/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Financial services major Morgan Stanley has been convinced to remove memory leader Micron (MU) as its top pick and replace it with Nvidia (NVDA). Raising doubts over the sustainability of the current strong demand, John Moore, an analyst at the firm, said, “There is a commonly voiced view that memory stocks are pricing in a much longer and more durable cycle than processor stocks; we actually somewhat disagree with that. Our memory conversations with clients are very similar to NVIDIA conversations - a clear recognition that conditions are exceptional in both right now, But [sic] a very strong peak year at current valuations has been viewed as more investable for memory, because upward revisions are more dynamic. There is not much conviction about 2027 for either stock.”

It should be noted that though Nvidia has been preferred as the top pick, it has not been with much enthusiasm. As for the demand for memory, it remains as hot as ever. Though it may go through its own cycles, the overall picture remains unchanged: AI will grow rapidly, data center demand will grow rapidly, and consequently, the demand for memory will also grow rapidly.

About Micron

Founded in 1978, Micron (MU) designs and manufactures memory and storage semiconductors, primarily DRAM (dynamic random access memory), HBM (high bandwidth memory), and NAND flash memory. While DRAM is used in servers, PCs, smartphones, and AI infrastructure, NAND is used for SSDs, mobile storage, and enterprise storage systems, and HBM is a specialized memory used in AI accelerators and GPUs.

These technologies are critical for computing performance because they determine how quickly data can be accessed and processed. Micron sells its products to hyperscale cloud providers, device manufacturers, automotive companies, and semiconductor firms that integrate memory into computing systems.

