/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Palantir (PLTR) shares are losing ground on Friday following reports a battlefield communication system the company co-developed with Anduril Industries has significant cybersecurity flaws.

NGC2 – a platform designed to integrate real-time data across military assets – was flagged in an internal U.S. Army memo today as a “very high risk” system that could allow adversaries “persistent undetectable access.”

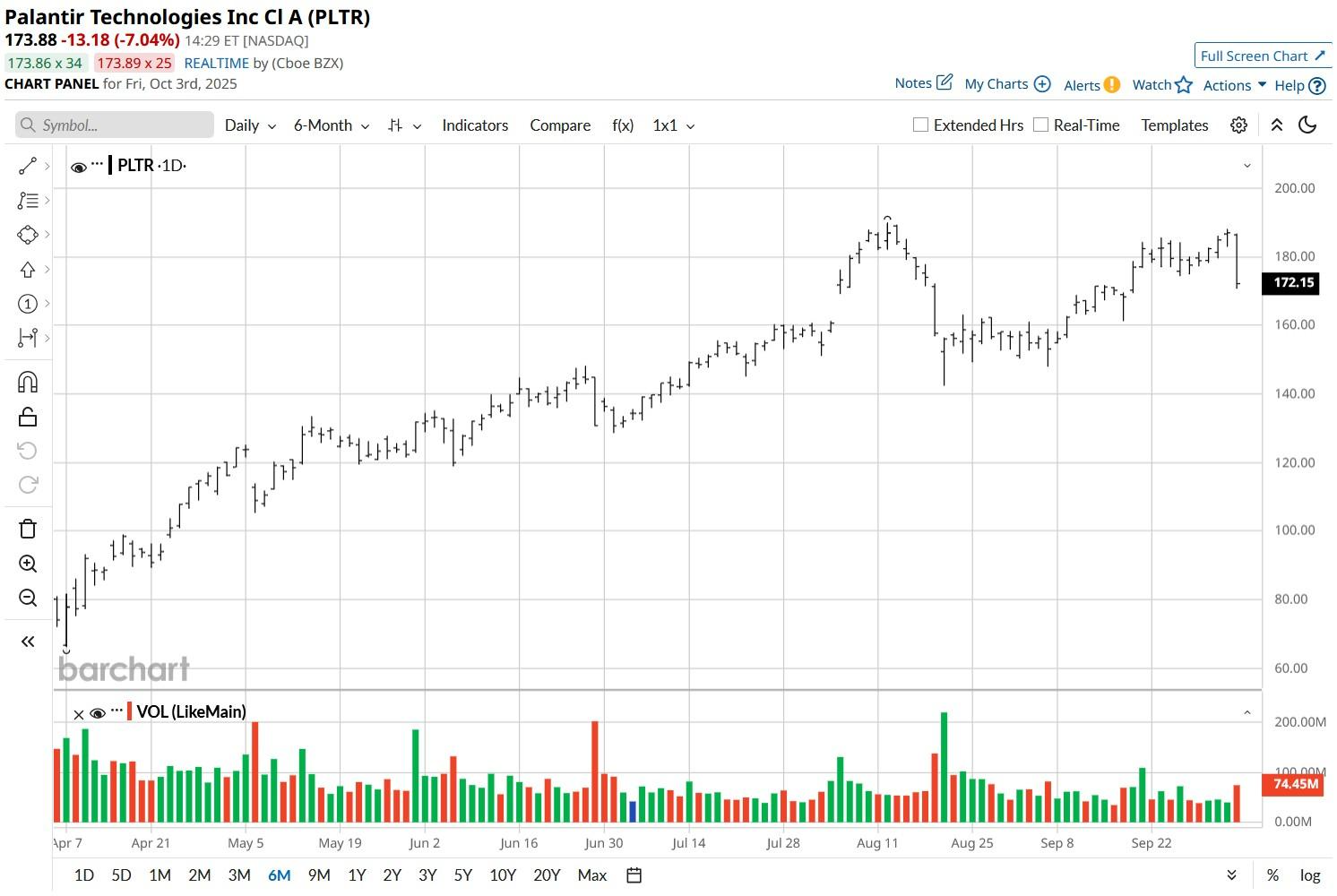

Despite the pullback, Palantir stock remains up some 175% versus its year-to-date low in January.

What the NGC2 News Mean for Palantir Stock

Investors are bailing on PLTR stock this morning primarily because much of its valuation is based on the company’s success in winning lucrative, long-term U.S. government and defense contracts.

But the Army memo exposing security loopholes in the NGC2 platform directly threatens that core business narrative.

Lack of user access control and unaudited third-party code, as indicated in the memo, compromise the system’s ability to protect sensitive, raising concerns about reputational damage and delays or loss of future defense contracts.

In the near term, this forces the data analytics behemoth to incur unexpected cost to quickly fix the issues.

Together, all of it could trigger a prolonged selloff in Palantir shares as investors re-evaluate the company’s reliability as a key defense technology provider.

