/Applied%20Materials%20Inc_%20campus%20sign-by%20Sundry%20Photography%20via%20iStock.jpg)

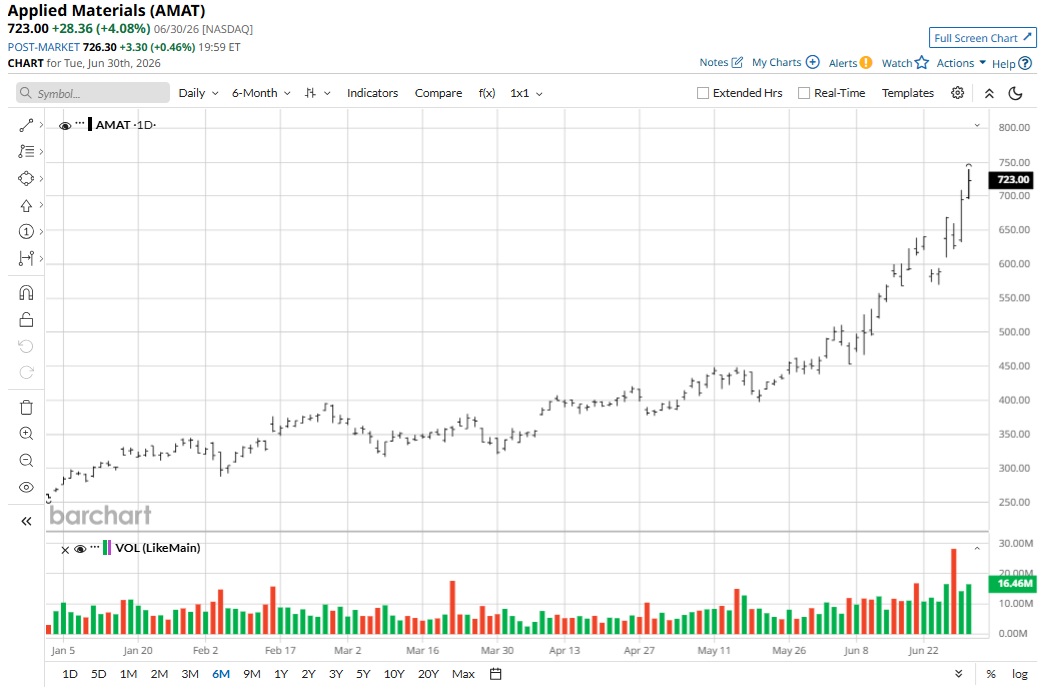

Applied Materials (AMAT) stock has delivered stellar returns of 211% in the last 52 weeks. This rally has been supported by structural tailwinds for the semiconductor industry that will likely benefit the company’s semiconductor segment growth.

To put things into perspective, Deloitte believes that the global semiconductor industry will reach $975 billion in sales this year. Further, semiconductor annual sales are expected to swell to $2 trillion by 2036.

Considering this total addressable market, Applied Materials has ample headroom for growth and cash flow upside. Accordingly, it’s unsurprising that analysts continue to remain bullish on AMAT stock even after a big rally.

Susquehanna recently increased its price target for Applied Materials from $575 to $900 per share. This view is backed by an upgraded forecast for wafer fab equipment spending. Further, with customers “paying premiums” to leading suppliers in order to secure allocations, it’s likely that higher average selling price will boost EBITDA margin and cash flows.

About Applied Materials Stock

Headquartered in Santa Clara, California, Applied Materials is a provider of materials engineering solutions used to produce semiconductors globally. The company operates through two main segments: Semiconductor Systems and Applied Global Services. The Semiconductor Systems segment designs, develops, manufactures, and sells a wide range of equipment used to fabricate semiconductor chips, while the Applied Global Services segment provides services and factory automation software to customer fabrication plants.

For the first half of fiscal 2026, Applied Materials reported revenue of $14.9 billion. For the same period, the company delivered operating cash flow and free cash flow of $2.5 billion and $1.3 billion, respectively.

With steady growth, robust margins, and structural tailwinds for the semiconductor industry, AMAT stock has surged 122% in the last six months.

