The recent agitations by the governments of Kerala and Karnataka, and the support extended by several State governments, have highlighted many disquieting issues in the practice of fiscal federalism in India. These agitations show that the newly constituted 16th Finance Commission (FC) would have to proceed seriously and innovatively to justly address complaints of increasing vertical and horizontal inequalities in devolution.

Within the domain of vertical devolution — that is the sharing of resources between the Union and States — there are two disturbing trends that need urgent redressal. First, the Union government has sought to keep an increasing share of its proceeds out of the divisible pool so that they need not be shared with States. Secondly, it has also not been devolving the shares of net proceeds to the States as mandated by successive FCs.

The shrinking divisible pool

The net divisible pool, or net proceeds, is that part of the gross tax revenue from which a share would have to be vertically devolved by the Union to all States. Such shares are assigned by each FC for a five-year period. Earlier, all corporation taxes and customs duties were fully absorbed by the Union, and only income taxes and excise duties were shared with the States. However, with changes over the years, culminating in a constitutional amendment in 2000, all taxes of the Union were added to the net proceeds. But there was a catch — cesses and surcharges under Article 270 and Article 271 were kept out of the net proceeds. In the past, such exclusion of cesses and surcharges were based on specific FC recommendations. But the amendment in 2000 provided a constitutional basis for it. Presently, the net proceeds consists of the gross tax revenue after the deduction of cesses, surcharges and the cost of collection of taxes.

Over the past decade or more, several cesses and surcharges were introduced by the Union government. When the Goods and Services Tax (GST) was initiated in 2017, the expectation was that many cesses and surcharges would be discarded and subsumed into the GST system. On the contrary, new cesses and surcharges continued to be introduced, and many old cesses and surcharges remained outside the GST system. For instance, the Agriculture Infrastructure and Development Cess was introduced as recent as in 2021-22. Similarly, when the Health and Education Cess was introduced in 2017-18, it just replaced the Primary Education and Secondary Education cess on direct taxes. The expansion of cesses and surcharges have led to the exclusion of an increasing share of the gross tax revenue from net proceeds. Interestingly, there is conflicting information released by the government on the quantum of cesses and surcharges. In December 2022, responding to a question raised in the Rajya Sabha, the government stated that the share of cesses and surcharges in the gross tax revenue was 18.2% in 2019-20, 25.1% in 2020-21 and 28.1% in 2021-22. But responding to another question in the Lok Sabha in March 2023, the government stated that the corresponding shares were 15.6% in 2019-20, 20.5% in 2020-21 and 18.4% in 2021-22.