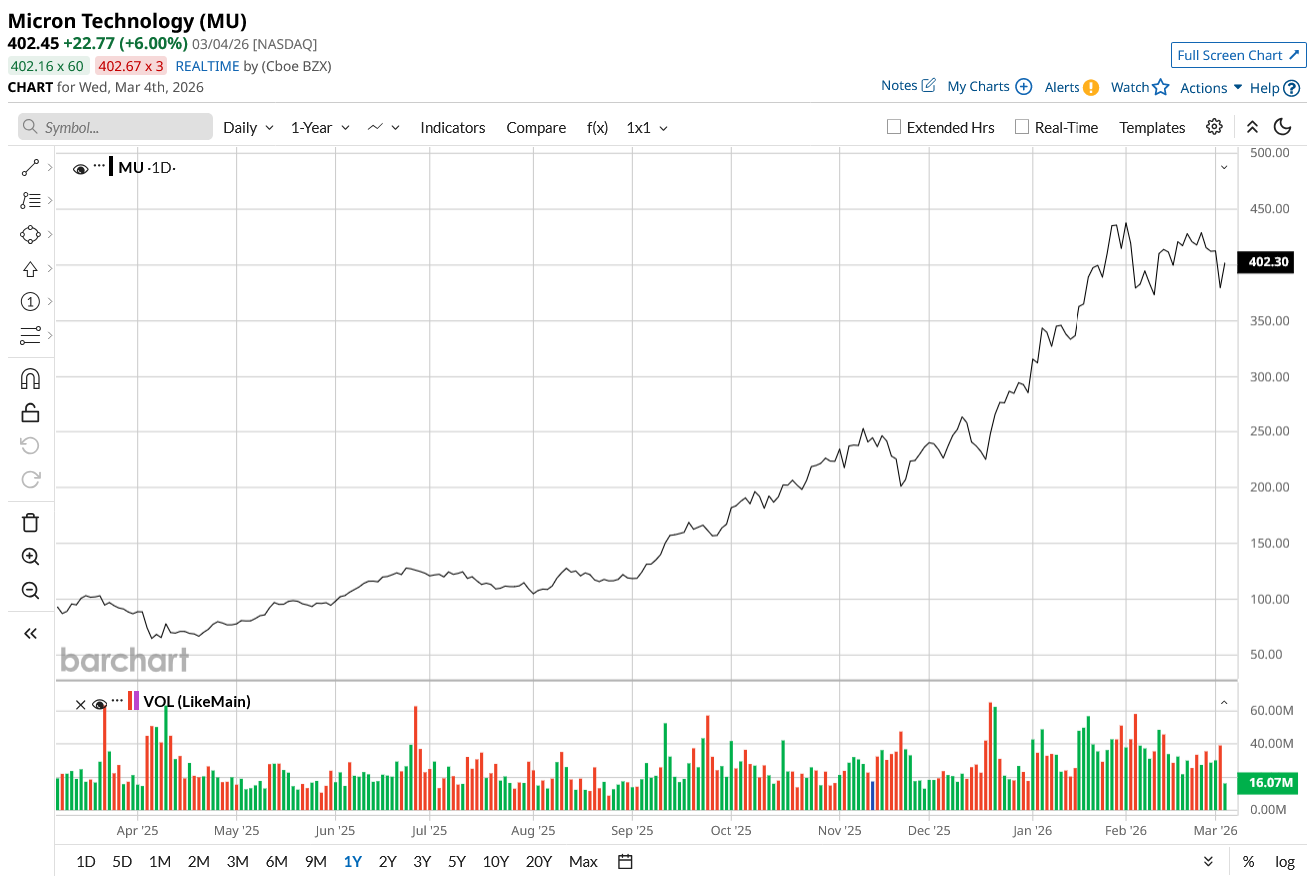

Valued at a market cap of $464.5 billion, the MU stock has been on a tear over the past year, jumping by 338% over the past year.

So, should investors who are believers in the AI trade remain bullish about Micron? Short answer: Yes, and here's why.

Great Financials and Only Getting Better

Micron may have captured the imagination of the market in recent times. However, it has been steadily growing its operations at a healthy rate for years now. Over the past 10 years, revenue and earnings have displayed CAGRs of 10.95% and 18.93%, respectively. Moreover, earnings have been reporting beats for each of the past nine quarters straight.

Notably, the results for the latest quarter were a blowout as well, with both revenue and earnings surpassing estimates. Revenues jumped by 56.6% from the previous year to $13.64 billion, coming in higher than the consensus estimate by $760.74 million. All the revenue segments witnessed growth, led by the cloud memory and the mobile businesses. While the cloud memory unit reported revenues of $5.3 billion in fiscal Q1 2026, the mobile business had revenues of $4.3 billion in the same period, implying growth rates of 103.8% and 65.4% on a year-over-year (YoY) basis, respectively. However, growth for the data center business was disappointing, with an annual growth rate of just 4.3% to $2.4 billion.

Earnings growth did not disappoint, however, growing at a rapid pace of 167% from the prior year to $4.78 per share, much ahead of the consensus estimate of $3.96 per share. Further, this was the eighth consecutive quarter in which Micron has reported a doubling of earnings yearly.

Meanwhile, cash flow activities also remained robust. Net cash from operating activities for the quarter came in at $8.4 billion compared to just $3.2 billion in the year-ago period. Overall, Micron closed the quarter with a cash balance of $9.7 billion, much higher than its short-term debt levels of just $569 million.

For fiscal Q2 2026, Micron expects revenue to be between $18.3 billion and $19.1 billion, while EPS forecasts are for $8.22 to $8.62. While the midpoint for revenues will represent a growth of 132.3% from the previous year, the midpoint for EPS would result in an even sharper growth rate of 440%.

Micron's valuations are also not out of whack. While in terms of forward P/E and P/CF, its metrics at 12.10 and 9.75 are lower than the sector medians of 21.97 and 16.90, respectively, its forward P/S of 6.08 is not much higher than the sector median of 3.10. Notably, forward revenue and EPS growth rates of 57.47% and 298.22% are much higher than the sector medians of 10.21% and 14.85%, respectively.

Micron: The Memory Stalwart

The global memory chip market is a large one already and is projected to grow to an even bigger size. At about $300 billion currently, it is expected that the memory market will reach $846.81 billion by 2033. And with about 25% market share, Micron is certainly going to have a decisive say in this burgeoning market.

Micron has carved out a focused strategy centered on leadership in memory and data storage technologies, which positions it as a vital supplier to the rapidly expanding AI ecosystem. The company maintains a comprehensive presence across the memory spectrum, supplying solutions for everything from consumer mobile devices to high-performance data center computing. Its primary emphasis, however, is on serving data center operators with cutting-edge HBM products, particularly HBM3E and the forthcoming HBM4. Micron's HBM3E variant stands out for consuming approximately 30% less power than competing offerings, a meaningful advantage for data center operators focused on energy efficiency and operating costs.

The company has also gained a clear technical lead in NAND flash through early mass production of 232-layer and 276-layer technologies utilizing a CMOS-under-Array (CuA) architecture. This design enables a more vertically integrated structure and significantly smaller die sizes than peers, resulting in the industry's highest areal density (exceeding 14.6 Gb/mm²). For enterprise SSDs critical to AI training workloads, this translates into higher-capacity drives (64TB and 128TB) that deliver superior quality of service and lower latency compared with Samsung's V-NAND alternatives. Thus, by prioritizing bit efficiency over sheer bit volume, Micron is capturing higher-margin specialty segments where performance specifications, rather than price alone, determine design wins.

