Markets end a turbulent week on positive note

Signs that central bankers might extend their support for the flagging global economy - possibly extending QE in the case of the US or the Bank of England not raising rates as quickly as expected - has given a boost to markets at the end of a volatile few days, writes Nick Fletcher.

Better than expected Michigan consumer figures also calmed some of the recent nerves, as did an easing of bond yields in the eurozone. But David Madden at IG warned:

The fear has evaporated out of the eurozone today as the bond markets have calmed down but I wouldn’t get too comfortable as next week is likely to be a rocky ride. The eurozone debt crisis has a history of rearing its ugly head, Ebola has yet to be contained, China’s GDP report will tell us the golden days of Chinese growth are over. Confidence in equity markets takes months to be gained but it is lost in hours.

For now though markets have accentuated the positive, unlike the past few days, and so the closing scores showed:

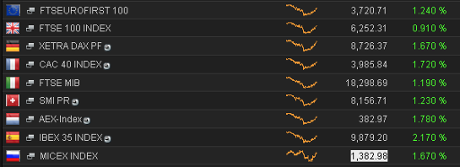

- The FTSE 100 finished up 114.38 points or 1.85% at 6310.29

- Germany’s Dax added 3.12% to 8850.27

- France’s Cac closed 2.92% better at 4033.18

- Italy’s FTSE MIB climbed 3.42% to 18,700.98

- Spain’s Ibex ended 2.97% higher at 9956.8

On Wall Street the Dow Jones Industrial Average is currently up 285 points or 1.77%.

And on that note, we’ll close up for the evening. Thanks for all your comments and don’t forget our pieces looking at the five years of the eurozone crisis. We’ll be back on Monday, so have a good weekend.

Some afternoon reading...

It’s five years (tomorrow), since the eurozone crisis began, when Greece revealed that its budget deficit was a staggering 12%.

Larry Elliott, our economics editor, has written about how the crisis remains unresolved:

Eurozone crisis, five years on: no happy ending in sight for Greek odyssey

And I’ve looked back over the hundreds of live blogs we’re written over half a decade...

Europe in turmoil: five years of economic crisis

And here’s Data Blog’s take:

Since taking office, Angela Merkel has met with 54 eurozone leaders, of which only four women http://t.co/zDRwU0ywAZ pic.twitter.com/SoLaXuB3OT

— Alberto Nardelli (@AlbertoNardelli) October 17, 2014

Good news for those rich Americans -- shares on Wall Street are rallying in early trading.

All major indices up over 1% in early going.

— Joseph Weisenthal (@TheStalwart) October 17, 2014

European markets are holding their gains too - the FTSE 100 is currently up 66 points, or around 1%. The German DAX is up 1.7%, and the CAC has gained 2%.

Updated

Yellen on inequality, the key charts:

The Fed has released 12 charts to accompany Janet Yellen’s speech on inequality -- they’re online here.

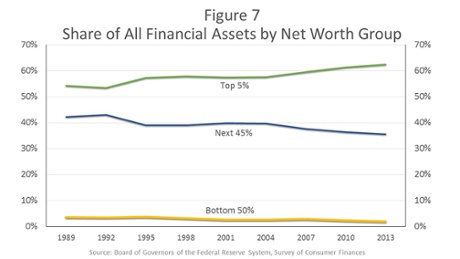

I’ve picked a few out, to show the scale of wealth disparity in America. As Yellen asks, is this really compatible with a country based on opportunity?

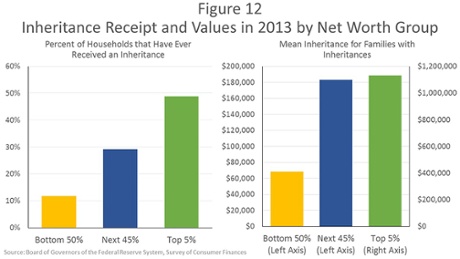

Yellen also touches on inheritance as a key factor in wealth inequality

The average age for receiving an inheritance is 40, when many parents are trying to save for and secure the opportunities of higher education for their children, move up to a larger home or one in a better neighborhood, launch a business, switch careers, or perhaps relocate to seek more opportunity.