Is It Worth Buying PLTR Shares on the Pullback?

Investors are recommended caution in buying the dip in Palantir shares as they’re still trading at a massive premium, pricing in flawless execution across artificial intelligence (AI)-enabled defense technologies.

At the time of writing, the Nasdaq-listed firm is going for forward price-earnings (P/E) multiple of about 425x, which suggests minimal room for operational missteps.

Moreover, insiders have been aggressive sellers of PLTR shares over the past three months, which signals one of two things:

- The management agrees Palantir is egregiously overvalued at current levels

- Executives’ confidence in the company’s long-term prospects is waning

In short, until Palantir shows tangible evidence of focused remedial measures and transparency – jumping into buy the dip appears highly premature.

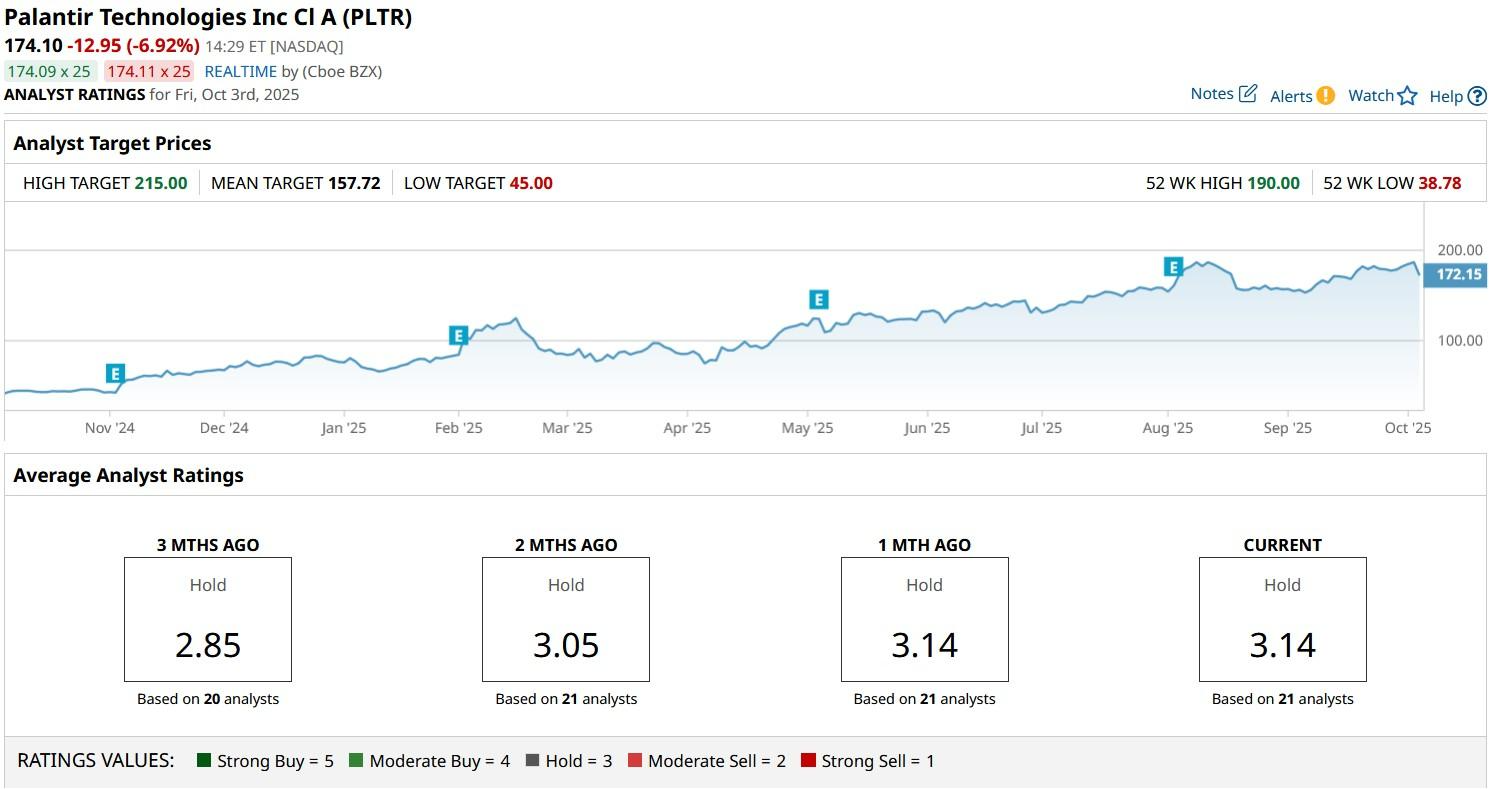

Wall Street Sees Significant Further Downside in Palantir

Wall Street also agrees that Palantir stock is concerningly overvalued at current levels.

The consensus rating on PLTR shares sits at “Hold” only with the mean price target of about $158 indicating potential downside of another 12% from here.