The defense and public safety technology sector has been strong this earnings season. Northrop Grumman (NOC) posted Q4 revenue of $11.7 billion, up nearly 10% and beating estimates by over $100 million, while RTX Corp's (RTX) sales surged 12% to $24.2 billion, supported by a record $268 billion backlog.

In the same vein, Motorola Solutions (MSI) saw its Q4 revenue climb 12.3% to $3.38 billion as AI-powered tools like its SVX body-worn assistant, which has already shipped over 15,000 units, lifted demand from law enforcement agencies. All of this is happening against the backdrop of the Trump administration's plan to boost defense spending to $1.5 trillion in fiscal 2027, a 66% increase that would send significant new funding into companies building advanced security and policing technology.

One company right in the middle of that shift toward modern defense hardware and AI-driven public safety tools just posted a quarter that stood out. Axon Enterprise (AXON), the company behind TASER devices, body cameras, and a growing cloud software platform for law enforcement, reported Q4 revenue of $796.7 million, a 38.5% jump that beat Wall Street’s forecast, and shares rocketed 23.8% in a single morning session.

With analysts still seeing roughly 30% upside from current levels and Axon targeting $6 billion in revenue by 2028, is this stock just getting started, or has the easy money already been made? Let’s find out.

The Numbers Powering AXON Stock’s Breakout

Axon Enterprise sits at the intersection of hardware and cloud software, selling conducted-energy weapons, body cameras, and a growing set of subscription tools that help public-safety agencies manage evidence and handle emergencies in real time.

AXON stock has risen a whopping 34% in the past five days. It is up about 8% over the past 12 months but down 23% in the past six months and almost flat year-to-date (YTD).

Axon currently trades at roughly 406x forward earnings, compared with about 21x forward earnings for its broader sector, showing just how much investors are paying for its growth story.

In Q4 2025, revenue jumped 39% to $797 million, powered by 40% growth in higher-margin Software and Services, which climbed to $343 million. Net income was a modest $3 million on a GAAP basis, but that supported $178 million in non‑GAAP net income and $206 million in adjusted EBITDA, highlighting the earning power behind the business once adjustments are factored in.

For 2025 overall, Axon delivered $2.8 billion in revenue, up 33%, crossed $1.3 billion in annual recurring revenue with 35% growth, and booked $7.4 billion of new business, lifting total future contracted bookings to $14.4 billion, a sign that demand is not only strong but also built into long-term contracts.

The Growth Engines Behind Axon’s Next Leg Higher

Cassava Technologies and Axon Networks have teamed up to build Africa’s first end-to-end Operator-as-a-Service platform (OaaS), combining AXON’s AI-ready, real-time, digital twin-enabled network technology with Cassava’s wide, high-speed fiber backbone to connect millions of people and businesses across the continent and speed up AI adoption and digital innovation. This OaaS setup is built for multi-tenant use and real-time insight, giving operators and service providers a practical way to deliver advanced connectivity and AI-driven services across Africa’s fast-growing markets.

On the public safety side, Axon is using targeted acquisitions to move deeper into the 911 and real-time operations stack. In late 2025, it closed the acquisition of Prepared, whose technology pulls together call audio, text, video, GPS, and real-time translation into a single view, already serving more than 1,000 agencies across 49 states and helping Axon push its goal of linking every part of public safety from call to closure.

In the first quarter of 2026, Axon completed a $625 million deal for Carbyne, a cloud-native emergency communications platform used by hundreds of agencies globally, whose call-handling and routing tools, combined with Prepared’s AI-driven situational insights, will feed into Axon 911, a next-generation, fully integrated emergency platform that brings real-time intelligence from the first call through field response, evidence management in Axon Evidence, and final resolution in the justice system.

What Wall Street Sees Ahead for Axon

For 2026, Axon is guiding for revenue growth of 27% to 30% year-over-year (YoY). For the current quarter (Q1 2026), analysts expect earnings of $0.13 per share versus a loss of $0.12 a year earlier, a 208.33% YoY swing back into positive territory. For Q2 2026, the Street is looking for $0.41 per share versus $0.85 last year, a 51.76% decline as it laps an unusually strong prior period. And for the full 2026 fiscal year, estimates call for $1.33 per share versus $1.25 in 2025, an increase of 6.4%.

On Jan. 6, Northcoast Research upgraded Axon to “Buy” from “Neutral” and set a $742 price target, pointing to a “more favorable view” of Axon’s growth path as recurring software and cloud revenue become a bigger part of the business. In a Feb. 24 post-earnings review, RBC Capital Markets kept an “Outperform” rating on the stock while trimming its target to $735, suggesting confidence in the long-term story even as near-term upside was adjusted after the rally.

