Bank of America has a message for anyone who has grown skeptical of the AI boom: you are thinking too small.

In a report published Thursday, the bank’s research team made a typically sweeping claim for a Wall Street bank assessing the supposed artificial intelligence boom. It’s not like electricity or even the internet, the global economics team wrote. It is more powerful than both — and the productivity boom it will eventually deliver could be 10x larger than anything the economy is currently showing.

The problem is that the economy is currently showing 0.1%, “a small aggregate effect relative to all the excitement around AI,” the bank admitted. It’s a number so small that it barely registers against global growth of 3.5%.

Whether that argument holds is the most consequential open question in economics right now — and not everyone on Wall Street is buying it.

What 0.1% actually means

The gap between AI’s micro-level fireworks and its macro-level footprint is real, documented, and striking.

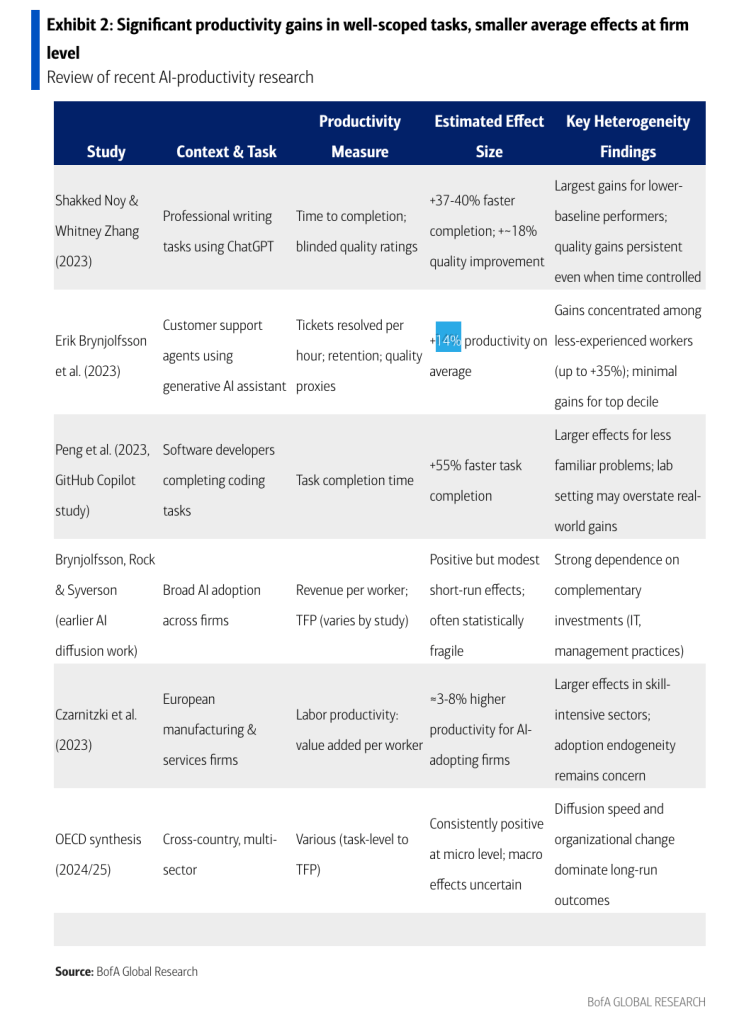

AI is already delivering task-level productivity gains that would have seemed implausible five years ago: software developers completing 55% more work with AI coding tools, customer support agents resolving 14% more tickets, professional writers finishing projects 37% to 40% faster.

But these aren’t showing up as a boost to GDP, BofA said, explaining that while AI can currently transform about 20% of all workplace tasks, only 23% of those are actually cost-effective to automate at today’s prices. Automated tasks save roughly 27% in labor costs, and labor is about half of all costs. Multiply it out and the theoretical ceiling is a 0.66% gain in labor productivity — before organizational friction, skills mismatches, slow diffusion, and regulatory drag compress it further toward the figure BofA has landed on: 0.1% per year.

The bank acknowledges the academic literature on AI’s aggregate impact is “inconclusive,” with multiple studies finding that even firm-level gains shrink or disappear when economists look at national accounts. While GDP statistics are poor at capturing quality improvements, this fits with the anecdotal sense that there’s a yawning divide between AI on paper and in reality. EY-Parthenon’s vice chair Mitch Berlin told Fortune earlier this month that he’s seeing a real “gap” in conversations with clients, even while saying that everyone he talks to is excited about what lies ahead.