...., I think the effects of inheritances for the sizable minority below the top that receive one are likely a significant source of economic opportunity.

(note those double axis on the right)

Yellen: How the American rich have got richer

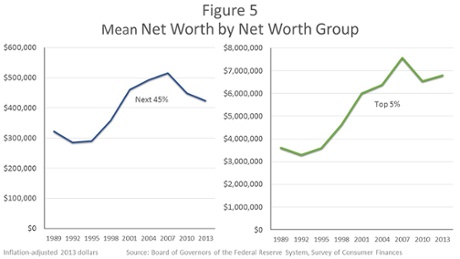

Fed chair Janet Yellen has also provided stark evidence of how the richest 5% in America have become richer in the last 25 years.

In her speech on inequality, she says:

The wealthiest 5 percent of American households held 54 percent of all wealth reported in the 1989 survey. Their share rose to 61 percent in 2010 and reached 63 percent in 2013. By contrast, the rest of those in the top half of the wealth distribution--families that in 2013 had a net worth between $81,000 and $1.9 million--held 43 percent of wealth in 1989 and only 36 percent in 2013.

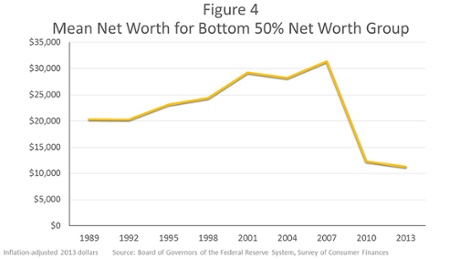

The lower half of households by wealth held just 3 percent of wealth in 1989 and only 1 percent in 2013. To put that in perspective, figure 4 shows that the average net worth of the lower half of the distribution, representing 62 million households, was $11,000 in 2013.

About one-fourth of these families reported zero wealth or negative net worth, and a significant fraction of those said they were “underwater” on their home mortgages, owing more than the value of the home.

Yellen: Is inequality consistent with American values?

Janet Yellen, chair of the US Federal Reserve, has made a dramatic intervention into the debate on inequality.

Yellen, arguably the most powerful woman in the world, has questioned whether America’s wealth inequality can actually be squared with its founding principles.

She told a conference on Economic Opportunity and Inequality that she is ‘greatly concerned’ by the wealth inequality in America, which are at their worst in a century.

The distribution of income and wealth in the United States has been widening more or less steadily for several decades, to a greater extent than in most advanced countries.

This trend paused during the Great Recession because of larger wealth losses for those at the top of the distribution and because increased safety-net spending helped offset some income losses for those below the top. But widening inequality resumed in the recovery, as the stock market rebounded, wage growth and the healing of the labor market have been slow, and the increase in home prices has not fully restored the housing wealth lost by the large majority of households for which it is their primary asset.

The extent of and continuing increase in inequality in the United States greatly concern me. The past several decades have seen the most sustained rise in inequality since the 19th century after more than 40 years of narrowing inequality following the Great Depression. By some estimates, income and wealth inequality are near their highest levels in the past hundred years, much higher than the average during that time span and probably higher than for much of American history before then.

It is no secret that the past few decades of widening inequality can be summed up as significant income and wealth gains for those at the very top and stagnant living standards for the majority. I think it is appropriate to ask whether this trend is compatible with values rooted in our nation’s history, among them the high value Americans have traditionally placed on equality of opportunity.

Here’s the speech:

Perspectives on Inequality and Opportunity from the Survey of Consumer Finances

More to follow...

Update: The European Central Bank has issued a statement on the leak of its minutes to the New York Times.

It insist that the governing council was united in its handling of the Cyprus crisis, even though these minutes expose the concerns expressed by some members.

It concludes:

The ECB was not the supervisor and fully relied on the assessment of the Central Bank of Cyprus. Therefore to draw conclusions about the ECB’s future banking supervision role on the basis of ELA to Cyprus is tendentious.

17 October 2014 - Statement on New York Times articles

But...but... the leak, dammit? How did that happen?!

