Closing market summary

A final look at the markets before I close the blog for the day. It’s been a messy day for markets, which bounced back from yesterday’s losses in the first hour of trading, only to go into freefall again later. All the main indices in Europe and the US are still down, but have recouped some of their earlier losses.

In London, the FTSE 100 index is now down some 40 points at 6170, a 0.7% fall. Germany’s Dax is trading 0.3% at 8544.76 lower while France’s CAC has slid 0.9% to 3904.31.

On Wall Street, the Dow Jones lost 0.8% to 16,006.76 and the S&P 500 shed 0.75 to 1849.45. US Treasuries rose for a second day as investors sought out safe haven assets from sliding stock markets, despite upbeat jobs and industrial production data.

With that, I’m off. Thankyou for all your great comments, and we’ll be back tomorrow.

Spain struggled to fill its target at a double bond auction. It sold €3.2bn of debt, falling short of the top end of the Spanish Treasury’s target range of €2.5-3.5bn. Spain usually meets or even tops the high end of its target range.

Rabobank analysts said:

This weakness is unsurprising given the very chunky increase seen in all eurozone spreads versus the [German] Bund.

France, on the other hand, had no trouble selling €7.5bn of debt, benefiting from its relative safe-haven status. There was demand for nearly double the amount sold.

EU vows support for Greece

European officials are vowing continued support for Greece as investors sell off the bailed-out country’s stocks and bonds, reports AP.

The country is being buffeted by a range of concerns, including that the government will struggle to wean itself off international aid and that its banks remain shaky. Investors have also been spooked by the prospect of new elections that could bring to power the left-wing Syriza party, which wants to renege on a part of Greece’s debt. A broader global market sell-off has only made matters worse.

Jyrki Katainen, vice-president of the European Union’s executive Commission, said:

There should be no doubt that Europe will continue to assist Greece in whatever way is necessary” so the government can keep financing itself.

European officials are currently reviewing Greece’s progress in complying with bailout loan conditions requiring economic reforms and restrictions on government deficits. Katainen said the commission would work closely with Greece to complete the review and “ensure a smooth evolution of European support” even after the bailout ends.

The European Central Bank is also ready to make more credit available to Greek banks, according to a person familiar with the matter [see earlier post 9:09]. The ECB would do that by providing more credit against collateral such as Greek government bonds.

Greece ran up too much debt and needed €240bn in bailout loans in 2010 and 2012 from other countries that use the euro and the International Monetary Fund. The bailout enabled the government to finance itself after market borrowing costs rose higher than it could afford and threatened to push the country out of the euro currency union.

The country had earlier appeared on the way to recovery and Prime Minister Antonis Samaras had expressed hopes of leaving the bailout program early by doing without remaining installments of bailout loans. Instead, the country would borrow normally on the bond market.

The possibility of such an early exit appeared to recede this week. The yield on the benchmark 10-year rose 0.98 percentage points to 8.71%, from around 5.6% as recently as September. That is a sign investors see an increased risk of not being repaid.

The main stock index in Athens was faring somewhat better, down only 0.6% but that came after a stunning 12% loss over the previous two days.

Updated

US stocks extend fall

On Wall Street, the Dow Jones lost nearly 190 points to 15958, a 1.2% fall, in early trading. The S&P 500 is down 1% and the Nasdaq nearly 2%.

Updated

US industrial output posts biggest rise since Nov 2012

More good news on the American economy, where industrial production jumped 1% in September, the biggest rise since November 2012 (versus expectations of a 0.4% gain). ING economist James Knightley said:

Today’s data suggests that the US economy remains in pretty good shape even if bond and equity markets have their doubts. Jobless claims plunged to 264,000 last week, the lowest reading for over 14 years, which indicates that payrolls growth should accelerate.

