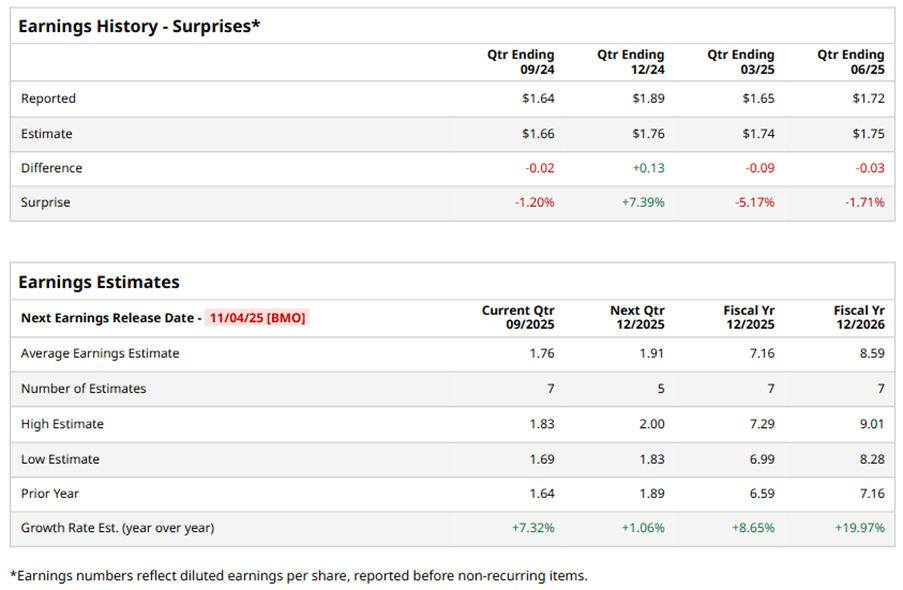

New York-based Apollo Global Management, Inc. (APO) is a private equity firm specializing in investments in credit, private equity, infrastructure, secondaries and real estate markets. Valued at $69.1 billion by market cap, the company focuses on investing in yield, hybrid, and equity markets to generate retirement and investment incomes. The private equity giant is expected to announce its fiscal third-quarter earnings for 2025 before the market opens on Tuesday, Nov. 4.

Ahead of the event, analysts expect APO to report a profit of $1.76 per share on a diluted basis, up 7.3% from $1.64 per share in the year-ago quarter. The company missed the consensus estimates in three of the last four quarters while beating the forecast on another occasion.

For the full year, analysts expect APO to report EPS of $7.16, up 8.7% from $6.59 in fiscal 2024. Its EPS is expected to rise 20% year over year to $8.59 in fiscal 2026.

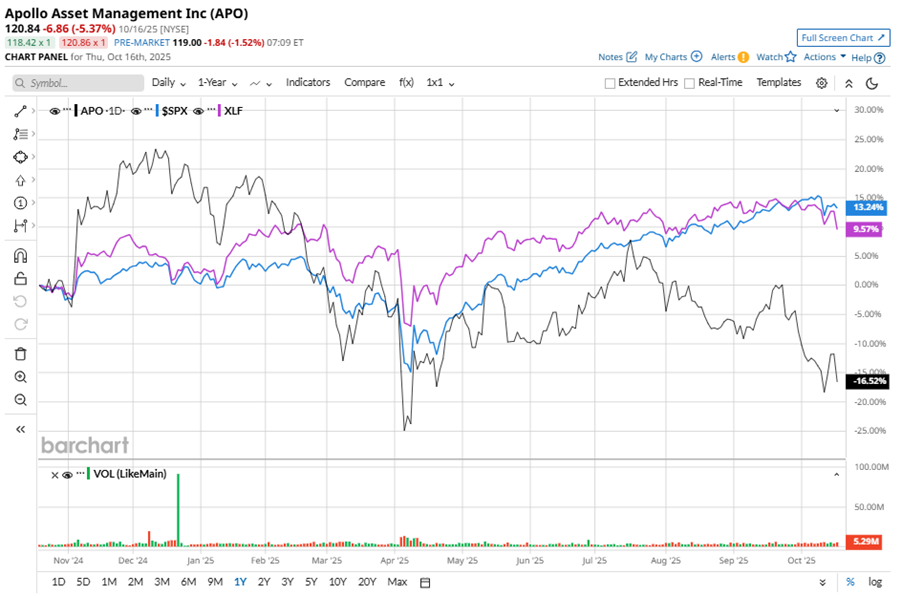

APO stock has considerably underperformed the S&P 500 Index’s ($SPX) 13.5% gains over the past 52 weeks, with shares down 15.4% during this period. Similarly, it notably underperformed the Financial Select Sector SPDR Fund’s (XLF) 9% gains over the same time frame.

APO’s weak performance is driven by rising expenses, acting as a headwind.

On Aug. 5, APO shares closed up by 2.5% after reporting its Q2 results. Its adjusted EPS of $1.92 surpassed the consensus estimate of $1.85. The total revenues stood at $6.8 billion, up 13.2% year over year.

Analysts’ consensus opinion on APO stock is bullish, with a “Strong Buy” rating overall. Out of 22 analysts covering the stock, 15 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and six give a “Hold.” APO’s average analyst price target is $158.74, indicating an ambitious potential upside of 31.4% from the current levels.