ECB minutes leaked

Now this is interesting..... The New York Times appears to have been leaked the minutes of several European Central Bank governing council meetings.

These minutes are meant to be kept secret for decades. But someone’s passed them into the NYT. Full story.

They show divisions at the heart of the ECB over how to address Cyprus’s banking woes, in the months leading up to its bailout.

In particularly, Germany, France and the Netherlands all expressed concern over providing help to peripheral banks, such as the Cyprus Popular Bank.

The NYT says:

Mr. Weidmann, the tough-talking Bundesbank head, had long styled himself as the institution’s bailout scold. The minutes show him sharply opposing E.C.B.-backed rescues of the French-Belgian lender Dexia and smaller banks in Ireland, Greece and Spain.

In January 2013, just two months before the controversial Cyprus rescue package, Mr. Weidmann repeated his complaint that the E.C.B. was putting itself at risk in propping up Cyprus Popular Bank — which subsequently changed its name to Laiki Bank.

Moreover, Mr. Weidmann said that the value of the collateral posted at the central bank was inflated — which, if true, would allow it to secure more credit...

In the end, the ECB didn’t block the lifeline to Cyprus Popular Bank - and subsequently it collapsed amid the Cyprus bailout.

Interesting stuff, and a major breach of security at the ECB....

.@Landonthomasjr's piece in the @nytimes re 2012 ELA support for #Cyprus' Laiki is nothing less than a bombshell for @ecb's credibility.

— Yannis Koutsomitis (@YanniKouts) October 17, 2014

I guess the presumption has to be that the @ecb minutes came from the @bundesbank. So, what does @Mario_Draghi do when Buba goes rogue?

— Lorcan Roche Kelly (@LorcanRK) October 17, 2014

More here: Before a Bailout, Doubts Over Keeping a Cyprus Bank Afloat

Updated

European carmakers are rallying after data showed car sales in Europe climbed 6.1% to 1.3m vehicles last month.

Shares in Renault and Volkswagen are both up 3%, and Peugeot Citreon have surged 5.5%.

Europe’s car market bottomed out last year, ending a six-year slump, and has been growing for 13 months.

According to the Association of European Carmakers, Germany, the biggest market, saw sales rise 5.2% to 260,062. The UK, the number 2 market, was up 5.6% while France, the number 3, climbed 6.3%.

Sales in Spain, Portugal and Greece surged 30% or more as buyers snapped up cars from Volkswagen, Ford and Opel.

JP Morgan economist Allan Monks has pushed back his prediction for the first UK rate hike by one quarter to the second quarter of next year, following Andrew Haldane’s comments today.

Haldane’s views have been close to the centre ground on the committee so far. He is one of the MPC’s intellectual heavyweights, as well as Chief Economist, and hence we put significant weight on his comments.

Although the UK data have turned more mixed, the primary driver of Haldane’s shift rhetoric is global at heart. He summarizes by drawing attention to “the mark-down in global growth, heightened geo-political and financial risks and the weak pipeline of inflationary pressures from wages internally and commodity prices externally”. The speech contains a lengthy discussion of the recent weakness in wages.

But as we noted earlier this week, the pay data are showing tentative signs of improvement and are consistent with the BoE’s August Inflation Report projections. While the odds of a 1Q15 rate increase have not completely evaporated, Haldane’s comments suggest the data would need to turn stronger than we expect to deliver the first rate increase on this timescale.

But we are also mindful that the global element driving Haldane’s view could look rather different in a few months time. JPMorgan’s global forecast is relatively upbeat, with the US projected to grow at 3% and the euro area at 2% by the early part of next year. If delivered, this path would give the MPC confidence in the UK recovery, while clearer signs of wage inflation by that time (our current view) will also help to shift perceptions of medium term inflation risks.

While Jimmy Choo got its float away this morning, Virgin Money has just delayed its planned stock market listing beyond this month against a background of financial chaos.