Manufacturing rose 0.5% even while auto output fell 1.4%MoM. Utilities output rose 3.9% and mining jumped 1.8%. All in all these are a really strong set of numbers that point to very decent GDP growth numbers for both 3Q and 4Q14, especially when you add in the huge boost to household spending power from plunging gasoline prices. Falling mortgage rates in the wake of the bonds market moves should also be supportive for growth. The risk that we have to be alert to is that the fall in equities and Ebola concerns sap confidence and households save this windfall.

Markets are looking messy...

Here is a handy round-up of the market action from independent City analyst Louise Cooper.

Safe assets in demand:

10yr German bunds fall to record intraday low of 0.716%

10 year UST yield fallen 58bp to 2.06% in one month

Gold has gone from $1190 at beginning of October to $1240 (up 4.2% in just over a week)

Risky assets spurned:

FTSE100 currently down 1.6% today

DAX down 1.3% today

CAC down 1.8% today

US futures currently indicating that the Dow Jones will open 1% lower at 2.30pm London time (after closing 1% lower last night).

Greek stock market fallen 35% since mid June

Greek 10yr bonds up from around 5.6% at beg Sept to 8.75% yield

ICE Brent crude has fallen from $88.25 to $83 in the last three days

Updated

Ross McEwan, the boss of Royal Bank of Scotland, has warned that the bailed out bank’s customers are concerned about the impact of rising interest rates on their mortgage repayments and described the number of complaints about the industry as “nothing short of appalling,” writes Jill Treanor.

A year into his role running the 81% taxpayer-owned bank, McEwan told the BBA conference that 1.5m people have bought their homes since 2007 so have never experienced the impact of a rise in interest rates and the bank intended to conduct extensive research on how customers react to rate rises. The information will be handed to regulators.McEwan said this was a moment for RBS to win back trust from its customers about how they would treated once mortgage rates started to rise and it might make it difficult for them to manage their household budgets.

Admitting that the timing of a rate rise from the historic lows of 0.5% was difficult to predict, McEwan said:

In particular we know that our mortgage customers are seeing conflicting reports about the timing of interest rate rises and they are concerned that they might not be able to balance their household budgets when the day comes, even if that is some time well into the future. This anxiety comes despite the fact that, like most banks, RBS and NatWest have stress tested our customers’ affordability in the event of a significant rise in interest rates up to 7%.

He said RBS would explain to customers how it would manage interest rate rises.

Our customers expect us to handle this issue with transparency and with thoughtfulness. That is what our bank intends to do and what I think we as the UK banking industry need to do.

McEwan said the 2.5m complaints against the industry this year was “nothing short of appalling”. “In any other industry that would be regarded as a crisis,” said McEwan. He also warned that RBS faced a slew of regulatory issues, signalling fines for forex trading and the IT meltdown in 2012.

Updated

US jobless claims lowest in 14 years

Amid all the gloom in markets, data just showed the number of Americans filing new claims for jobless benefits fell to a 14-year low last week. But European stock markets seem to be ignoring the news. The FTSE 100 is still down over 100 points, or 1.7%, at 6107.12. Germany’s Dax has lost 1.7% and France’s CAC is 2.2% lower.

The FTSE is heading for its sharpest two-day fall in three years, but some people think it could bounce back soon.

Patrick Armstrong, chief investment officer at Plurimi, told Reuters:

I don’t think there is any real, clear thing that is creating this anxiety. It seems [this is due to] general fears and people worried about the valuation so I think we’re going to start to see a bounce fairly shortly.

Updated

Seven reasons the world’s stock markets are falling

My colleague, Angela Monaghan, has looked at the reasons why stock markets are falling:

Markets have fallen sharply across the world with a range of anxieties looming large: US economic slowdown, Ebola, German industrial woes, geopolitical tension, the eurozone crisis and fears that a major institution is about to collapse – and it’s October. You can read the full article here.

The FTSE is down more than 100 points now, taking it into technical correction territory, as we observed earlier (a correction being a fall of 10% from recent highs). The recent high of 6,878 was achieved on 4 September.

