/A%20Tesla%20Cybertruck%20with%20visible%20bullet%20impacts_%20Image%20by%20Karolis%20Kavolelis%20via%20Shutterstock_.jpg)

For the year so far, Tesla (TSLA) stock has witnessed significant volatility. In April, the stock touched lows of $222. There has been a meaningful rally from those levels, with TSLA stock currently trading at $439.

Amidst the rally, there have been multiple concerns that include sales growth deceleration and margin compression. In particular, the company’s Cybertruck sales have disappointed. For Q3 2025, Tesla sold only 5,400 Cybertruck pickup trucks.

The rally in TSLA stock, however, indicates that the markets are looking forward to some impending catalysts playing out in FY 2026 and beyond.

About Tesla Stock

Tesla is still, at its core, an electric vehicle (EV) company but also operates in the energy generation & storage segments and is expanding more into AI and robotics. The company maintains its position among the global leaders in EV sales.

For Q2 2025, Tesla reported 384,000 vehicle deliveries and deployed 9.6 GWh of energy storage products. For the same period, the company’s total revenue was $22.5 billion, which was lower by 12% on a year-on-year (YoY) basis.

Even with global economic deceleration and competition impacting margins, TSLA stock has surged by 84% in the last six months. It is likely that the stock is discounting better numbers in the coming financial year.

Reasons to Be Cautiously Optimistic on Tesla

Some of the headwinds in Tesla’s growth story include competition, global economic deceleration, and geopolitical factors. However, it’s likely that Tesla will overcome the challenges and continue to deliver growth.

An important point to note is that Cybertruck sales numbers have continued to disappoint. However, Tesla’s deliveries growth is largely driven by Model 3 and Model Y. In October, Tesla rolled out its affordable version of Model 3 and Y. It’s likely to have a positive impact on deliveries growth.

Cybercab is expected to be another major growth driver for Tesla. Analyst estimates indicate that Cybercab revenue can reach $1 billion in 2026 and $75 billion by 2030. This would imply 45% of the company’s automobile sales by the end of the decade. Tesla has already launched its first robotaxi service in June. Furthermore, with the Tesla Semi and Roadster also in the pipeline, the outlook is optimistic in terms of delivery growth.

Cash burn was one of the most enduring challenges for Tesla in its initial years. In the last four quarters, the company has reported operating cash flow of $15.8 billion. Further, Tesla has a cash buffer of $36.8 billion. High financial flexibility provides the company with ample headroom to invest in innovation and capacity expansion.

What Analysts Say About TSLA Stock

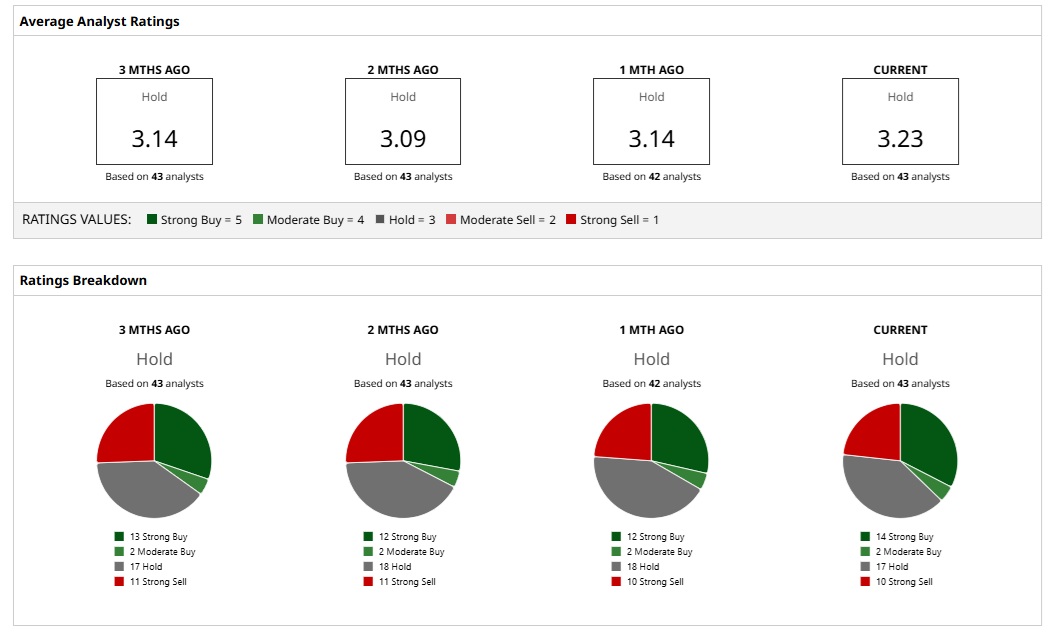

Analyst opinion is seemingly significantly divided when it comes to TSLA stock. Currently, 14 analysts believe that the stock is a “Strong Buy,” while 10 analysts opine that TSLA stock is a “Strong Sell.” However, a majority of them, 17 analysts, believe that the stock is a “Hold.”

It’s worth noting that the mean analyst price target for TSLA stock is $358.3, and it implies a 19% downside potential from current levels. However, the most bullish price target of $600 implies an upside potential of 36.6%.

Overall, there are reasons to be cautiously optimistic about Tesla. An important factor to note is that analysts expect earnings degrowth for the current financial year. However, earnings growth for FY 2026 is expected at 67.24%.

With interest rates trending lower globally, it’s likely that expansionary monetary policies will support economic growth and boost EV sales. This can potentially offset the negative impact of the loss of the $7,500 U.S. tax credit. Further, the robotaxi business is likely to be a key growth catalyst for the next few years.