If you can afford the average cost of healthcare as you age, you'll be closer to solving one of the thorniest problems in retirement planning.

Unfortunately, the older you get, the crankier your body gets. That means more trips to the doctor, more prescriptions to fill and more money spent on care.

The average monthly cost of healthcare exceeds $1,300 by the time you're 60. It’s no surprise, then, that 80% of respondents to an RBC Wealth Management survey (PDF) said they’re concerned about funding the cost of healthcare in retirement.

Healthcare expenses in retirement rank second after housing costs, according to Western & Southern Financial Group. Given projected Medicare funding shortfalls by the next decade, planning for medical costs will be even more important.

What does healthcare cost at different ages — and stages of life? To find out, we dove into health expenditure data by age from the nonpartisan Center on Budget and Policy Priorities, the Peterson-KFF Health System Tracker and an analysis by ValuePenguin, a financial information website. We included an important 2026 cost update from the Employee Benefit Research Institute (EBRI).

Average cost of healthcare rises over time

In the big picture, here’s what the numbers tell us.

If you’re 55 and older, you can expect to pay anywhere from 50% more or even double what you would in your 20s, 30s or 40s, according to ValuePenguin data that looks at average monthly premiums for Silver tier coverage (e.g., moderate monthly premiums and moderate out-of-pocket expenses) purchased on the Affordable Care Act (ACA) marketplace.

If you’re 65 or older, expect to pay even more. A small segment of the population accounts for an oversized share of total health spending each year. That’s one key takeaway from the health spending analysis by Peterson-KFF.

People age 55 and older account for more than half (56%) of total health spending, despite making up just 31% of the U.S. population, according to KFF’s analysis of the Agency for Healthcare Research and Quality’s 2021 Medical Expenditures Panel Survey (MEPS).

“Health spending often increases with age, as we generally have more health conditions and need more care as we grow older,” the study co-authors noted.

A KFF report published in July 2025, titled "Americans' Challenges with Health Care Costs," revealed that just under half (44%) of U.S. adults find it difficult to afford healthcare costs.

Adults who’ve been diagnosed with chronic conditions, such as emphysema, diabetes, heart disease and high blood pressure, have much higher medical costs. Annual out-of-pocket costs, on average, go up for common medical conditions, such as diabetes (plus 27%), heart disease (plus 55%), and high blood pressure (plus 19%), according to new research from T. Rowe Price.

Those with mental health diagnoses such as anxiety and depression also pay more out-of-pocket for care.

Typically, younger people are healthier, have fewer chronic health conditions, and, as a result, pay less for health insurance. Here’s a cost breakdown by age that illustrates how medical bills can rise as people age.

Age |

2025 Cost |

2026 Cost |

|---|---|---|

20 |

$471 |

$571 |

25 |

$488 |

$591 |

30 |

$552 |

$668 |

35 |

$594 |

$719 |

40 |

$621 |

$752 |

45 |

$702 |

$850 |

50 |

$868 |

$1,052 |

55 |

$1,084 |

$1,313 |

60 |

$1,319 |

$1,598 |

64 and older |

$1,458 |

$1,766 |

*Cost for Affordable Care Act (ACA) Marketplace “benchmark” plans in Silver tier coverage, which comes with moderate monthly premiums and moderate out-of-pocket costs.

Source: ValuePenguin

Healthcare cost components

Age. “Age is one of several factors insurers use when calculating your health insurance premium,” said Dan Marticio, insurance expert at SmartFinancial, an online insurance marketplace.

For marketplace insurance plans, health insurers also consider these other factors when calculating premiums, according to SmartFinancial.

Location. Premium prices can vary by state and even by city, based on different costs for medical products, prescription drugs and care. See the table below for the average cost in your state. Keep in mind that the average cost of care in your state might be lower or higher for you, depending on your age or other factors.

Tobacco use. Smokers can pay up to 50% more than nonsmokers. You might be able to reduce your insurance rate a year after you quite smoking.

Number of insured. Adding dependents, such as children or a spouse, can increase the cost of health insurance.

Plan category. There are five coverage tiers for Marketplace healthcare plans, ranging from low-end Bronze to high-end Platinum. There’s also a Catastrophic plan.