The dividend yield on the UK market is now over 3.6%, while the 10 year gilt is yielding just under 2%. The Cyclically Adjusted P/E ratio of the UK market suggests UK stocks are now cheaper than they were in 2003, says Laith Khalaf, senior analyst at Hargreaves Lansdown.

The market free fall has continued today, and the FTSE 100 has now suffered a technical correction, falling over 10% since the beginning of September. Markets are in fretful mode, heightened by the spectres of 2008 and 2011, which still haunt investors.

However, long term investors should recognise there will be times like these which are uncomfortable, but when the best policy is to grin and bear it. Indeed, they might well see a glimmer of opportunity in current stock prices. The UK market now looks cheaper than it did at the bottom of the bear market in 2003, according to one long term valuation measure. Things could get well get worse before they get better. But when equities are yielding almost twice as much as gilts, you do have to stop and think where you want your long term savings invested.

Updated

Banks “cringing” in front of regulators

More from the BBA conference where a senior advisor to HSBC chairman Douglas Flint has warned that the new wave of regulations is forcing the bank to perform what he called “preemptive cringe in front of regulators”, writes Jill Treanor.

Describing the way the bank is pulling out of risky business areas, Sir Sherard Cowper-Coles said “risk appetite was shrinking” as a result of new rules.

HSBC was fined £1.2bn by US regulators in 2012 to settle money laundering claims.

Cowper-Coles is on a panel alongside regulators including deputy governor of the Bank of England Sir Jon Cunliffe, who said that consideration about the size of fines was needed.

Cowper-Coles said the “punishment should suit the crime”.

Updated

Goldman Sachs profit boosted by pickup in bond market

Goldman Sachs has reported a 50% jump in third quarter profit, thanks to last month’s sudden pickup in bond market activity, which boosted trading revenue.

Profits for the quarter beat analysts’ expectations, at $2.24bn and earnings were $4.57 per share. Analysts had expected around $3.21 per share. The bank’s total net revenue rose 25 percent to $8.39 billion.

Here’s some more detail courtesy of Reuters:

Revenue from bond-trading, a notoriously volatile business, increased 74 percent to $2.17 billion as strong U.S. economic data, stimulus measures by the European Central Bank, and the surprise exit of trading superstar Bill Gross from giant bond-trading firm Pimco jolted what had been a listless market.

But Goldman’s fixed-income, currency and commodities (FICC) business has been on a declining trend since 2009 as new rules discourage banks from trading on their own book, and many in the industry wonder whether the business will ever truly rebound.

“The combination of improving economic conditions in the U.S. and a strong global franchise continued to drive client activity across our diverse set of businesses,” Chairman and CEO Lloyd Blankfein said in a statement, while acknowledging that “conditions and sentiment can shift quickly.”

Updated

Wall Street is set to join the European sell-off, according to stock futures.

Dow futures now down over 200 points, below fair value. Follow our markets live blog here: http://t.co/TxI1wqrrfj pic.twitter.com/FCNBpbfMEt

— CNBCWorld (@CNBCWorld) October 16, 2014

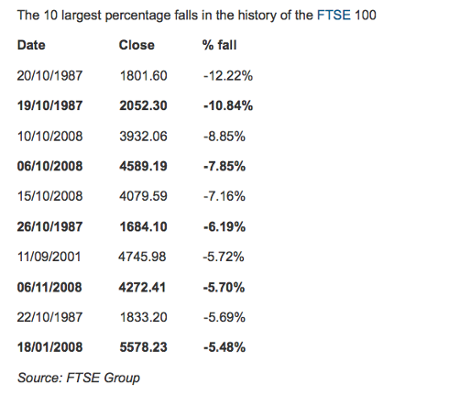

The Footsie is now down more than 10% from its recent peak of 6878, reached on 4 September. The all-time high for the index was 6950, hit on 31 December 1999.

The sell-off on European stock markets is gathering pace. Germany’s Dax is now down nearly 2% and earlier broke through the 8400 level, while France’s CAC has slid 2.8%. All the main European indices are nursing heavy losses, with banks among the biggest fallers.