BofA said AI is different when compared to previous innovations such as electricity or information and communication technology. The key difference, the bank argued, is that it can have an impact across a broader part of the economy than those previous advances, and “small improvements on this front can easily magnify the impact on aggregate productivity 10 times over the next decade.” BofA’s case rests heavily on the view that AI will follow the same J-curve — delayed impact followed by rapid acceleration.

But, still, a 10x increase? Really?

The 10x claim, unpacked

BofA’s bull case is not a forecast so much as an arithmetic exercise in what happens when conditions change — and the bank is explicit that the conditions driving that change are reasonable to expect.

The 10x figure comes from work by economist Philippe Aghion and co-authors published in 2024, which plugged more current AI capability estimates into a standard productivity model and found cumulative gains over the next decade that are 10 times larger than what today’s numbers suggest. The mechanism is straightforward: as AI models improve and inference costs fall — currently halving roughly every three months — the share of tasks that are both transformable and economically viable to automate expands rapidly. Each incremental expansion compounds non-linearly.

Doubling AI’s task reach from 20% to 40%, everything else equal, more than doubles aggregate productivity gains. If AI becomes cheap enough that all currently transformable tasks make economic sense to automate, gains multiply by more than seven. Add capital deepening — companies investing more as the return on capital rises — and the numbers get larger still.

But BofA makes a distinctive argument about innovation itself. Whereas electricity was powerful in automating physical processes, and the internet moved information faster, neither technology made inventing new things faster. AI can — by assisting research, accelerating hypothesis generation and augmenting the cognitive work that produces breakthroughs.

The bear case BofA doesn’t mention

Eight days before BofA’s report landed, Panmure Liberum strategist Joachim Klement published a detailed argument that the AI investment cycle is not a productivity story waiting to unfold, but rather a bubble that is still waiting to pop.

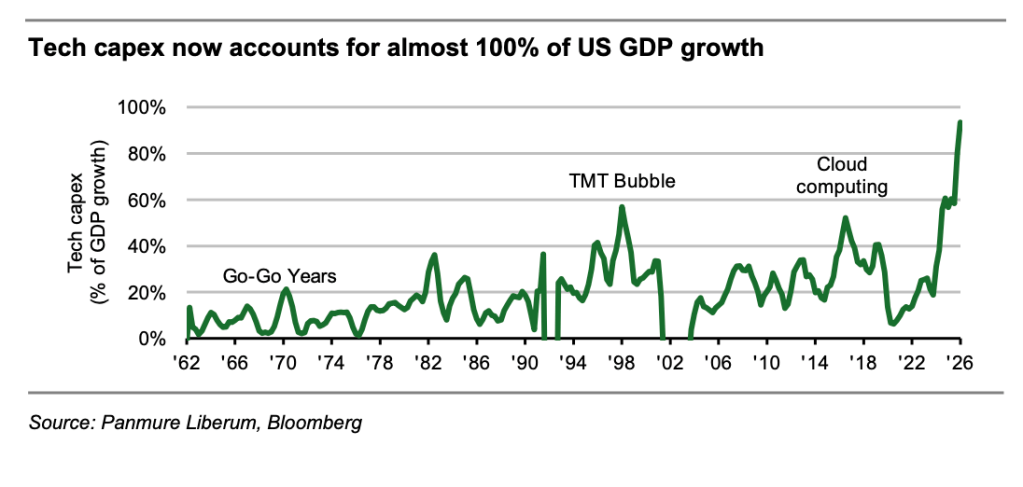

From a macro perspective, the AI boom is already 60% larger than the dot-com bubble at its peak, with tech investment accounting for 93% of all U.S. GDP growth, far beyond the 56% peak of the technology, media and telecom era. Hyperscalers — Amazon, Microsoft, Alphabet, Meta, Oracle — are projected to spend $658 billion on capital expenditures in 2026 alone, growing at a 20% annual clip through 2030.

