/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

Optical names grow larger and more power-hungry while chipmakers and networking firms race to build faster and more efficient ways to move information between servers. That has made optical interconnects a key growth area.

This is where Marvell Technology (MRVL) comes in. The company recently acquired Polariton Technologies, a move that should strengthen its optical photonics capabilities and help it push toward higher-speed connectivity as AI workloads continue to climb. By adding Polariton’s silicon photonics expertise, Marvell is aiming to improve bandwidth, power efficiency, and integration across next-generation data-center networks.

For investors weighing whether MRVL stock is a buy or sell, this deal adds another layer to the company’s AI story. Marvell is not just riding the wave of demand for advanced chips, but trying to position itself deeper inside the infrastructure that powers the next phase of AI growth.

Why This Deal Matters for Marvell

On one hand, Marvell is already a major player in data infrastructure. It sells chips for networking, storage, and custom AI work. On the other hand, the AI boom is forcing cloud builders to spend more on optical interconnects, and that is where Polariton fits in.

Polariton brings plasmonics-based silicon photonics technology to the table. Marvell said the deal will enhance its optical technology portfolio and help it scale toward higher bandwidth and better power efficiency. That is a pretty clean fit for the AI story. If data centers keep growing the way they have been, Marvell could become even more important in the hardware stack.

Markets liked the move. MRVL stock got a lift after the announcement, which tells you investors see this as more than a small tuck-in deal. They see it as another sign that Marvell wants to own more of the AI infrastructure chain.

What Does the Valuation Say About MRVL Stock?

MRVL stock has already had a huge run and surged with the AI chip wave. The stock is up roughly 80% year-to-date (YTD) and has nearly tripled over the past year. The rally follows a big earnings beat and partnerships — from Nvidia’s (NVDA) NVLink Fusion to Amazon's (AMZN) AWS Trainium — that have fueled growth. The 2025 decline has reversed into a steep climb as investors price in continued AI-led data-center demand.

Marvell has been tying itself more tightly to the biggest names in AI and cloud computing. Its work with Nvidia on data-center connectivity has drawn a lot of attention. So has its role in the broader custom AI chip ecosystem.

But here comes the real test. At around 54 times forward earnings, MRVL stock does not look cheap. Additionally, the price-to-book ratio is 10 times, significantly above the sector median, suggesting that MRVL is trading at a premium.

That does not make the stock automatically expensive in a bad way. It just means the bar is high. If Marvell keeps delivering strong growth, the valuation can make sense. But if growth slows, shares could get hit hard.

Marvell’s Business Is Still Growing Fast

The good news is that Marvell is not just a stock story. Its latest quarter was strong. In the fourth quarter of 2026, revenue came in at $2.22 billion, up 22% year-over-year (YOY). That was a record quarter. Full fiscal 2026 revenue hit $8.19 billion, up 42% YOY.

The data-center business did most of the work. That makes sense, since AI demand has been driving a lot of spending across the industry. Marvell also showed good earnings power. Net income came in at $396.1 million, while EPS reached $0.80. Finally, cash flow from operations came in at $373.7 million, and the company ended the quarter with about $2.64 billion in cash and equivalents.

CEO Matt Murphy sounded confident on the earnings call. Murphy said the company delivered record fiscal 2026 revenue, driven by robust AI demand, and he expects revenue growth to accelerate again in fiscal 2027. That is the kind of language AI investors want to hear. It tells you management still sees a long runway ahead.

The outlook also looks solid. For Q1 2027, Marvell guided for about $2.4 billion in revenue and diluted EPS of around $0.79. Analysts are also leaning in the same direction, with expectations near that range for the quarter and continued growth for the full year.

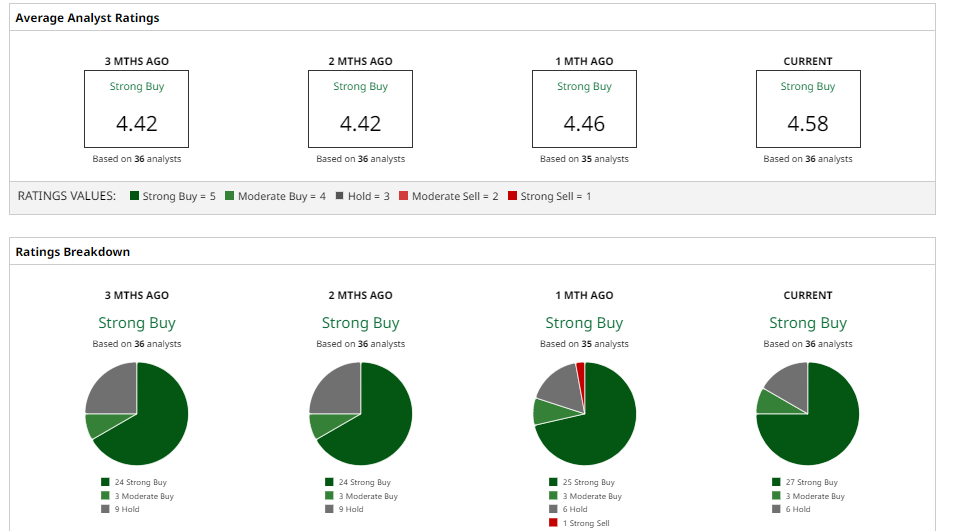

What Do Analysts Think of MRVL Stock?

Wall Street is still mostly positive on Marvell stock, but the opinions are not all the same. Some firms think the company still has room to run, while others believe the stock has already gone a bit far.

RBC Capital recently raised its price target to $170 and kept an “Outperform” rating. GF Securities also turned bullish with a $165 target. Barclays is constructive, too, with a $150 target and an “Overweight” rating. These firms like Marvell’s role in optical connectivity and AI infrastructure.

Morgan Stanley is more cautious. The firm has a $103 target and “Equal Weight” rating on MRVL stock. That is a clear sign that not everyone wants to chase shares after such a big rally.

The broader consensus is still fairly upbeat. Marvell stock has a consensus “Strong Buy” rating with an average target of $126.95, although that number is 17% below where the stock currently trades. That tells investors that Wall Street is positive on the business but less certain on the stock price after the run.