/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Set to report its earnings today, artificial intelligence (AI) bellwether Nvidia (NVDA) recently unveiled the latest version of its robotics chip module, the Jetson AGX Thor. On sale for $3,499 as a developer kit, Nvidia says that it is 7.5 times faster than its previous generation. Commenting on the development, Nvidia’s vice president of robotics and edge AI, Deepu Talla, said: “We do not build robots, we do not build cars, but we enable the whole industry with our infrastructure computers and the associated software.”

Nvidia's Keen Focus on Robotics

Nvidia's thrust on robotics comes right from the top, with CEO Jensen Huang being particularly excited about the space, touting it to be a “multitrillion-dollar growth opportunity” for the company. Notably, with the Jetson AGX Thor, Nvidia takes a major step forward by introducing its latest Blackwell-generation GPU compute architecture into both industrial and consumer/humanoid robotics.

Alongside the new hardware, the company offers a range of software platforms and tools tailored for robotics applications. Nvidia's Jetson software platform has been upgraded to support the latest boards, with the Isaac Groot humanoid robot foundation models and Nvidia Metropolis for Vision AI integrated to further improve robotics development and deployment capabilities.

Still, despite being one of Nvidia's fastest-growing segments, robotics currently only contributes just 1% of the company's overall revenues.

However, with a humongous market capitalization of $4.4 trillion, Nvidia's position as the most valuable company in the world is driven by several other factors, making it an investor's paradise. What are they? Let's take a closer look.

At the Center of the AI Revolution

Let alone the 35.6% uptick seen in NVDA stock on a YTD basis, it is up 5% since my last analysis of the company. Not much has changed since then, as Nvidia remains at the forefront of the AI revolution.

Nvidia has expanded its impressive product portfolio with the introduction of the Blackwell Ultra, a next-generation GPU architecture engineered for the demanding requirements of large-scale AI reasoning workloads. Built on the foundation of the broader Blackwell family, the Ultra version offers substantial gains in computational throughput, memory capacity, and power efficiency, specifically designed to support modern AI infrastructure at scale. In dense low-precision compute performance, Blackwell Ultra exceeds the standard Blackwell GPU’s capabilities by approximately 1.5 times, reaching 15 PFLOPS compared to 10 PFLOPS for its predecessor. Memory capacity has also seen a major enhancement, with a maximum of 288 GB, an increase from 192 GB on the standard Blackwell GPU and more than triple the 80 GB available on the H100. Compatibility with Nvidia’s CUDA ecosystem remains central, preserving one of the company’s most substantial competitive advantages in the market.

Further, with an estimated 92% share of the GPU market, Nvidia’s product range keeps it firmly positioned at the forefront of the AI infrastructure build-out among hyperscale operators, whose capital expenditure programs continue to accelerate. Microsoft’s (MSFT) fourth-quarter fiscal 2025 capital spending reached $22.6 billion, marking a 53% year-over-year (YoY) rise. The company has reiterated plans for $80 billion in AI-related capex for the fiscal year, representing a substantial increase over prior years.

Amazon’s (AMZN) projections are even more aggressive, with 2025 capital expenditures expected to surpass $100 billion, up from $83 billion in 2024, with the majority directed toward AI infrastructure. Meta (META) has likewise intensified its investment push, doubling capital spending year over year as it scales its AI Superintelligence program. The company has raised its full-year capex guidance to between $66 billion and $72 billion from its earlier forecast of $60 billion to $65 billion, with AI infrastructure expansion cited as the top priority.

Financials as Good as They Can Be

Nvidia’s unmatched leadership in the semiconductor space, combined with its ongoing focus on scaling and innovation, has not come at the expense of its financial discipline or performance. Rather, the company has continued to deliver a string of strong results that reinforce its position as one of the most consistently high-performing firms in the market today, with 10 year revenue and earnings CAGRs of 41.15% and 61.71%, respectively.

In fiscal Q1 2026, Nvidia posted revenue of $44.1 billion, reflecting a substantial 69% rise compared to the same period a year ago. This exceptional performance was driven primarily by its data center business, which accounted for $39.1 billion in sales, representing annual growth of 73%, and further cementing its importance as the company’s key growth engine.

Nvidia’s bottom-line performance also stood out, with earnings per share rising to $0.81, surpassing the consensus estimate of $0.75. Looking forward, analysts expect this momentum to carry into the next quarter, with projections indicating earnings of $0.94 per share on revenue of approximately $45.59 billion.