The Bronze plans charge the lowest monthly premium but have the highest deductibles and out-of-pocket costs. In contrast, Platinum plans charge the highest premiums but cost you the least out of pocket.

State |

2025 |

2026 |

Percent Change |

National |

$621 |

$752 |

21% |

Alabama |

$564 |

$691 |

23% |

Alaska |

$1,088 |

$1,037 |

-5% |

Arizona |

$529 |

$685 |

29% |

Arkansas |

$494 |

$823 |

67% |

California |

$656 |

$728 |

11% |

Colorado |

$554 |

$703 |

27% |

Connecticut |

$708 |

$859 |

21% |

Delaware |

$578 |

$759 |

31% |

Florida |

$647 |

$859 |

33% |

Georgia |

$553 |

$729 |

32% |

Hawaii |

$523 |

$583 |

11% |

Idaho |

$490 |

$537 |

10% |

Illinois |

$684 |

$888 |

30% |

Indiana |

$432 |

$558 |

29% |

Iowa |

$507 |

$624 |

23% |

Kansas |

$642 |

$787 |

23% |

Kentucky |

$538 |

$662 |

23% |

Louisiana |

$654 |

$827 |

26% |

Maine |

$623 |

$771 |

24% |

Maryland |

$412 |

$480 |

16% |

Massachusetts |

$661 |

$725 |

10% |

Michigan |

$561 |

$719 |

28% |

Minnesota |

$451 |

$556 |

23% |

Mississippi |

$533 |

$756 |

42% |

Missouri |

$616 |

$742 |

20% |

Montana |

$636 |

$763 |

20% |

Nebraska |

$743 |

$960 |

29% |

Nevada |

$592 |

$792 |

34% |

New Hampshire |

$373 |

$491 |

32% |

New Jersey |

$583 |

$669 |

15% |

New Mexico |

$635 |

$800 |

26% |

New York |

$1,038 |

$1,090 |

5% |

North Carolina |

$664 |

$800 |

21% |

North Dakota |

$627 |

$700 |

12% |

Ohio |

$536 |

$635 |

18% |

Oklahoma |

$603 |

$739 |

23% |

Oregon |

$610 |

$643 |

5% |

Pennsylvania |

$610 |

$750 |

23% |

Rhode Island |

$477 |

$589 |

23% |

South Carolina |

$538 |

$657 |

22% |

South Dakota |

$690 |

$734 |

6% |

Tennessee |

$558 |

$775 |

39% |

Texas |

$610 |

$826 |

35% |

Utah |

$675 |

$821 |

22% |

Vermont |

$1,157 |

$1,224 |

6% |

Virginia |

$421 |

$514 |

22% |

Washington |

$543 |

$761 |

40% |

Washington, D.C. |

$573 |

$618 |

8% |

West Virginia |

$955 |

$1,093 |

14% |

Wisconsin |

$608 |

$722 |

19% |

Wyoming |

$895 |

$1,119 |

25% |

*Your cost might be lower or higher, depending on your age or other factors. Source: ValuePenguin

You may need to save much more for healthcare in retirement

Don't let those annual projections of healthcare costs by state lull you into complacency. While high, they don't capture all of the costs you'll need to consider when it comes time to retire. That's the conclusion of a 2026 report by EBRI, which found that some couples may need up to $469,000 in savings to cover their healthcare expenses in retirement. Couples on Medicare needing costly drugs fit this extreme example.

Here's a more common example.

"To have a 90 percent chance of meeting their healthcare spending needs in retirement," explains the EBRI report, "a man will need to have saved $212,000, and a woman will need to have saved $252,000. Couples enrolled in a Medigap plan with average premiums, meanwhile, will need to have saved $267,000 to have a 50 percent chance of covering their medical expenditures in retirement and $405,000 to have a 90 percent chance."

There's always a tradeoff between Medicare and its private counterpart, Medicare Advantage. But in general, the study found that those on a Medicare Advantage plan paid less. "Couples [on Medicare Advantage] will need to have saved $135,000 to have a 50 percent chance and $203,000 to have a 90 percent chance of covering their healthcare expenditures in retirement."

