/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Intel’s (INTC) decision to spin out its AI robotics division, RealSense, marks another strategic move in the chipmaker’s ongoing transformation under new CEO Lip-Bu Tan. The $50 million Series A funding round for RealSense, which includes participation from MediaTek Innovation Fund and Intel Capital, signals both the promise of the robotics industry and Intel’s need to streamline operations while maintaining exposure to high-growth markets.

The spinout suggests a calculated approach to asset optimization during a challenging period for Intel. The chip maker is targeting $17 billion in operating expenses for 2025 and $16 billion for 2026. So, divesting non-core assets while retaining minority stakes allows Intel to reduce operational complexity while preserving upside potential.

RealSense, formerly Intel Perceptual Computing, has been developing 3D vision technology for over a decade and serves autonomous robot manufacturers, including Eyesynth and Unitree Robotics.

Intel is under pressure to execute on its foundry strategy and regain a competitive positioning in core markets where it has lost market share to Nvidia (NVDA) and Advanced Micro Devices (AMD). Under Tan’s leadership, the company has adopted a more focused approach, emphasizing customer service and manufacturing excellence.

The Robotics Market Is Huge for Intel

The robotics market opportunity is expanding at an exponential pace, with Morgan Stanley projecting the humanoid robotics market to reach $5 trillion by 2050. However, Intel’s decision to spin out rather than fully divest RealSense suggests management believes the robotics opportunity may not align with the immediate priorities of fixing core CPU competitiveness and foundry execution.

For investors, the spinout showcases disciplined capital allocation and a willingness to unlock value from non-core assets. Intel’s ability to attract external investment in RealSense while maintaining a minority stake indicates strategic thinking about portfolio optimization.

However, the broader context remains challenging. Intel continues to wrestle with manufacturing execution, as it faces supply constraints on Intel 7 while ramping 18A production. The company’s data center market share erosion persists, despite some stabilization efforts with products like Granite Rapids. Competition from both traditional rivals and ARM-based alternatives intensifies across client and server segments.

What’s Next for INTC Stock?

The path forward for Intel stock likely depends more on foundry execution and product competitiveness than robotics spinout proceeds. Tan’s emphasis on organizational flattening, return-to-office mandates, and engineering talent retention suggests awareness of cultural issues hampering innovation. Yet meaningful product leadership recovery will take time, particularly in AI workloads where Intel trails significantly.

Intel stock reported a net loss of $0.13 per share in 2024 and is forecast to end 2025 with earnings of $0.30 per share. Moreover, Wall Street estimates earnings to improve to $2.70 per share in 2028. If INTC stock trades at 15 times forward earnings, it will be priced at $40 in early 2028, indicating an upside potential of almost 90% from current levels.

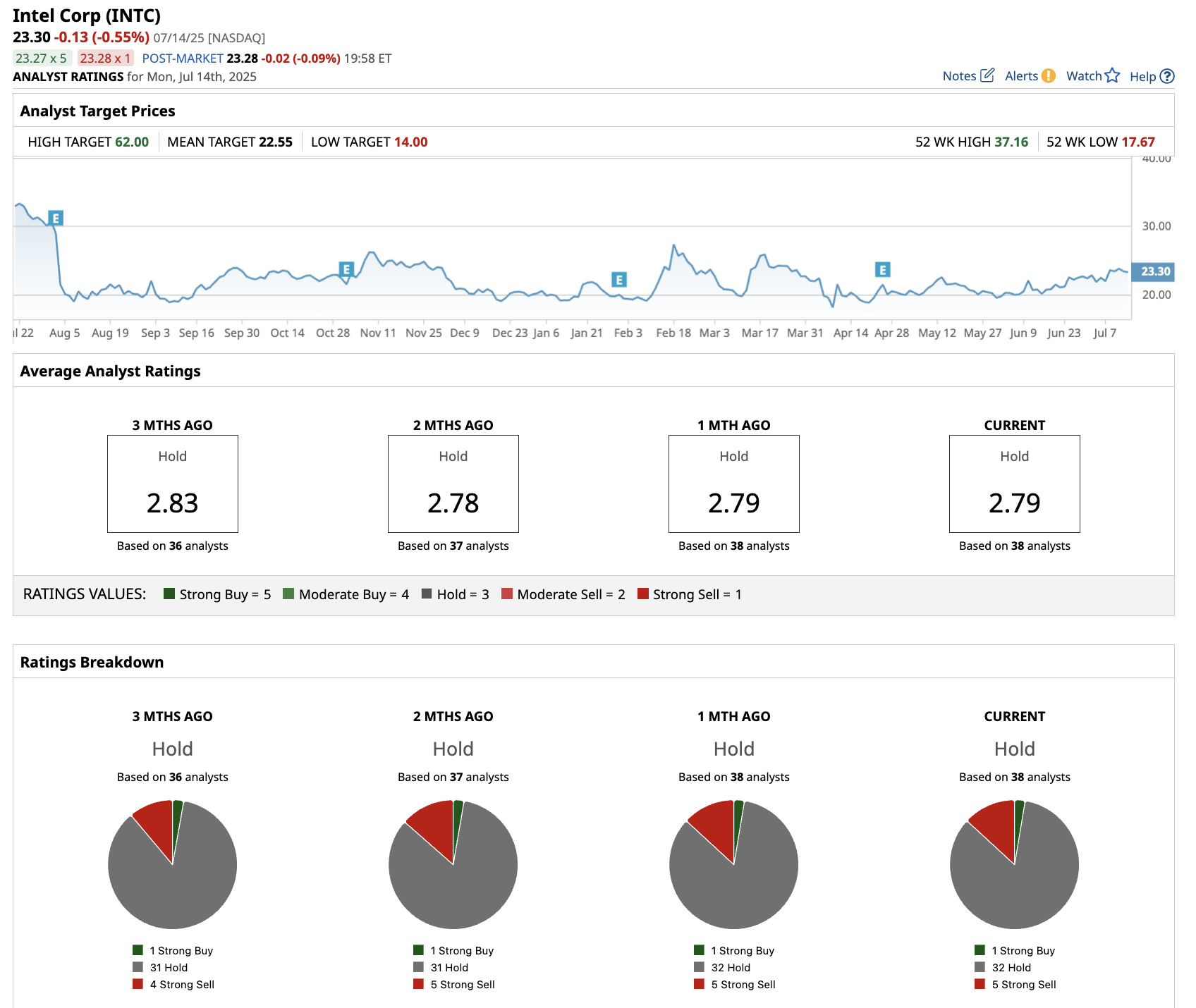

Out of the 38 analysts covering INTC stock, one recommends “Strong Buy,” 32 recommend “Hold,” and five recommend “Strong Sell.” The average target price for Intel stock is $22.55, below the current trading price.