/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)

For years, Intel (INTC) had been the undisputed leader in the semiconductor industry, powering the vast majority of the world’s computers and servers. However, that dominance has slipped over the last decade as Advanced Micro Devices (AMD) has steadily increased its share of CPUs and Nvidia (NVDA) has emerged as the powerhouse of artificial intelligence (AI) and accelerated computing.

With both rivals firing on all cylinders, the question is whether Intel can truly stage a comeback. With billions of dollars in new funding from both the U.S. government and private partners, new leadership under CEO Lip-Bu Tan, and an ambitious $100 billion manufacturing expansion plan, Intel may finally be putting the pieces together for a comeback.

A Massive Vote of Confidence With New Investments

Two major investment announcements this month could be a turning point for the company. On Aug. 18, Intel announced that SoftBank Group (SFTBY) would invest $2 billion in its common stock.

More recently, and in a far more significant development, the U.S. government announced an $8.9 billion equity stake in Intel, equivalent to nearly 10% of the company. The investment, made possible by CHIPS Act grants and the Secure Enclave program, provides Intel with permanent capital to accelerate its $100 billion-plus U.S. expansion plan. With warrants to increase its stake, the U.S. government is making a generational bet on Intel’s ability to reestablish American semiconductor leadership.

Intel stock is up 23.92% year-to-date, compared to the S&P 500 Index ($SPX) gain of 10.2%.

A Mixed Quarter Amid Headwinds and Restructurings

Intel’s turnaround plan is ambitious. The company is investing more than $100 billion to expand chip manufacturing in the U.S., with flagship facilities in Arizona and Ohio. Its Arizona facility is set to start high-volume advanced-node production later this year. Intel has spent $108 billion on capital expenditures and $79 billion on R&D over the last five years, with the majority of that investment going toward process technology and U.S. manufacturing. The goal is to regain or even surpass the positions of Taiwan Semiconductor Manufacturing Company (TSMC) (TSM) and Samsung in advanced nodes.

In the second quarter, revenue reached $12.9 billion, above the high end of prior guidance, but flat year-over-year. Growth was driven by strength in both client computing and servers, aided by Windows 10 end-of-service refresh cycles and an aging installed base of PCs from the COVID period.

However, profitability remains under pressure. The second-quarter gross margin stood at 29.7%, well below long-term targets, owing primarily to impairment and depreciation charges. Management stated that, excluding one-time items, adjusted gross margin would have been 37.5%, with earnings per share of $0.10 rather than the reported negative $0.10.

While Intel ended the quarter with $21.2 billion in cash and short-term investments, free cash flow came in negative at $1.1 billion due to gross capital expenditures of $4.5 billion. Intel is focusing heavily on capital discipline. The company has not delivered a full year of positive free cash flow since 2021, which Tan called “completely unacceptable.”

One of Intel’s biggest challenges was overinvesting in capacity and side projects, which resulted in idle fabs and a scattered footprint. CEO Lip-Bu Tan is refocusing by monetizing a portion of Mobileye (MBLY) and selling Altera to Silver Lake, freeing up funds for CPUs, foundry, and AI. With AMD and Nvidia remaining lean and focused, Intel must now streamline, bet wisely, and execute flawlessly to reclaim credibility.

Intel’s foundry ambitions are still central to its turnaround story. In Q2, Intel Foundry generated $4.4 billion in revenue, a 5% drop sequentially but ahead of expectations. Importantly, 18A, the company’s next-generation process node, began production in Arizona. Panther Lake, the company’s upcoming client CPU, is set to be the first major product on 18A, with a launch later this year. The company also provided an early version of its 14A process design kit (PDK) to lead customers, indicating progress on the next node. If Intel is successful in executing this ramp, it will not only restore credibility but also attract external foundry customers.

AMD has been Intel’s most direct competitor in CPUs. In response, Intel’s AI PCs are emerging as a bright spot, accounting for an increasing share of the client mix. On the server side, hyperscalers and enterprises continue to refresh their CPU fleets, with the new Xeon 6 family gaining popularity. While Intel and AMD compete in CPUs, Nvidia presents a completely different challenge. Nvidia’s dominant position in AI training workloads, combined with its CUDA software ecosystem, gives it a near-monopoly on AI infrastructure spending. Intel understands that it cannot dethrone Nvidia, so it is instead focusing on AI inference, edge AI, and software platforms.

While management expressed cautious optimism in Q2, the path forward will be marked by painful restructuring, capital discipline, and a shift of resources back to its core business. Intel expects revenue in the third quarter to be between $12.6 billion and $13.6 billion, compared to $13.3 billion in the prior-year quarter. In the third quarter, the company expects neither a loss nor a profit, which is consistent with analyst expectations. Analysts predict Intel will earn $0.12 per share this year, rising to $0.66 by 2026.