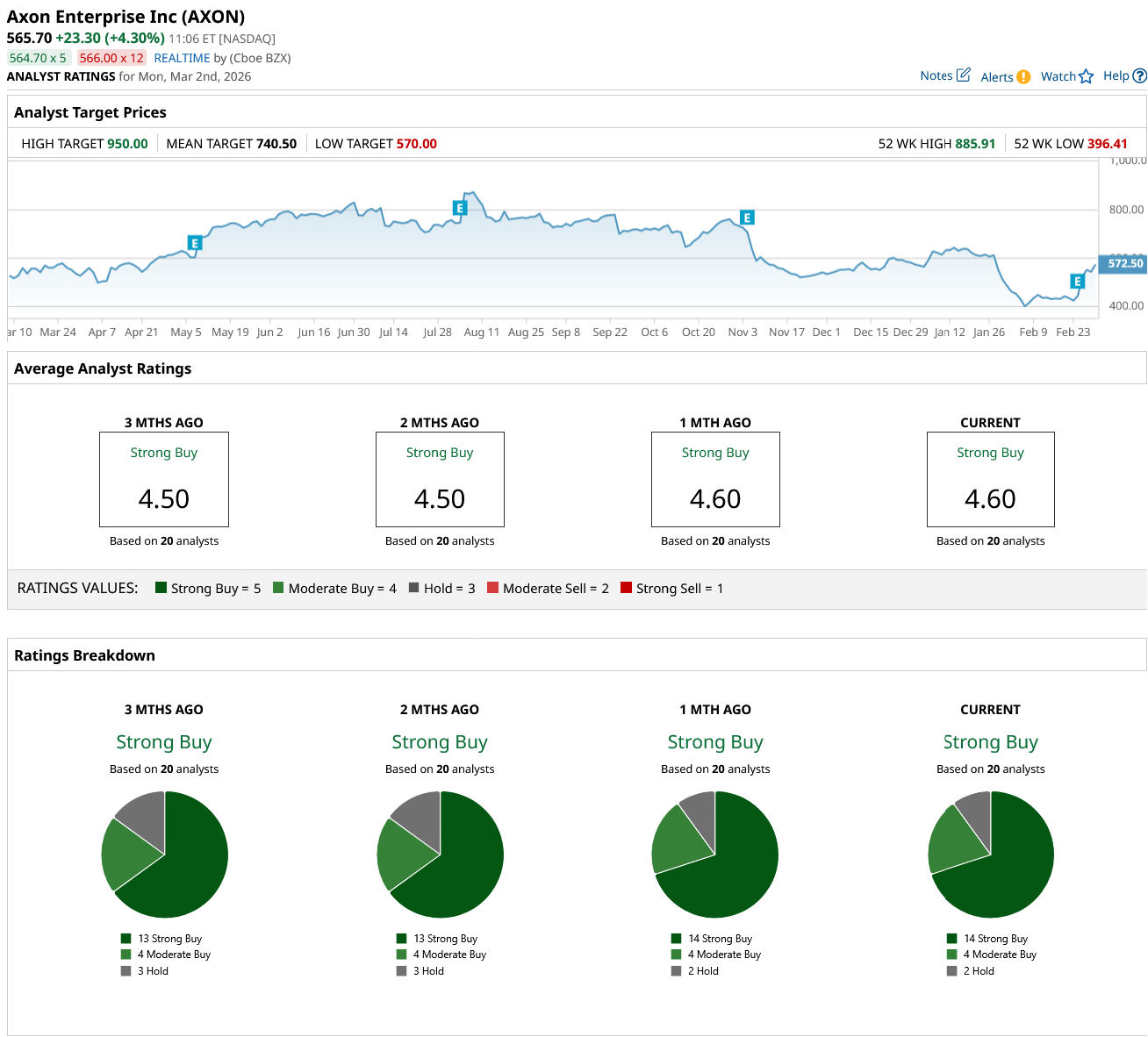

Stepping back, the broader analyst view is firmly positive. The 20 analysts surveyed currently rate Axon as a consensus “Strong Buy.” Their average 12-month price target is $740.50, and with the stock recently trading around $565 after its earnings-driven jump, that points to about 31% potential upside from here.

Conclusion

For now, Axon still looks more like a momentum story with fuel in the tank than a spent trade. The combination of high‑visibility recurring revenue, aggressive AI and 911 integrations, and a sector backdrop supported by rising defense and public safety spending gives the bulls plenty to lean on, even at a premium multiple. The flip side is that expectations are now sky‑high, and any stumble on growth, margins, or deal integration could hit the stock hard. On balance, though, as long as Axon keeps delivering on its pipeline and software mix, the path of least resistance still looks higher over the next year.