With a market cap of $2.4 trillion, Alphabet Inc. (GOOG) is a global technology company incorporated in 1998 that operates through three segments: Google Services, Google Cloud, and Other Bets. It offers a wide range of products and platforms such as Search, YouTube, Android, Google Cloud, and healthcare technologies across the U.S., Europe, Middle East, Africa, Asia-Pacific, Canada, and Latin America.

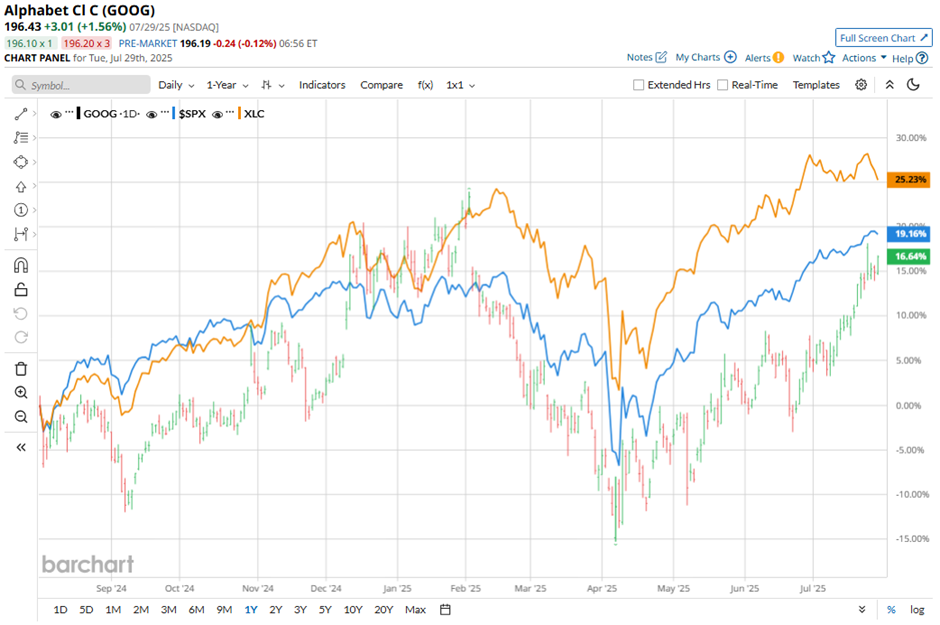

Shares of the Mountain View, California-based company have underperformed the broader market over the past 52 weeks. GOOG stock has risen 14.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 16.6%. Moreover, shares of Google parent company are up 3.2% on a YTD basis, compared to SPX’s 8.3% increase.

Focusing more closely, shares of the internet search leader have also lagged behind the Communication Services Select Sector SPDR ETF Fund’s (XLC) 25.7% gain over the past 52 weeks and 9.6% return on a YTD basis.

Shares of GOOG rose over 1% following its strong Q2 2025 results on Jul. 23, with net income of $5.12 per share and total revenue of $96.4 billion, surpassing expectations. Google Cloud sales surged nearly 32%, beating estimates, and advertising revenue rose 10.4% to $71.3 billion, topping forecasts. Despite investor concerns over a $10 billion increase in capital spending to $85 billion for the year, confidence grew as Alphabet emphasized strong AI-driven cloud demand and highlighted new wins like OpenAI joining its cloud customer base.

For the current fiscal year, ending in December 2025, analysts expect GOOG's EPS to grow 25.9% year-over-year to $10.12. The company's earnings surprise history is strong. It beat the consensus estimates in the last four quarters.

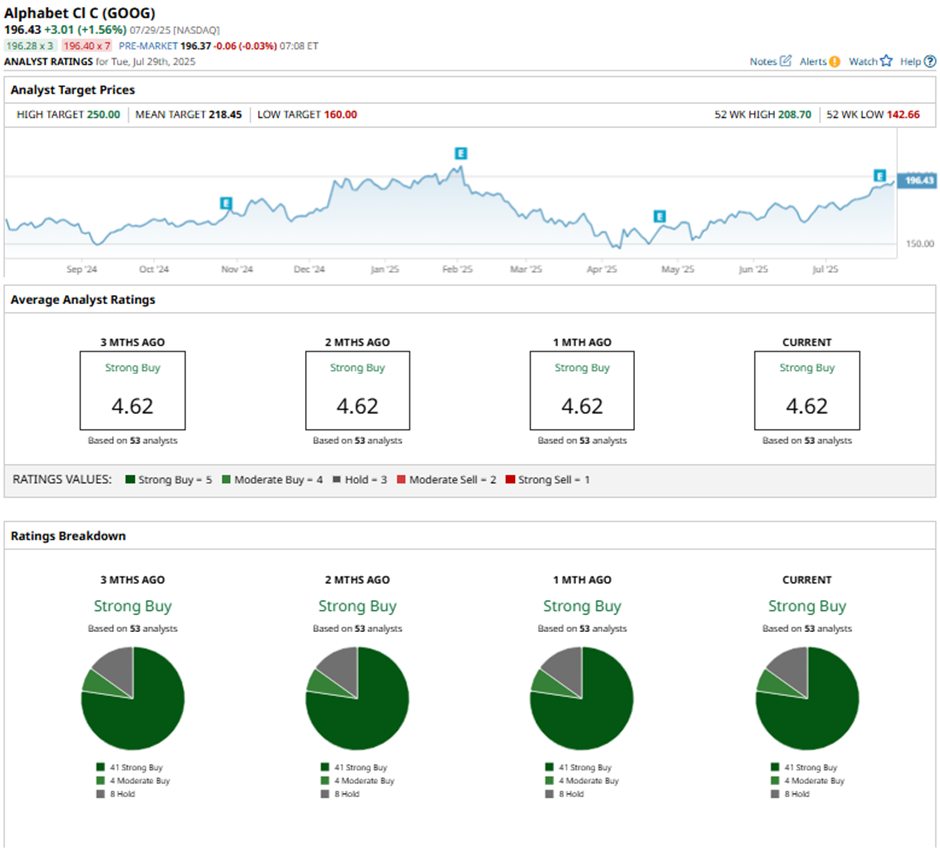

Among the 53 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 41 “Strong Buy” ratings, four “Moderate Buys,” and eight “Holds.”

On Jul. 29, Wells Fargo raised Alphabet’s price target to $187, maintaining an “Equal Weight” rating. The firm expects Google Cloud to benefit from OpenAI and Anthropic workloads in 2026, with recent Q2 strength driven by core performance despite early 2025 headwinds.

As of writing, the stock is trading below the mean price target of $218.45. The Street-high price target of $250 implies a potential upside of 27.3% from the current price levels.