This colour-coded chart from our data blog team shows which eurozone countries have benefitted most today’s revised growth data:

Impact of eurozone 2010 GDP revisions by country: pic.twitter.com/obLUQpKjGc

— Alberto Nardelli (@AlbertoNardelli) October 17, 2014

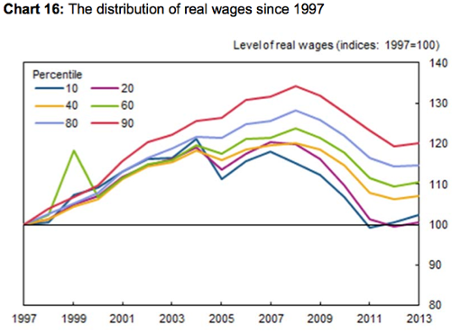

Here’s another important chart from Andy Haldane’s speech, showing how higher earners have disproportionately benefitted from pay rises since 1997.

Haldane says that this shows that the distribution of wages has not been static; it has widened over the past 20 years.

In the late 1990s, wages for the top 10% of earners were around 6.5 times higher than the bottom 10%. Today, the figure is closer to eight. Or, put differently, in the decade prior to the recession, real wages for the top decile rose on average by 3% per year, while for the bottom decile they rose by around half that.

Since the crisis, there has been an across-the-board squeeze on real wages.

Those distributional differences have, however, persisted and have if anything widened further. Despite having fallen by almost 10% since the crisis, real wages among the top 10% are still over 20% higher than in 1997. But wages for the bottom 20% have fallen by almost 20% since 2007 and are essentially back to where they were in 1997.

Weidmann: Germany doesn't need stimulus

Haldane isn’t the only central banker making headlines this morning.

Germany’s Jens Weidmann, head of the Bundesbank, has criticised those who are calling for Berlin to boost its spending to help its own economy, and the rest of the eurozone.

Speaking in Riga, Weidmann claimed:

“The boost to the peripheral countries from an increase in German public investment is ... likely to be negligible

“And with the economy operating at normal capacity utilisation, Germany is not in need of stimulus either – and this will remain the case with the revised forecasts that still foresee growth in line with potential.”

This kind of comments could backfire RT @lemasabachthani: *WEIDMANN SAYS GERMAN STIMULUS NOT NEEDED, COULD BACKFIRE

— Frederik Ducrozet (@fwred) October 17, 2014

Singapore’s sovereign wealth fund GIC has snapped up a 4.6% stake in Jimmy Choo, which debuted on the London stock market this morning. The shares are now flat at 140p.

Share price of Jimmy Choo barely above offer price at 140p. At least got it away. Anyone know demand to supply ratio?

— Louise Cooper (@Louiseaileen70) October 17, 2014

Eurostat: eurozone GDP 3.5% bigger than thought

Over to the eurozone....and stats body Eurostat has updated its GDP, to get into line with international standards.

The revisions account for research and development activity, and also for black market activities. And they have added an extra 3.5% to the size of the eurozone economy, and the wider EU.

That should drive down the region’s debt/GDP ratio, making Europe’s debts look more sustainable. But the broad picture isn’t changed; Europe still suffered a massive recession after Lehman Brothers collapsed, and has managed little growth since the debt crisis.

Some highlights: the Netherlands GDP is 7.6% bigger than thought. Cyprus is 9.5% larger (mainly due to ‘statistical improvements’).

R&D has added an extra 3.5% to Ireland’s GDP; those multinational tech firms making a contribution to the local economy (if not to the tax pot). But Latvia is 0.1% smaller, due to statistical improvements...

More here:

ESA 2010 shifts level of EU and euro area GDP upward, growth rates almost unaffected

Here’s more charts from this morning’s Andy Haldane speech on the ‘agony and ecstasy’ of the UK economy:

My three fave charts from Andy Haldane's speech pic.twitter.com/4bMNRDRF6S

— Ben Southwood (@bswud) October 17, 2014

Updated

Relief rally gathers pace

The relief rally continues in European stock markets. The FTSE 100 index is trading nearly 80 points higher at 6273.07, a 1.2% gain (with only five fallers on the blue-chip index in stark contrast to yesterday, when stocks were in freefall around the world). Germany’s Dax is 1.8% ahead and France’s CAC has added 1.9%.