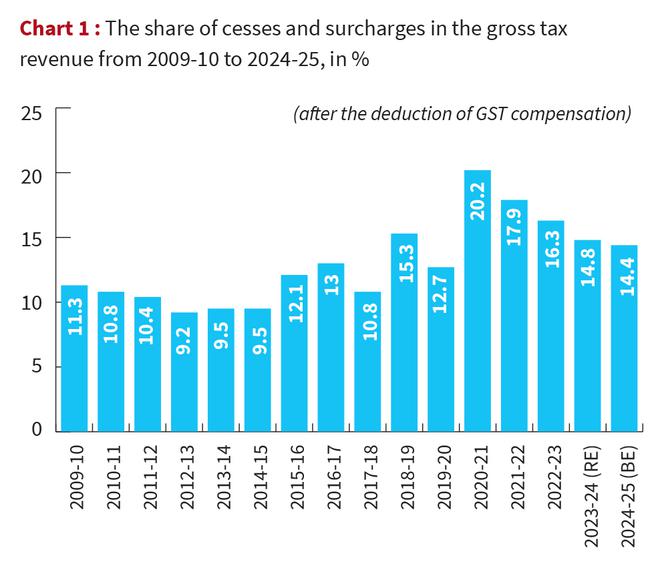

To obtain more accurate estimates of cesses and surcharges, this article uses disaggregated data from budget documents between 2009-10 and 2024-25. The collection of each type of cess and surcharge was separately recorded and added up, after giving due consideration to their occasional abolishment and/or merger with other taxes. The total collection of cesses and surcharges rose from ₹70,559 crore in 2009-10 to ₹6.6 lakh crore in 2023-24 (RE) and ₹7 lakh crore in 2024-25 (BE). These collections include the GST compensation cess, which is given to the States as per statutory requirements. If we deduct the GST compensation cess, the collection of cesses and surcharges rose from ₹70,559 crore in 2009-10 to ₹5.1 lakh crore in 2023-24 (RE) and ₹5.5 lakh crore in 2024-25 (BE). Considered as a share of the gross tax revenue, cesses and surcharges fell from 11.3% in 2009-10 to 9.5% in 2014-15, but then rose to 15.3% in 2018-19, a peak of 20.2% in 2020-21 and 16.3% in 2022-23. As per the tentative figures for 2023-24, cesses and surcharges are estimated at 14.8% of the gross tax revenue, which is still higher than the corresponding shares in 2009-10 or 2014-15 (see Chart 1).

Between 2009-10 and 2023-24, a cumulative total of ₹36.6 lakh crore was collected by the Union government as cesses and surcharges. An additional ₹5.5 lakh crore is projected to be collected as cesses and surcharges in 2024-25. This amount was not shared with States and was used solely by the Union government.

Rise in tied transfers

The Union government may argue that a part of this amount was used to finance centrally sponsored schemes and central sector schemes, while another part was used to provide non-plan grants or capital transfers to States. The problem, however, is that such transfers are not untied as is the case with the devolution of State’s share in central taxes. In centrally sponsored schemes, about 40% of the cost must be borne by the State governments. Even in central sector schemes, the contribution of the Union government is often meagre, and the State governments are forced to contribute significantly larger amounts to run the schemes meaningfully.

Even when State governments contribute a lion’s share in implementing a central project, the Union government often tries to usurp credit by insisting on displaying the Prime Minister’s photograph or other forms of labelling. Recent disputes over labelling in the Ayushman Bharat wellness centres is one such example. Similarly, several grants given to the States are contingent on fulfilment of conditionalities — and some of these conditionalities include the insistence on labelling. Finally, most capital transfers given to the States are loans, which must be repaid to the Union government

The bottom line is that none of the transfers to the States outside the FC recommendations are either unconditional or suitable to meet their context-specific needs. Instead, they tend to reaffirm a centralising tendency in the fiscal realm — one that effectively tends to push the Union-State relationship into a patron-client relationship. Any purported deviation from the guidelines or a failure to meet the imposed conditionalities can lead to the denial of such resources.

The share of States in central taxes is, thus, a gold standard in any assessment of fiscal federalism. It is a matter of deep worry, then, that the Union government increasingly pays less of untied transfers to States and retains more of the gross tax revenue as cesses and surcharges. The substitution of such untied transfers with central schemes does not ameliorate the loss; instead, it inserts rigidities in Union-State relations and ends up diluting the spirit of cooperative fiscal federalism.

The CAG indictments

Cesses and surcharges have also been subjected to critical scrutiny by the Comptroller and Auditor General (CAG). All cesses must be transferred to a reserve fund in the Public Account of India after their collection. In its reports the CAG has uncovered numerous instances of either non-transfer or short transfer of the collected amounts to the respective funds. A CAG report in 2023 noted that if ₹52,732 crore was collected towards the Health and Education Cess in 2021-22, only ₹31,788 crore (or 60%) was transferred to the reserve fund of Prarambhik Shikha Kosh. The Research and Development Cess must be transferred to the Fund for Technology Development and Application. A CAG report in 2019 noted that the total collection of Research and Development Cess between 1996-97 and 2017-18 was ₹8,077 crore, but only ₹779 crore (or 9.6%) was transferred to the Fund.

The Swatchh Bharat Cess must be transferred to the Rashtriya Swachhata Kosh. The extent of short transfer to the Kosh between 2015–16 and 2017–18 was ₹4,891 crore. The extent of short transfer between 2010–11 and 2017–18 under the Road Cess was ₹72,726 crore and under the Clean Energy Cess was ₹44,505 crore.

Non-transfers and short transfers of cesses defeat the logic of their collection. It also reaffirms the view that cesses and surcharges are just a ruse to divert increasing quantum of funds away from the divisible pool to meet other financial requirements of the Union government.

Deviations from FC recommendations

Speaking in Parliament on February 8, 2024, the Union Finance Minister claimed: “whatever the Finance Commission has recommended [as the rate of devolution], I follow it to the last word”. How robust is this claim?

