/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Boise, Idaho-based Micron Technology, Inc. (MU) designs, develops, manufactures, and sells memory and storage products. Valued at $568.7 billion by market cap, the company manufactures and markets dynamic random access memory chips, static random access memory chips (SRAMs), flash memory, semiconductor components, and memory modules.

Shares of this chip giant have significantly outperformed the broader market over the past year. MU has gained 541.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29.1%. In 2026, MU’s stock rose 76.7%, surpassing the SPX’s 4.3% rise on a YTD basis.

Zooming in further, MU’s outperformance is also apparent compared to the iShares Semiconductor ETF (SOXX). The exchange-traded fund has gained about 137.8% over the past year. Moreover, MU’s gains on a YTD basis outshine the ETF’s 45.7% returns over the same time frame.

Micron’s massive outperformance is driven by an AI-fueled memory shortage and its lead in high-bandwidth memory. HBM is the key growth engine with volume HBM4 shipments underway, while HBM3E shifted mix to high-margin AI assets. Data center demand is strong across server DRAM, enterprise SSDs, and HBM, doubling Cloud Memory revenue. With UBS citing 95% Q1 memory price jumps and a shift to long-term supply deals, Micron is positioned as a core AI infrastructure play with durable pricing power into 2027.

For the current fiscal year, ending in August, analysts expect MU’s EPS to grow 651.6% to $57.72 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

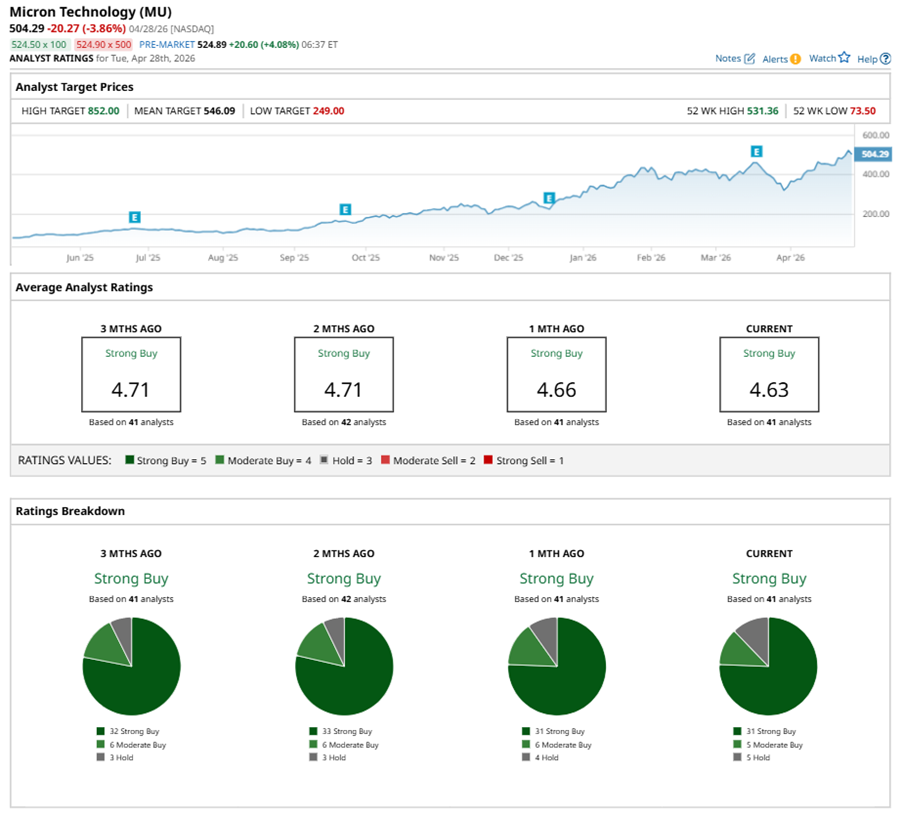

Among the 41 analysts covering MU stock, the consensus is a “Strong Buy.” That’s based on 31 “Strong Buy” ratings, five “Moderate Buys,” and five “Holds.”

This configuration is less bullish than a month ago, with six analysts advising a “Moderate Buy.”

On Apr. 26, Krish Sankar from TD Cowen maintained a “Buy” rating on MU with a price target of $660, implying a potential upside of 30.9% from current levels.

The mean price target of $546.09 represents an 8.3% premium to MU’s current price levels. The Street-high price target of $852 suggests an ambitious upside potential of 69%.