FTSE100 within 10 points of yesterdays high 6282. Little bit of nerves up here maybe after the bounce back?

— David Jones (@JonesTheMarkets) October 17, 2014

Wall Street futures indicate the Dow Jones will open 174 points higher...

Updated

Haldane highlighted the long period of falling real wages (adjusted for inflation) in his speech this morning. He said:

This has been a jobs-rich, but pay-poor, recovery.

amazing chart in Haldane speech - UK has seen longest sustained fall in real wages in history http://t.co/yJvMP1QKRt pic.twitter.com/IJHsln3BvV

— Tony Tassell (@TonyTassell) October 17, 2014

Dear Andy Haldane if you wanted a gloomier view of real wage growth in the UK you could have used the Retail Price Index and not the CPI

— Shaun Richards (@notayesmansecon) October 17, 2014

Relief is rife in the European stock markets - the main indices are a sea of green:

If Haldane is right, the UK won’t see an interest rate rise before next May’s election.

That’s a relief for George Osborne and colleagues, suggests Paul Waugh of Politics Home:

Senior Tories feared interest rate rises cd cause real trouble if done early 2015. So Andy Haldane remarks to @itvnews signif

— Paul Waugh (@paulwaugh) October 17, 2014

Updated

On the markets, Jimmy Choo made its stock market debut this morning. While the luxury brand is famous for its perilously high heels, the shares got off to a rather flat start: up 0.5p to 140.5p. They were priced at the bottom end of the price range (140p), valuing the company, owned by JAB Luxury – the investment arm of Germany’s billionaire Reimann family – at £545.6m – rather than £700m as expected last month.

Updated

It’s early days, but there are signs that the US stock market might rally today.

Investors are taking comfort in Andy Haldane’s dovish comments that UK interest rates will stay lower for longer.

Last night’s hints from Federal Reserve policymaker Jimmy Bullard that America could maintain its QE stimulus programme for longer has also calmed nerves.

The Bullard and Haldane effect: S&P futures pointing to 15 point gain when Wall Street opens

— Chris Adams (@chrisadamsmkts) October 17, 2014

News Release - Twin Peaks - speech by Andy Haldane http://t.co/Luu7oCpTWn pic.twitter.com/1OGROcKsP2

— Bank of England (@bankofengland) October 17, 2014

Bank of England's chief economist Andy Haldane tells me it's "not a bad bet" to expect rates to rise in "the middle of next year"

— Richard Edgar (@ITVRichard) October 17, 2014

Haldane also warns that Britain is vulnerable to another explosion in the eurozone crisis, telling ITV News that:

“It’s a concern. It [the euro area] is our biggest trading partner by far. We know we’ve see recently that any event on the continent laps back to the UK very quickly through our trade links but also through our financial links and indeed increasingly just because of confidence.

If confidence is ebbing on the continent, it appears to leak across here pretty quickly.”

Haldane: I've changed my mind on interest rate rises

Andrew Haldane has also given an interview to ITV News, in which he reiterates that he is more reluctant to consider raising interest rates than three months ago.

The Bank of England’s chief economist says:

In the global economy, certainly, we’ve seen some of the energy of the recovery reduced, we’ve seen global growth prospects revised down a bit and here in the UK we’ve seen inflationary pressures from wages but also from oil prices, from commodity prices also heading south and those two things in combination means that I’m a bit less on the front foot than I was three months ago.”

So when might they rise?

“Who knows precisely when the lift-off date [the first interest rate hike] will come. If you believe the financial markets, they’re now betting somewhere in the middle of next year. Perhaps that’s not a bad bet.”

That interview will be on ITV News at 1.30pm, 6.30pm and Ten.

Updated

The pound has fallen by half a cent against the US dollar, underlining that expectations of an early rate rise have been stumped.

It’s trading at $1.6044 this morning.

Updated

I wish there was a new Andy Haldane speech in my inbox every morning.

— Duncan Weldon (@DuncanWeldon) October 17, 2014

The key monetary policy message from Andy Haldane this morning is that UK interest rates will probably stay at their current record lows for longer.