On the capital front, Micron is pursuing aggressive expansion, with a particular focus on U.S.-based manufacturing amid ongoing geopolitical uncertainties. Management has outlined plans for a major new facility in New York State, alongside substantial investments totaling approximately $200 billion across two Idaho plants, four New York plants, and a significant upgrade to its largest Virginia facility ($150 billion allocated to production capacity and $50 billion to R&D). The objective is to secure roughly 40% of U.S. memory demand. As part of this strategy, ground was broken on January 16, 2026, for a large-scale memory manufacturing complex in New York, with total construction costs estimated at $100 billion and completion targeted for 2030. This will represent the largest semiconductor facility in the United States upon completion.

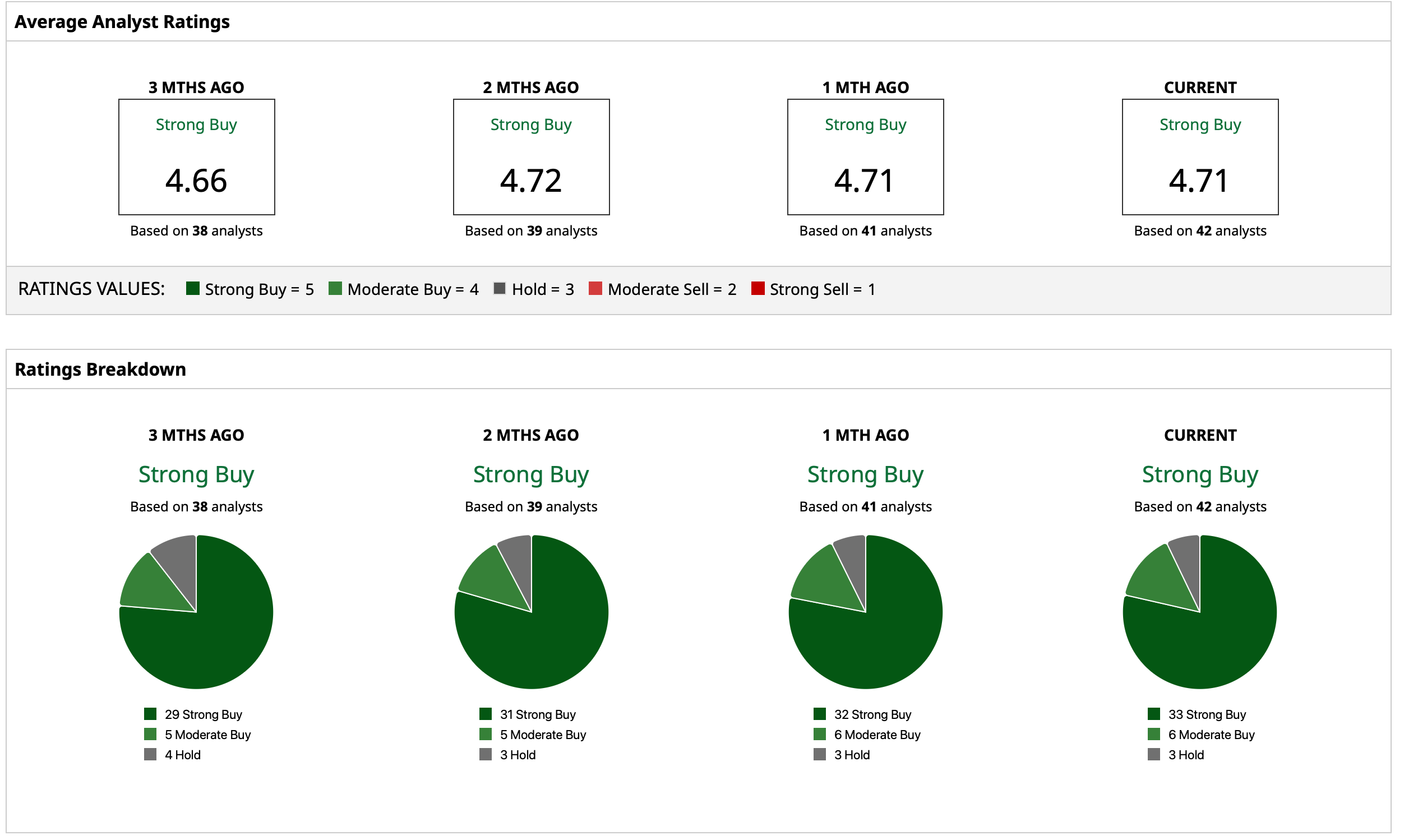

Analyst Opinion

Thus, analysts have deemed the MU stock to be a “Strong Buy,” with a mean target price that has already been surpassed. The high target price of $500 denotes an upside potential of about 25% from current levels. Out of 42 analysts covering the stock, 33 have a “Strong Buy” rating, six have a “Moderate Buy” rating, and three have a “Hold” rating.