Updated

#FTSE The next question is does it take out June '13 lows? Seems as if it will do so, vigorously. #bringbackcapitalism #banQE

— Jonathan Davis (@J0nathanDavis) October 16, 2014

October is the cruellest month?

October is the cruellest month... ?

The Wall Street crash of 1929 happened in October, as did Black Monday in 1987. However, it is worth noting that September has had its share of Black Days too, and sometimes the reaction is simply delayed into October (the catalysts that set off both the 1929 crash and the 1907 panic happened in September or earlier). More here on Investopedia.

Updated

Greek 10-year bond yields rose by one percentage point today 8.86%.

The euro has sunk to the day’s low of $1.2756, down 0.6%. Against the yen, it hit an 11-month low of 134.98 yen.

Updated

European banks and construction stocks are the worst hit, as they are sensitive to economic conditions. The eurozone’s banking index tumbled 5.2% while the European construction index lost 3.2%.

Updated

European stock markets slide; German Bunds hit new record low

it’s all kicking off again. German ten-year Bund yields have hit a new record low of 0.718%. Germany’s Dax has lost 0.9%, France’s CAC has slid nearly 2%, Italy’s FTSE MiB has tumbled 3.5% and Spain’s Ibex has fallen 2.8%. The FTSEurofirst 300 has tumbled 2.5% and it hits worst level since early September last year.

FTSE Eurofirst is now down 10.6 per cent this month - a technical correction. Europe fear index at two-year high.

— Robin Wigglesworth (@RobinWigg) October 16, 2014

Updated

FTSE tumbles over 2%

The Footsie continues on its downward path, now down more than 130 points at 60821.73, a fall of over 2%. There are only four risers on the index.

Updated

In volatile trading, the FTSE 100 is now down 1.1%, a fall of more than 70 points, at 6137.44 – having started the day up 1.1%.

Updated

Returning to the 0.3% inflation figure for the eurozone, ING economist Martin van Vliet says:

The very low inflation reading for September will reinforce concern that the Eurozone remains on a slippery slope to deflation.

Until recently the consensus view was that headline inflation in the Eurozone would gradually start to pick up again from Q4 onwards. But now that oil prices have tanked, headline inflation may stay close to zero for longer and not reach 1% before Q4 of next year (if at all). Financial markets also seem increasingly concerned that Eurozone inflation could get stuck below the ECB’s 2% target ceiling. Indeed, the ECB’s favourite gauge of inflation expectations, the five-year, five-year forward inflation-swap rate is currently trading at a record low of 1.72%, which will not be received with much enthusiasm at the ECB.

All in all, with the cushion against deflation getting smaller and smaller and economic growth in the Eurozone stagnating, pressure on the ECB to extend its purchase programmes by adding government bonds may become overwhelming over the next few months.

Oil prices lowest since 2010

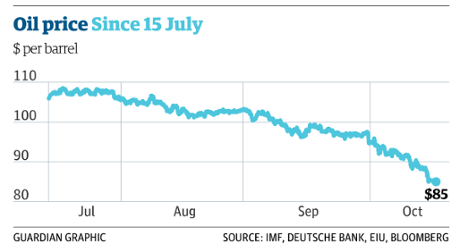

Oil extended yesterday’s heavy losses and dropped more than $1 a barrel to a four-year low. Growing worries over the global economy sent Brent crude, the global benchmark, to $82.72 a barrel earlier this morning, the lowest since November 2010. It is now at $83.09 a barrel. Brent has lost more than 28% since June when it hit a high of $115.71.

Analysts at JBC Energy said:

The $30 fall since June has led to an intense discussion whether prices could be in for a new norm.

FTSE 100 in the red

Markets are all over the place today. The FTSE 100 index has moved into the red, trading nearly 40 points lower, or 0.6%, at 6174.91. Germany’s Dax and France’s CAC are also in negative territory.