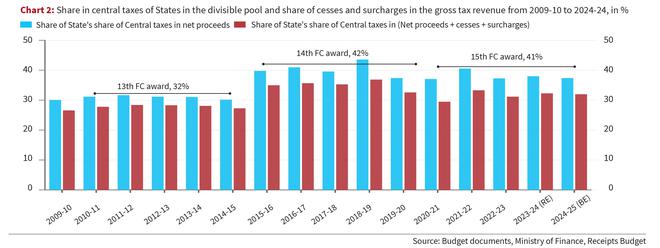

We have seen that a significant portion of the gross tax revenue is retained by the Union government as cesses and surcharges. One may disagree with such a retention, but it has some basis in constitutional provisions. However, what has happened to the recommendation of the FCs that a certain share of the net proceeds must be shared with all States? These shares were stipulated as 32% by the 13th FC (2010 to 2015), 42% by the 14th FC (2015 to 2020), and 41% by the 15th FC (2020 to 2025).

Annual estimates of net proceeds can be obtained by deducting cesses, surcharges, and costs of collection of taxes from the gross tax revenue. These estimates of net proceeds can be compared against the “States’ share of central taxes” in each year to check if they amounted to the FC-stipulated percentage of the net proceeds. It turns out that the Union government has not been sharing even the FC-recommended shares of net proceeds with the States. The States’ share of central taxes as a percentage of net proceeds was below the recommendations of the respective FCs for most years (see Chart 2).

The average of the annual shares of devolution was 31.1% during the 13th FC period, 40.3% during the 14th FC period and 38.1% during the 15th FC period. The shortfall was widest during the ongoing period of the 15th FC, for which the claim of “to the last word” has been offered.

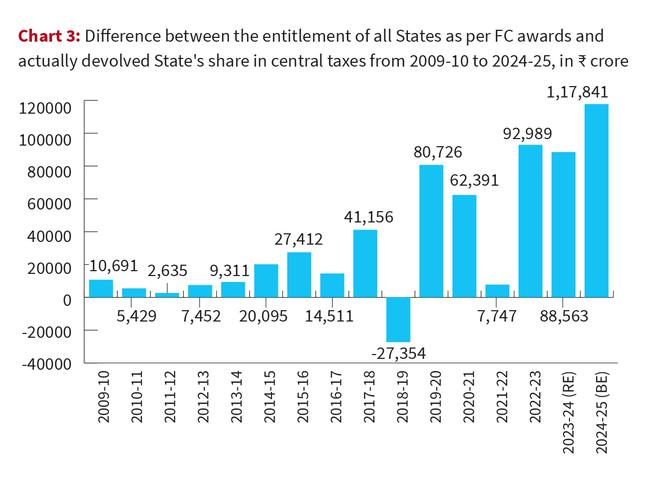

If we add cesses and surcharges to the net proceeds — to create a revised divisible pool — the share of devolution would fall even further to 28% during the 13th FC period, 35.1% during the 14th FC period and 31.7% during the 15th FC period. What do these shortfalls vis-a-vis FC recommendations amount to in quantum terms? Between 2009-10 and 2024-25 (BE), the cumulative amount not devolved to the States was ₹5.61 lakh crore (see Chart 3).

The total amounts not devolved to the States were ₹44,922 crore during the 13th FC period, ₹1.36 lakh crore during the 14th FC period and a whopping ₹3.69 lakh crore during the 15th FC period (including 2024-25 BE). The failure to devolve these funds to States must be treated as a striking constitutional impropriety.

The agenda of reform

To conclude, sharing of resources from the divisible pool, and the extent of cesses and surcharges, must be matters of critical importance for the 16th FC. The FC must take initiative to correct historical wrongs in vertical devolution through compensations to the States. It must instruct the Union government to publish accurate estimates of “net proceeds” in the budget documents. It must also arrange to provide shortfalls in devolution over the last decade as a lump sum untied grant to States. On its part, the Union government must legislatively act to have strict limits on the collection of cesses and surcharges; cesses and surcharges should automatically expire after a short period and must not be rechristened under another name. Apart from addressing rightful complaints on the inequalities in horizontal devolution, the stance of the 16th FC on vertical devolution would be critical to the survival of fiscal federalism in India.

R. Ramakumar teaches at the School of Development Studies, TISS, Mumbai.