How to cope with the cost of healthcare in retirement

The high cost of healthcare in retirement can be daunting.

“Year after year, so many Americans underestimate how much they’ll need to save to cover healthcare costs in retirement,” said Shams Talib, head of Fidelity Workplace Consulting. The uncertainty surrounding one’s health trajectory, rising premiums and hard-to-predict out-of-pocket costs are the major reasons why many people stress about medical care and costs.

Get some perspective

T. Rowe Price research suggests it’s a mistake to view healthcare expenses in retirement as one giant lump sum amount. Despite these so-called big, scary numbers, nobody pays for healthcare all at once. It makes more sense to view medical costs as an ongoing budget.

“(Medical expenses) are spread out over many years,” Stuart Ritter, vice president, insights director at T. Rowe Price, wrote in a piece aimed at financial advisers titled, “What Your Clients Need to Know About Health Care Costs in Retirement."

“(Our research shows that) health care is far more financially manageable than it’s made out to be,” Ritter said. What makes planning a bit easier is that policy premiums, which account for 73% of healthcare expenses, are predictable fixed costs that retirees can plan for and pay from their monthly income, according to T. Rowe Price.

More unpredictable expenses, which are harder to plan for, such as out-of-pocket costs, account for just 27% of overall medical costs.

Severe healthcare 'shocks' are rare

What’s more, despite the pervasive fear of so-called healthcare “shocks,” or large, unexpected costs that arise due to an illness, causing financial ruin, only a small percentage of retirees experience such a destructive financial hit.

Only 10.9% of retirees experienced an increase in medical costs from $2,000 to $5,000 over a two-year period, according to T. Rowe Price research (PDF). Just 2% experienced an increase of $25,000 or more over a 24-month span.

How to plan for your future cost of healthcare

Like any financial goal, paying for healthcare costs requires planning. RBC Wealth Management (PDF) advises younger savers with time on their side to create a long-term investment plan to help cover the costs later in life.

Look to your employer

Workers should take advantage of workplace wellness programs, which can help reduce the cost of healthcare as they age. It's also prudent to choose the right healthcare plan that offers the best mix of coverage and cost.

ACA premiums have increased

For anyone not on Medicare, Medicare Advantage or employer-sponsored insurance, news that Congress axed the subsidy (enhanced premium tax credit) for ACA Marketplace plans came as a blow. In fact, about 14% of ACA enrollees failed to make their January 2026 payments after premiums increased, according to The Wall Street Journal. If you are struggling to afford an ACA plan, you'll need to understand the tradeoff of opting for a lower-tier plan.

Think Roth

Investing in a Roth 401(k) is another savings vehicle to consider, as you can withdraw your retirement savings tax-free, freeing up additional dollars to fund healthcare in retirement. Consider converting a traditional 401(k) into a Roth 401(k); you can convert all or part of your traditional 401(k), and you can stagger conversions to lower your taxable income in the years you convert.

Invest in HSAs for the long-term

Using tax-friendly health savings accounts (HSAs), which offer pre-tax contributions, tax-free investment growth, and tax-free withdrawals for qualified healthcare, can also be advantageous and reduce the onerous impact of high medical costs in your golden years. You can even use your HSA to pay for Medicare premiums.

Keep in mind that HSA contribution limits have risen steadily. In 2026, single plans can contribute up to $4,400, and family plans can contribute up to $8,750 in an HSA. Individuals 55 and older can contribute an additional $1,000. Before you go whole-hog on HSAs, look for hidden costs such as fees and yields.

Don't forget long-term care

Finally, think about how you might pay for long-term care. You might think you'll never need it, but government data show that about 70% of older adults require long-term care.

In addition to some of the strategies mentioned above, long-term care insurance and annuities might help fund long-term care needs. Both these options have downsides, so research them carefully.

Medicare premiums increased in 2026

Medicare Part B costs rose more than 9% in 2026. Moreover, if you're 63 or older, remember to account for the IRMAA two-year rule.