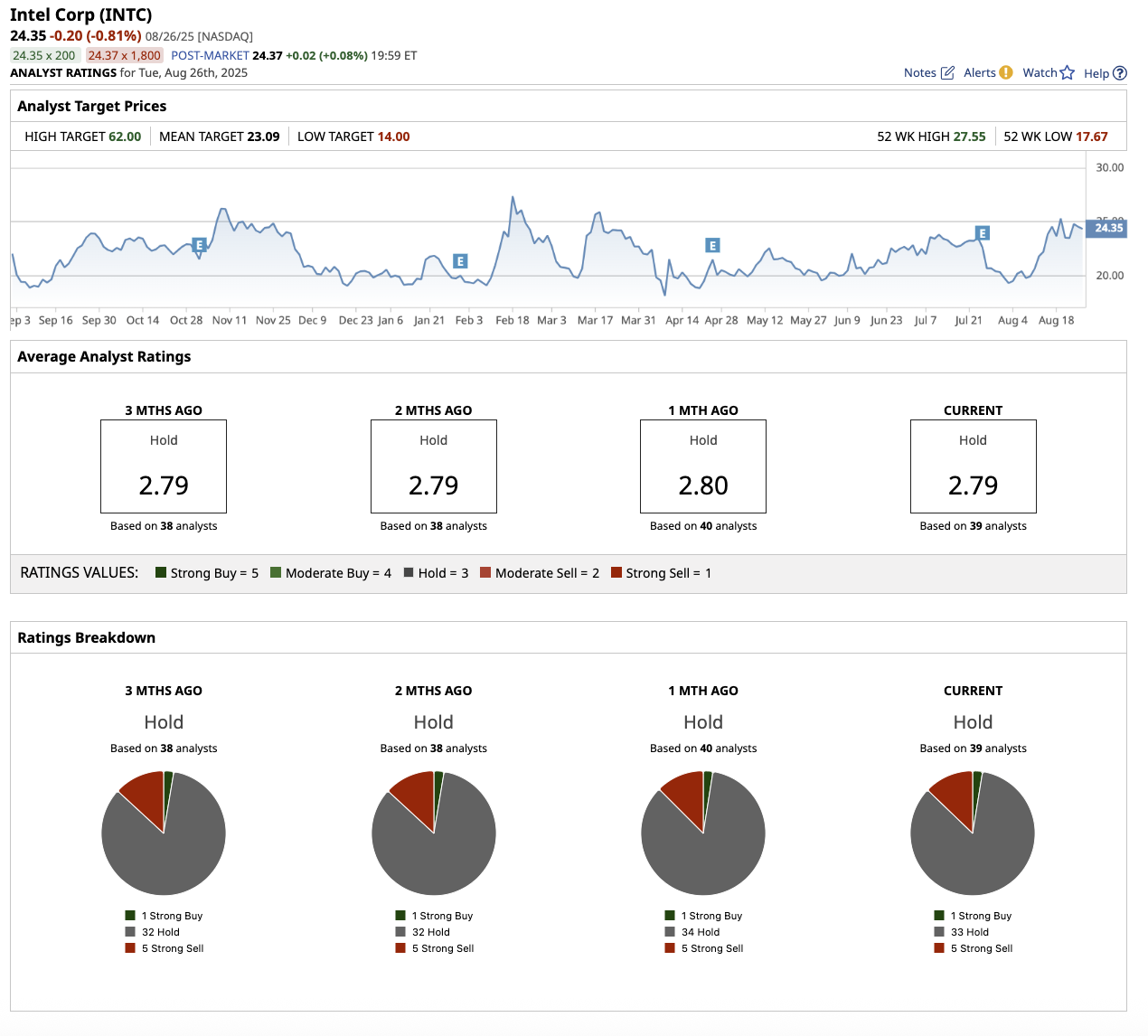

Is INTC Stock a Buy, Hold, or Sell on Wall Street?

Overall, Wall Street rates INTC stock a “Hold.” Of the 39 analysts covering the stock, one rates it a “Strong Buy,” 33 rate it a “Hold,” and five suggest a “Strong Sell.” The stock has surpassed it average target price of $23.09. However, the Street-high estimate of $62 suggests the stock has upside potential of 150% over the next 12 months.

The Bottom Line

Intel’s comeback is more than just a one-year story. Management acknowledges that the turnaround will take time and requires patience. For long-term investors, Intel represents a high-risk, high-reward turnaround story. It is not yet on the same growth trajectory as AMD or Nvidia. However, with significant capital support and new leadership, Intel has the potential to re-emerge as a key player in the next era of semiconductors.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.