"Put in rather plainer English, I am gloomier” - BoE chief economist Andy Haldane

— Chris Adams (@chrisadamsmkts) October 17, 2014

Having weighed up his agony and ecstasy indexes, the Bank of England’s chief economist turns to cricket to explain his change of view:

In June, when evaluating the UK’s monetary stance, I used the metaphor of a batsmen in cricket deciding whether to play off the front foot (raise rates) or the back foot (hold rates). And I compared the averages of two English batsmen, one who played from the front foot (Ian Bell), the other from the back (Joe Root), to illustrate the dilemma.

At the time, Ian Bell averaged 45 to Joe Root’s 43. In other words, while it was a close run thing, the data narrowly favoured the front foot. Cricketing statistics are not the sole basis for my views on the appropriate stance for UK monetary policy. Nonetheless, on balance, I felt the same front-foot judgement was appropriate for UK interest rates at the time.

By contrast, if the effect on supply capacity was only temporary, lowering the measured output gap, that could imply the need for tighter policy.

Three months on, it is time to update the batting averages. Ian Bell’s batting average has remained at 45 – the front foot recovery has remained on track. But over the same period, Joe Root’s has risen to 51. Cricket statisticians and financial markets are agreed. While still a close run thing, the statistics now appear to favour the back foot.

So, Haldane won’t be voting to raise interest rates soon (the Bank’s monetary policy committee has been split 7-2 on his issue).

It seems unlikely that BoE's Andy Haldane is on the same wavelength as Martin "wages are about to take off" Weale: http://t.co/d6uerOnbq3

— Stephen King (@KingEconomist) October 17, 2014

Updated

Rolls-Royce has warned it won’t return to profit growth next year, blaming worsening economic conditions and tighter Russian trade sanctions. The shares tumbled more than 7%, or 71.5p, to 868p, making them the worst performer on the FTSE 100 in early trading. The British engineering firm said “a number of customers” had delayed or cancelled orders.

While the company cut its revenue forecast for this year, it maintained its forecast of “flat” 2014 profits – but no longer expects to return to growth in 2015. Its current “best estimate” is that underlying profit will be flat to 3% lower next year. Rolls-Royce is the world’s second-largest aircraft engine maker behind General Electric.

Updated

A calm start to Europe’s stock markets, as traders digest Andy Haldane’s speech (new readers start here).

The German DAX has jumped by 0.6%, and the French CAC is up 0.4%

The FTSE 100 is up just 3 points, dragged down by Rolls Royce which warned on revenues and profits this morning (more in a moment...)

Updated

Bottom line: Andy Haldane has joined the "lower for longer" camp at the @bankofengland. http://t.co/FeB3jev0IF pic.twitter.com/2Af8uvmQQV

— Peter Thal Larsen (@peter_tl) October 17, 2014

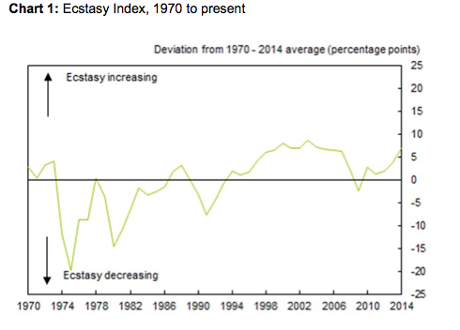

The ecstasy long-view from Andy Haldane pic.twitter.com/kFsoM3hGrN

— David Keohane (@DavidKeo) October 17, 2014

Haldane has also created an ‘ecstasy index, based on unemployment, inflation and GDP growth in the UK.

And in contrast to his agony index, this one looks quite good:

He says:

In only 42 of the past 144 years has the index been above current levels. So far, then, so good. The UK economy appears to be healthier than on average in the past, if perhaps not quite yet ecstatic. Certainly, it appears to be firmly on the front foot.

Thus Haldane’s point about Britain ‘writhing in agony and ecstasy’....