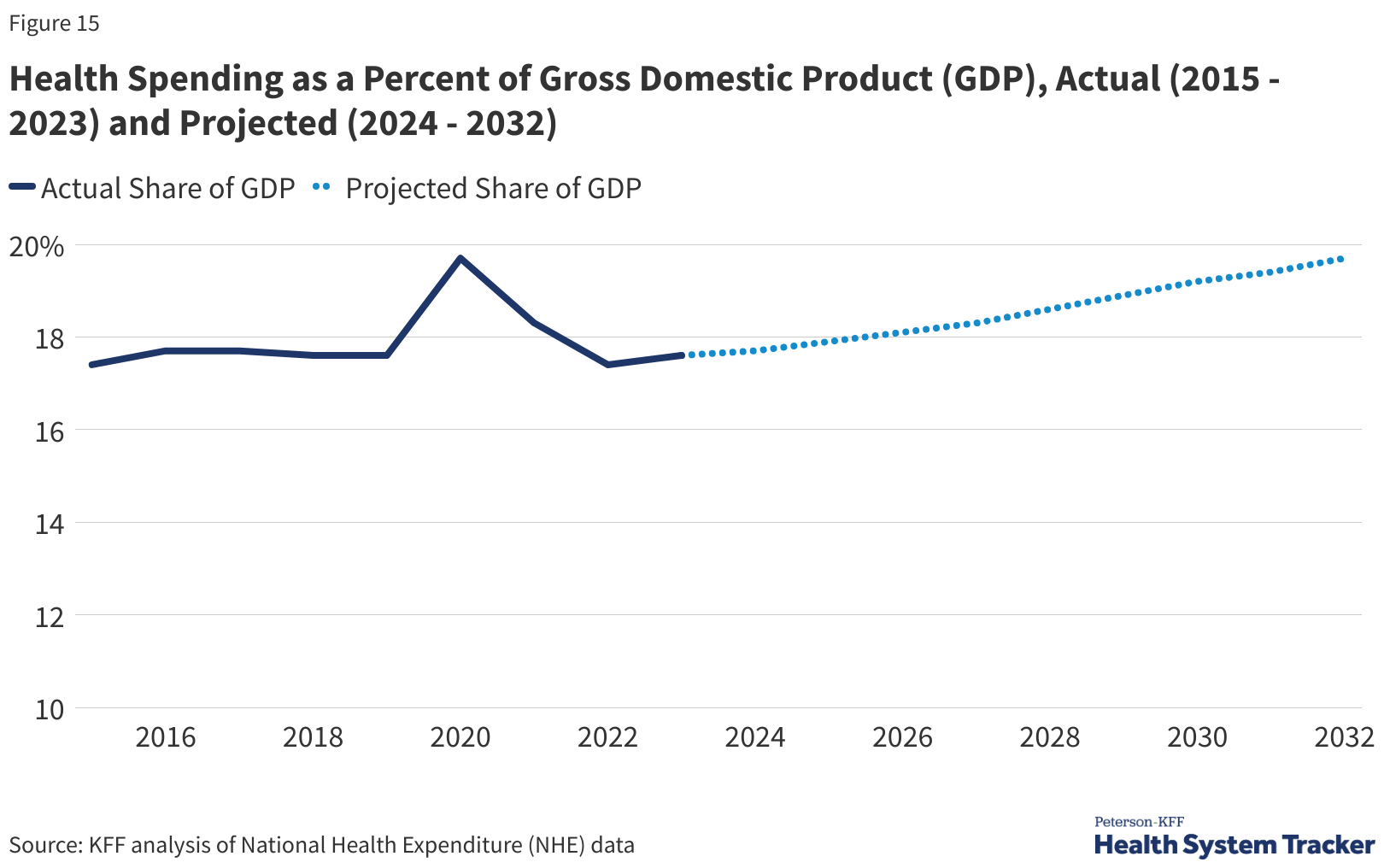

Healthcare cost forecast to 2032

Healthcare is projected to remain a drag on U.S. GDP over the next decade, according to KFF. In addition to an aging population, these costs are rising due to the increasing use of GLP-1 drugs such as Ozempic, new cancer drugs and price increases that outpace inflation.

In other words, as healthcare makes up a larger share of U.S. GDP over time, the government will be less able or less likely to help consumers.