Positive Business Catalysts

In the second quarter of fiscal 2026, Applied Materials delivered a gross margin of 50%, which was its highest gross margin in more than 25 years. Considering the strong industry demand, it’s likely that gross margin expansion will sustain.

At the same time, the company has indicated that its semiconductor equipment business is expected to grow by more than 30% for the calendar year. Additionally, with an “unprecedented demand environment,” Applied Materials is planning for impending demand in 2027 and beyond. Applied Materials has already doubled its manufacturing capacity to support growing demand, so the upcoming quarters should continue to surprise.

On the innovation front, Applied Materials is working with Taiwan Semiconductor (TSM) to “accelerate the development and commercialization of semiconductor technologies required for the next era of AI.” Similarly, the firm is working with SK Hynix for the development and deployment of next-generation DRAM and high-bandwidth memory (HBM). Meanwhile, its partnership with Micron (MU) focuses on the development of DRAM, HBM, and NAND solutions targeting energy efficiency in AI systems.

Industry tailwinds, capacity expansion, and a focus on innovation will likely ensure that Applied Materials remains in a high-growth trajectory.

What Do Analysts Say About AMAT Stock?

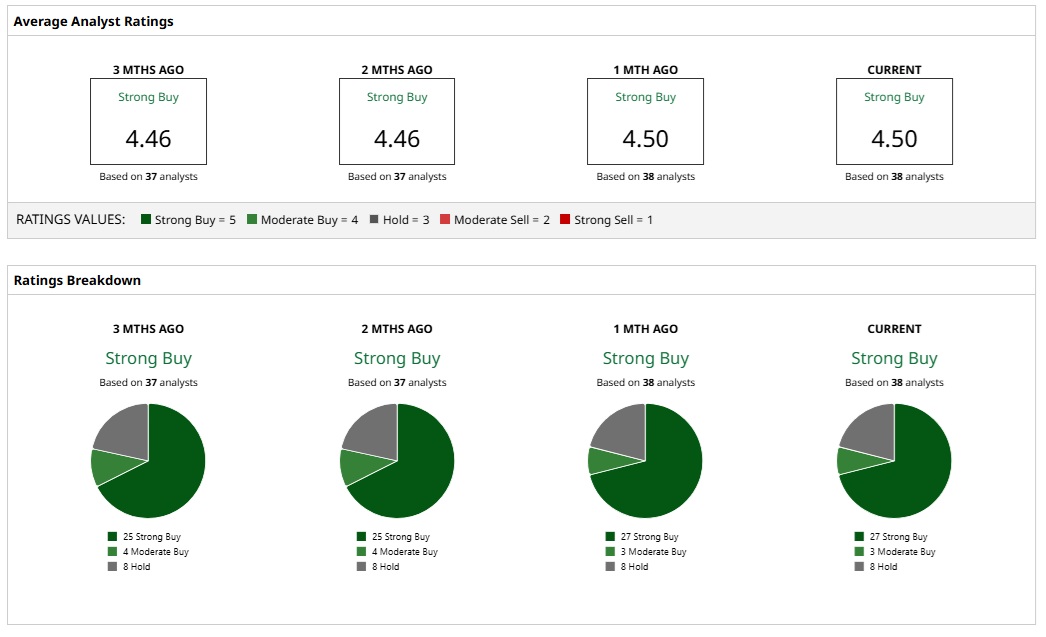

Based on 38 analysts with coverage, AMAT stock has a consensus “Strong Buy” rating. While 27 analysts have a “Strong Buy” rating for AMAT stock, three have a “Moderate Buy,” and eight have a “Hold” rating.

The mean price target of $594.21 represents limited potential upside from current levels. However, the most bullish price target of $900 suggests that AMAT stock could climb as much as 52% from here.

Conclusion

From a financial perspective, Applied Materials ended Q2 with total cash and investments of $13.4 billion. Further, as growth accelerates and margins expand, free cash flows should swell. Even with $6.5 billion in total debt, the company has strong credit metrics and high financial flexibility for investments. At the same time, dividend growth will likely be coupled with aggressive share repurchases.

Even after a big rally in the last 52 weeks, AMAT stock is poised to remain in an uptrend.