Still, not every figure was without concern. The company’s gross margin slipped to 61%, significantly lower than the 78.9% recorded in the corresponding period last year. Despite this decline, Nvidia remains the dominant player in the GPU space, which has helped soothe investor concerns regarding margin pressures and intensifying competition. Management reaffirmed its full-year gross margin target, which remains set in the mid-70% range, signaling sustained confidence in the company’s long-term model and execution.

On the cash flow front, Nvidia continued to display financial strength. Cash generated from operating activities reached $27.4 billion, marking a year-over-year increase of 79.1%. The company concluded the quarter with $53.7 billion in cash and equivalents and no short-term debt obligations, highlighting the firm’s robust liquidity position and reinforcing its flexibility to fund capital expenditures, acquisitions, and future strategic initiatives.

At the broader level, Nvidia’s forward-looking estimates remain well ahead of the industry. Analysts currently expect revenue and earnings growth rates of 62.38% and 68.31%, respectively, which far exceed the sector medians of 7.56% and 11.09%, providing further evidence of the company’s continued outperformance and leadership in its field.

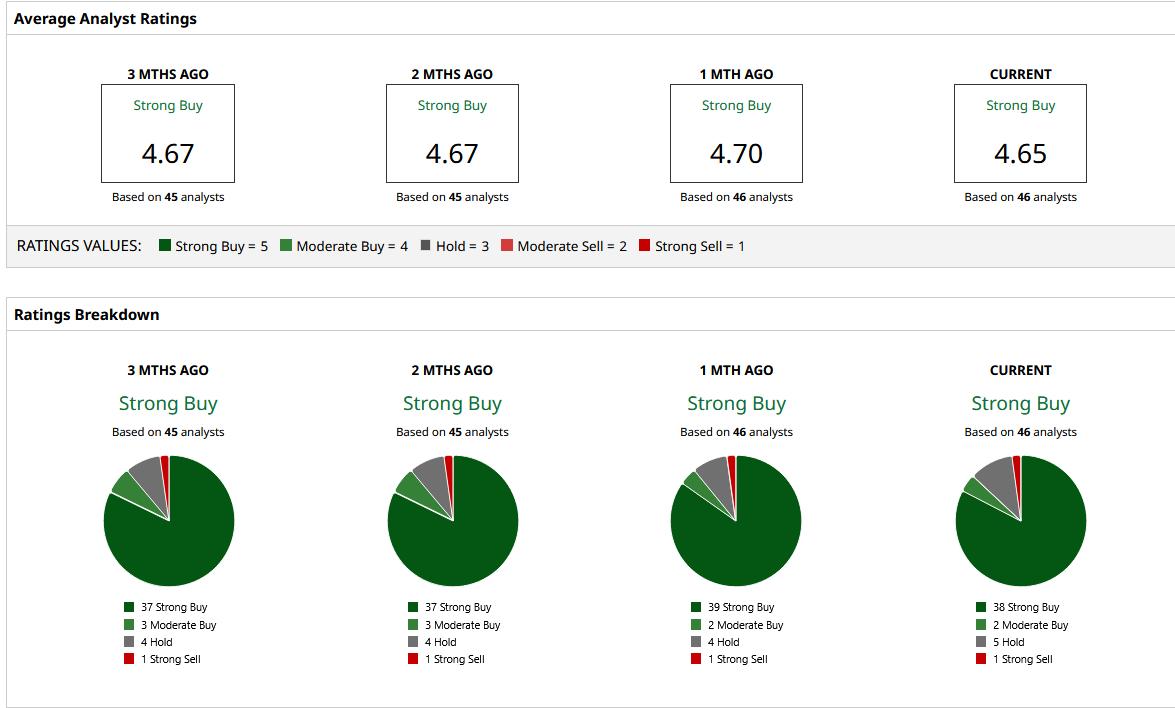

Analyst Opinions on NVDA Stock

Taking all of this into account, analysts have attributed a rating of “Strong Buy” for NVDA stock, with a mean target price of $198.35. This indicates upside potential of about 9.1% from current levels. Out of 46 analysts covering the stock, 38 have a “Strong Buy” rating, two have a “Moderate Buy” rating, five have a “Hold” rating, and one has a “Strong Sell” rating.