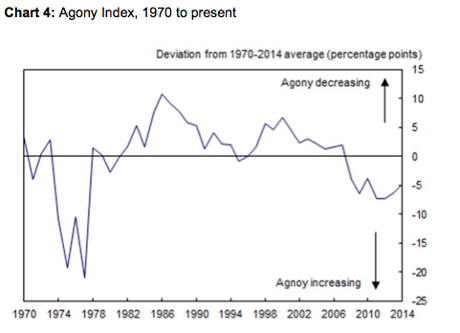

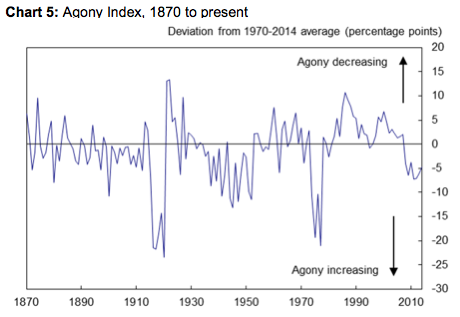

Haldane: Britain's agony index is currently at painfully low levels

Andy Haldane has also produced an “agony index” for the UK, a simple index of real wages, real interest rates and productivity growth.

And it shows that Britain’s economy is suffering serious pain:

Haldane tells his audience in Kenilworth, Warwickshire:

The agony index is currently at painfully low levels. It has been around 5 percentage points below its 1970-2014 average since 2008.

Such an extended period of agony is virtually unprecedented going back to the late 1800s, with the exception of the aftermath of the World Wars and the early 1970s.

See Andy Haldane's speech here

Andy Haldane speech is online here:

"The UK economy appears to be writhing in both agony and ecstasy." Very interesting speech by Andy Haldane. http://t.co/syxElzA08V

— Peter Thal Larsen (@peter_tl) October 17, 2014

Updated

Andy Haldane: I'm gloomier about the economy

Andy Haldane, the chief economist of the Bank of England, has warned that economic conditions have worsened.

In an important interventionat the Kenilworth Chamber of Trade right now, Haldane is explaining that he is gloomier about economic prospects.

He’s predicting that interest rates will remain at their record lows for longer.

Haldane points to slowing global growth, heightened geo-political and financial risks and the weak pipeline of inflationary pressures from wages in the UK and commodity prices worldwide.

This has led Haldane -- one of the brightest central bankers around -- to push back his own expectations of when UK interest rates will need to rise.

He says:

Rather peculiarly, the UK economy appears to be writhing in both agony and ecstasy. It is twin-peaked.

Haldane points out that the UK is in “fine fettle” by some measures; the strongest growth in the G7, and unemployment falling from 8.4% to 6%.

But there are also “reasons to be fearful”:

Growth in real wages has been negative for all bar three of the last 74 months’. ‘The level of productivity is no higher than it was six years ago’. And real interest rates are around zero. This combination of poor economic outcomes is ‘virtually unprecedented going back to the late 1800s, with the exception of the aftermath of the world wars and the early 1970s.’

And in conclusion, Haldane says:

On balance, my judgement on the macro-economy has shifted the same way. I have tended to view the economy through a bi-modal lens. And recent evidence, in the UK and globally, has shifted my probability distribution towards the lower tail. Put in rather plainer English, I am gloomier.

I’ll post some nice charts from his speech now....

Updated

The Agenda: markets tense after wild week

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and finance.

There’s no let- up in the panic swirling in the financial markets this morning, after the dramatic sell-offs that have racked the City in recent days.

Asian stock markets have endured another ropey day, with Japan’s Nikkei losing another 1.4%.

That’s despite St Louis Federal Reserve Bank President James Bullard suggesting yesterday that the Fed should consider delaying the end of its bond-purchase program.

European markets are expected to open more calmly, although in this environment who knows?

Modest update to European opening - FTSE -6, DAX +26, CSC -2

— David Buik (@truemagic68) October 17, 2014

The real story could come in the bond markets. Yesterday, Greece’s bonds came under heavy pressure, pushing the yield on its bonds up to 9%.

Chris Weston of IG comments:

The bond market looks like it has pushed Greece out (once again) of the funding markets.

There are plenty more central bankers speaking today, including Bundesbank chief Jens Weidmann, so it could be a lively day....