful currency unions. Germany itself is one. Prior to unification in 1871, there was no common currency.

- “The German Confederation, established in 1815, did not have a uniform currency. The Confederation was made up of approximately 35 principalities and cities, and they each issued their own coins.”

Italy, prior to its unification, also had several different currencies issued by different constant states (Naples, Florence, the Papal States…) – which were subsumed into the Lira in 1861.

Canada went through a process of “merging” French, British and American currencies to create the Canadian dollar.

In all these cases, currency unions had to accommodate important differences in language, culture, and local government. “Solidarity” was not an assumed precondition (and may still be deficient in some cases — e.g., Italy, Canada).

Stiglitz is Wrong

Stiglitz’ headline thesis is that the Euro — the common currency – is at fault for Europe’s troubles. But this cannot be the case. Well-functioning currency unions, in large states that encompass diverse local jurisdictions, do clearly exist and function well. In the EU, trade imbalances and the loss of adjustable exchange rates would be insignificant with a more complete federal system. (Who worries about the balance of trade between New York and Michigan?)

The difference between a successful currency union and an unsuccessful one is not about monetary mechanics. It lies in the fiscal arrangements — federal-level taxation, federal-level social welfare arrangements, federal-level banking regulation, etc – not in the monetary system per se.

Stiglitz’ argument that the economic ills of the Eurozone are due to the Euro is specious. The EU’s “failure” (so far) to achieve the goals of the European Project is due to a reluctance to embrace the “Hamiltonian moment” – a more robust federalism, and specifically a more comprehensive fiscal integration.