Enough banker bashing, says City minister

More from the BBA conference. Jill Treanor reports:

Andrea Leadsom, City minister, has told the BBA conference that she “wants to move the debate forward, away from banker bashing of the past”. A former member of the Treasury select committee, Leadsom is a former banker and did plenty of bashing of bankers when she sat on the committee until taking her current post in April.

Leadsom said the government was pleased with the switching service - set up to make it easier for customers to guarantee they can move their bank account in seven days - and the new criminal rules being introduced. “If you manipulate a benchmark you can end up in prison,” Leadsom said.

Eurozone reports €9.2bn trade surplus

Separate Eurostat figures show the eurozone recorded a trade surplus of €9.2bn in August, up from €7.3bn a year earlier, but down from July’s revised figure of €21.6bn. Seasonally adjusted exports dropped 0.9% while imports tumbled 3.1%.

Eurozone inflation at 0.3%, a five-year low

Annual inflation in the 18-nation eurozone has come in at 0.3% for September, a five-year low (in August it was 0.4%). Eurostat confirmed an earlier flash estimate.

Economists worry that price growth could soon turn negative, with the eurozone stuck in a feeble recovery. This is adding pressure on the European Central Bank to act.

Updated

Gilts edge lower after yesterday's stellar gains

UK government bond prices edged lower today after yesterday’s stellar gains when a market panic drove investors into safe haven assets.

Yields on ten-year gilt yields rose to just over 2% while 30-year yields increased to 2.77%. The latter hit a record low of 2.704% yesterday, while ten-year yields lost more than 18 basis points.

RBS bond strategist Simon Peck said there had been little fundamental economic news to justify yesterday’s moves.

Updated

Legendary investor Warren Buffett has sold more Tesco shares, after admitting earlier this month that he had made a “huge mistake”. Sean Farrell has all the details.

Updated

In the meantime, UK drugmaker Shire – whose US suitor AbbVie abruptly changed its mind after the Obama administration got tough on tax inversions – put out a terse statement:

The board of Shire notes the announcement by AbbVie of its board’s decision to withdraw its recommendation of the offer for Shire.

The board of Shire is considering the current situation and a further announcement will be made in due course.

Updated

Back to the BBA’s annual conference. Jill Treanor reports:

Cathy Jamieson, shadow financial secretary to the Treasury, has put banks on notice that Labour’s aim is to create two new challenger banks and introduce a market share test for competition to bolster competition on the high street. Labour also intends to tell banks to publish the number of employees earning more than £1m, she said.

Jamieson also set out her concerns about the upcoming referendum on Europe. She said she was “concerned that the referendum timetable is creating huge uncertainty for business and financial services” and stressed that Labour thinks that the UK “should have a seat at the table”.

She added “I don’t think it’s helpful” that the government is challenging the EU bonus cap. Asked about fines and said she took no pleasure in seeing fines but stressed that “if there was wrongdoing, people have to take the consequences”

Bowler concludes:

The closing months of 2014 mark the five-year anniversary of the end of the greatest economic slump since the 1930s. While we at The EIU are not expecting another worldwide crash, we have once again lowered our estimate for global GDP growth in 2014 and our forecast for 2015. What began as a promising year for the global economy will end on a sombre note.

Bleak conditions in eurozone seen as biggest drag on global growth

The bleak conditions in the euro zone continue to be the greatest drag on global growth according to The Economist Intelligence Unit, which has further lowered its 2015 global GDP forecast from 2.4% to 2.3% and its eurozone GDP growth forecast from 1.2% to 1.1%.

According to John Bowler, director at The Economist Intelligence Unit:

Despite the fact that weakness is apparent on a number of fronts, Europe is at the heart of the latest global slowdown. Only a handful of member states in the European Union, led by Poland, have seen output recover to the level reached before the recession. While Germany, France and the UK have regained what they lost, Italy, Spain, the Netherlands and Ireland remain in negative terrority.