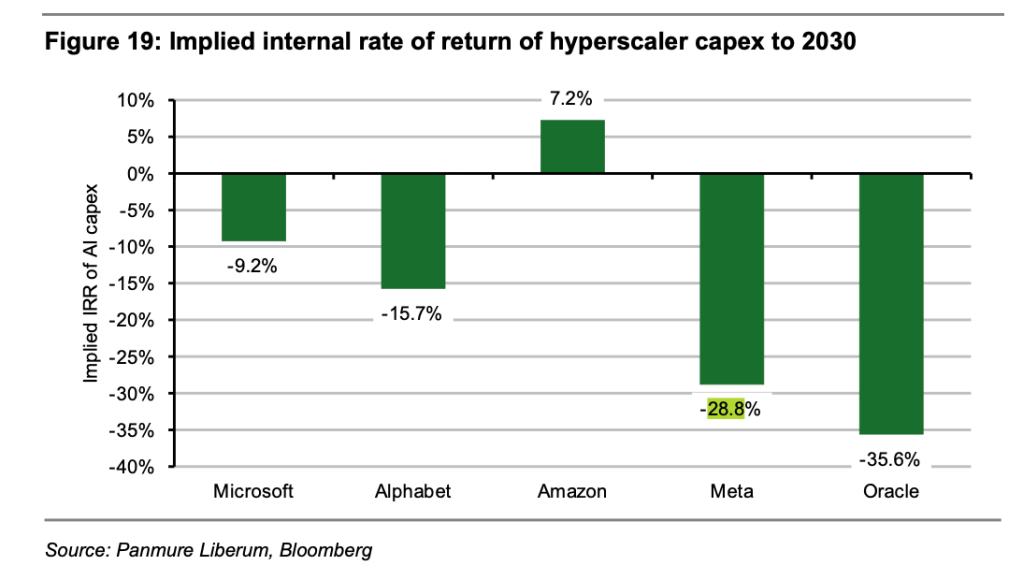

For those investments to generate even a 10% return, Klement calculated that hyperscalers need to find $2 trillion to $5 trillion in additional annual revenue — a quadrupling of their current base, with no meaningful increase in costs. Meta’s implied return on invested capital on its planned spending: negative 28.8%. Oracle’s: negative 35.6%. “There clearly are signs of irrational exuberance in stock markets today when it comes to the AI investment theme,” Klement wrote.

Klement also made a structural argument about the software layer that the productivity bulls tend to skip. Hallucinations in large language models, research from Tsinghua University shows, are not a fixable bug — they are neurologically inherent, traceable to neurons that emerge during pre-training and cannot be removed without breaking the model. This structurally disqualifies LLMs from the high-stakes deterministic use cases — accounting, legal filings, compliance — that currently justify much of the enterprise that premium investors are paying.

And threatening the entire data center rationale quietly from below: specialized small language models running locally on desktop hardware, at costs up to 1,000 times cheaper than cloud-based LLMs for routine commercial tasks. If the workloads that justify the hyperscaler capex boom can be handled locally and cheaply, the house of cards Klement described starts to look structurally unstable from the foundation.

Klement is not predicting imminent collapse — he estimates the bubble can sustain another one to two years on rate cuts. But in his mildest scenario, a modest correction in U.S. tech investment would send European and UK markets into bear territory. In a repeat of the dot-com crash, technology stocks would drop more than 70%.

The number in the middle

Tyler Cowen, one of the most widely read economists in the United States, addressed the gap between BofA’s bull case and Panmure’s bear case at the Sana AI Summit at the New York Public Library on Thursday — without quite framing it that way.

His forecast for AI’s contribution to U.S. growth: from 2% to 2.5%. Meaningful, he argued, but far short of what Silicon Valley is promising — and far short of BofA’s 1 percentage point addition to global growth. The constraint, in his telling, is institutional: roughly 40% to 50% of U.S. GDP sits in sectors — government, higher education, healthcare, nonprofits — that will be “very slow to adjust.” That drag doesn’t make AI less real. It makes the timeline longer and the path more uneven than the most bullish projections suggest.

Cowen’s 2.5% is still, in his view, transformative. Against the backdrop of $39 trillion in national debt, that delta is the difference between a debt spiral and a manageable fiscal path. “You feel we’re screwed,” he told the audience. “My kids are screwed, grandkids are screwed … But if our economy can grow at 2.5%, instead of 2%, that debt, rather than exploding and making us the next Greece, that debt actually converges to a manageable level.”

Cowen also asked the audience hypothetically, what else is there? “The way to get out of this hole, like if you work in AI, you are our savior.” Productivity growth means to no big tax increase and no big cut to Medicare, Medicaid and Social Security, he added, and there isn’t another good idea about how to plug the gap. “You are our plan A. There is no plan B.”

What the bulls and bears agree on

Strip away the valuation disagreement and BofA and Panmure Liberum share more common ground than their conclusions suggest. Both believe AI will materially change the economy. Both acknowledge the gap between task-level gains and aggregate productivity is real. Both identify organizational friction — not model capability — as the primary constraint on near-term macro impact.

The disagreement is not about whether the technology works. It is about whether the investment cycle has outrun the technology’s current economic contribution so dramatically that a correction is now the most likely near-term path — even if the long-term productivity boom eventually arrives on the other side of it.

That is a question BofA’s 10x argument, however coherent its mechanics, cannot answer. The gap between 0.1% and 1.0% has a plausible path. What it does not have yet is a timeline.