/Akamai%20Technologies%20Inc%20logo%20on%20building-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Akamai Technologies, Inc. (AKAM) is a cloud computing and cybersecurity company best known for its global content delivery network (CDN), edge computing infrastructure, and internet security solutions. Founded in 1998 and headquartered in Cambridge, Massachusetts, the company serves enterprises worldwide with services spanning cloud infrastructure, API security, DDoS protection, and AI-ready edge computing platforms. The company currently has a market cap of $21 billion.

Shares of the cloud services provider have outperformed the broader market over the past 52 weeks. AKAM stock has surged 84.7% over this time frame, while the broader S&P 500 Index ($SPX) has gained 23.2%. Moreover, shares of Akamai Technologies have gained 64.9% on a YTD basis, compared to SPX’s 7.3% rise.

Looking closer, the stock has also outpaced the Technology Select Sector SPDR Fund’s (XLK) 46.7% return over the past 52 weeks and 19.5% gain in 2026.

Akamai Technologies reported its first-quarter 2026 financial results on May 7. The company posted first-quarter revenue of $1.1 billion, up 6% year-over-year (YOY). The strongest performance came from Cloud Infrastructure Services (CIS), where revenue surged 40% YOY to $95 million, highlighting Akamai’s growing positioning in AI and cloud computing infrastructure.

Security revenue climbed 11% YOY to $590 million, continuing to be the company’s largest and most profitable segment. Meanwhile, delivery and other cloud applications revenue declined 7% YOY to $389 million.

Profitability metrics were mixed as Akamai increased investments in GPU infrastructure and AI cloud capacity. Non-GAAP operating income declined 8% YOY to $283 million, while non-GAAP operating margin compressed to 26% from 30% in Q1 2025. Non-GAAP EPS came in at $1.61, down 5% YOY. Adjusted EBITDA declined 3% YOY to $427 million.

On May 8, the stock exploded 26.6% intraday following the announcement and stable cloud momentum.

Analysts forecast EPS of $4.14 for fiscal 2026, a 6.1% decline, followed by a 11.6% rise to $4.62 in 2027. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters and missed on one occasion.

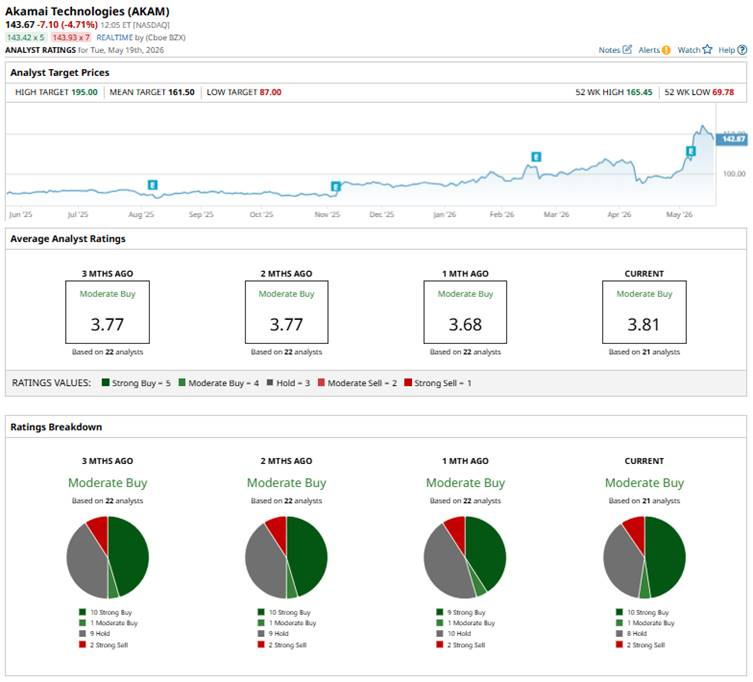

Among the 21 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buys,” one “Moderate Buy” rating, eight “Holds,” and two “Strong Sells.”

This configuration is slightly more bullish than one month ago, when there were nine “Strong Buy” ratings.

Recently, Morgan Stanley raised its price target on Akamai to $165 from $120 while maintaining an “Overweight” rating, citing accelerating momentum toward double-digit growth.

Its mean price target of $161.50 indicates a premium of 7.1% from the current market prices. The Street-high price target of $195 implies a potential upside of 29.3% from the current price levels.