Germany, traditionally the engine of the European economy continues to be hurt by the Russia sanctions, with its August industrial production falling by the fastest rate since January 2009.

The EIU believes the US recovery remains on track, keeping its 2015 GDP growth forecast at 3.2%. Employment continues to soar, which should in turn start to push up wages, further supporting the recovery. However the slowdown in other countries poses a risk to the US next year, the EIU judges.

China’s economy, after stabilising at mid-year, is softening again and as a result the EIU has cut its 2014 GDP growth estimate from 7.5% to 7.3% but maintains its 2015 global forecast of 7%. China should successfully manage a measured slowdown as it squeezes excesses from its financial system.

Looking at financial markets, the EIU says:

Global financial markets have been retreating as fears of the slower economic growth take hold. The crippling slowdown in Europe’s economy and the unsettled state of emerging markets are pushing some investors close to panic.

Of the four traditional asset classes (stocks, bonds, currencies and commodities), the most worrying is the price of oil, which has consistently been above US$100/barrel for the last two years. Weak growth, particularly Europe and China, is curbing demand for energy at a time when production, especially in the US, is rising rapidly. As a result the EIU has reduced its forecast for the price of oil (dated Brent) to US$97.60/barrel in 2015 from US$102.50 previously.

Updated

The $100bn question

Anthony Browne, boss of the British Bankers’ Association, has kicked off the annual conference of the industry’s lobby group by discussing what he calls the “$100bn question,” our banking correspondent Jill Treanor reports. Browne said:

One question that is particularly topical that we have today called the $100bn question - is the level of fines coming out of the US. So I’m looking forward to the discussions of the impact those huge fines are having on banks’ behaviour as they try to derisk their businesses, ending services that could expose them to balance sheet altering penalties.

Banks such as HSBC have warned about the fear of fines making them less likely to take risks and Browne picked up on this theme, popping to banks pulling services from people wanting to send home to sub-Saharan Africa, exporter and charities trying to get money to worn-torn countries because of fear they are processing money for “terrorists or drug traffickers”.

Yields on Greek 10-year government bonds have topped 8% for the first time since February, amid concerns over early elections and Athens’ plans to wean itself off international aid.

ECB trims haircut on Greek banks' collateral

Reuters is reporting that the European Central Bank has reduced the haircut it applies on bonds submitted by Greek banks as collateral to borrow funds, to boost their access to liquidity.

A Greek central bank official told Reuters:

The move was decided late on Wednesday evening after talks between the government, the ECB and Greece’s central bank governor. It’s a supportive move given the pressures in the last two days.

The official said this means that an extra €12bn of liquidity could be tapped by Greek banks. Bank of Greece governor Yannis Stournaras was in Frankfurt on Wednesday.

Most European markets tumble again; FTSE still positive

The recovery in European stocks has already petered out, less than an hour into trading. Some indices are tumbling again, such as Italy’s FTSE MiB which is now down 1.1%, and Spain’s Ibex has lost 1.3%. France’s CAC has also turned negative, and is trading 0.7% lower.

The FTSE 100 index is still in positive territory but has pared gains, trading 18 points higher at 6230.10, a 0.3% increase. Germany’s Dax is flat.

Updated

The AbbVie-Shire deal is the biggest so far to be wrecked by new US rules on tax inversions, designed to make it harder for American multinationals to shift their tax base abroad to cut their tax bills.

...so whither AbbVie? It’s an embarrassing, and costly, failure for boss Rick Gonzalez – especially because he had insisted that the deal wasn’t just about tax savings.

“We now know AbbVie was flying by the seat of its pants,” says Neophytou at Panmure Gordon.

With reputation at stake and possible litigation to face, why did AbbVie’s board have such a dramatic change of heart? Perhaps it hopes to recoup its costs by suing the US government. Its intention is possibly hinted by “...impact of the U.S. Department of Treasury’s unilateral changes to the tax rules...target specifically a subset of companies that would be treated differently than either other inverted companies or foreign domiciled entities...” in this morning’s press release.

Updated

The only consolation for Shire is that it will get a big break fee of $1.6bn. But its executives are losing out on retention payments worth £19m. Where next for the rare diseases specialist?

Panmure Gordon analyst Savvas Neophytou says:

In our view the fundamentals of the [Shire] business remain strong and valuation now looks attractive. We upgrade our recommendation to Buy (from Hold) and set a new price target of £42.

Investors will worry that Shire’s defence plans are too ambitious. As part of its defence, Shire made a compelling case to revenue base of $10bn by 2020. For a company growing consistently in double digit range, the implied CAGR [compound annual growth rate] of 12-13% appears achievable. The company remains acquisitive...

It is possible that the loss of four months strategic direction may have damaged those plans. Key staff may have made their own exit plans. However, Shire’s rare diseases business remains an attractive asset and we expect Shire to have multiple suitors.

Updated

European stocks bounce back; Shire only loser on FTSE 100

European stock markets have bounced back more strongly than expected. The FTSE 100 index in London gained more than 60 points, a 1.1% rise, to 6280 in the first few minutes of trading.

Shares in Shire are the only loser: they’ve slumped another 11% to £35.68 after yesterday’s 22% drop, after the UK drugmaker was spurned by US rival AbbVie. After the surprise news yesterday that it was reconsidering its agreed £34bn takeover of Shire, the AbbVie board called on shareholders to reject the deal in a statement this morning. Shire makes hyperactivity drugs and treatments for rare diseases, while AbbVie produces the world’s top-selling medicine, Humira for rheumatoid arthritis.

Germany’s Dax increased 0.6% in early trading, France’s CAC and Spain’s Ibex both added 0.7% while Italy’s FTSE MiB is up 0.8%.

Updated

Oil prices have fallen further today. Brent crude is down 0.85% at $83.07 a barrel while New York light crude has lost 1.4% to $80.67 a barrel.

Paul Ashworth, chief US economist at Capital Economics, believes the panic in financial markets is overdone.

The growing sense of market panic evident in the sharp declines in equity prices and the strong rally in US Treasury bonds over the past week is hard to square with the solid outlook for US economic growth. We would still argue that the declines in oil prices and long-term interest rates will provide a net boost to real US GDP growth, even after allowing for the sell-off in stock markets.

While the prospects for economic growth in the euro-zone have deteriorated, the outlook for global economic growth hasn’t changed that much at all. The impact of that eurozone slowdown on the US economy will be modest anyway.

The US economy hasn’t suddenly gone into a nosedive. The slump in oil prices will also help to boost real incomes and, consequently, real consumption of other goods and services. Retail gasoline prices should slip below $3.00 a gallon soon. Lower long-term interest rates will boost investment and housing. We calculate that GDP increased by around 3.0% annualised in the third quarter and we anticipate a similar sized gain in the fourth.

If US economic growth remains close to 3%, as we expect, then there is a strong likelihood that these latest market moves will be reversed sooner rather than later and that the Fed will still begin to hike rates sometime in the first half of next year.

Updated

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and the eurozone.

European stock markets are expected to open slightly higher today after yesterday’s sell-off. Poor US economic data triggered fresh fears over global growth, compounded by the rapid spread of Ebola in west Africa. US, UK and German bond yields also fell sharply and the price of oil hit a four-year low.

Asian stock markets extended the losses seen in Europe and the US, with Japan’s Nikkei tumbling 2.2% and Hong Kong’s Hang Seng down 0.7%.

We will get eurozone inflation data for September later, as well as US weekly jobless claims, industrial production for September and the Philadelphia Fed manufacturing survey for October.

Michael Hewson, chief market analyst at CMC Markets UK, said:

The Fed Beige Book overnight did manage to paint a fairly positive outlook for the US economy, but that doesn’t appear to be enough anymore to keep stocks at the levels we’ve become used to in recent weeks.

Updated