/Aon%20plc_%20on%20laptop-by%20monticello%20via%20Shutterstock.jpg)

Dublin, Ireland-based Aon plc (AON) operates as a professional services firm with clients in over 120 countries across the globe. With a market cap of $78.9 billion, Aon’s offerings include risk management services, insurance and reinsurance brokerage, human resource consulting, and outsourcing services.

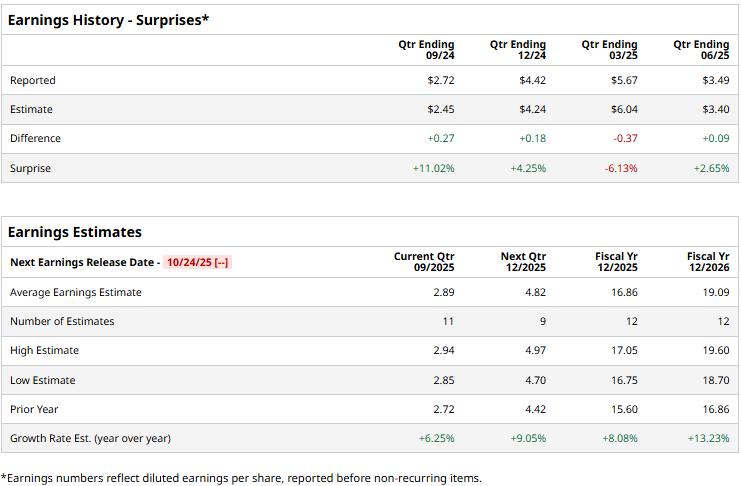

The financial sector giant is expected to announce its third-quarter results before the end of October. Ahead of the event, analysts expect Aon to deliver a non-GAAP profit of $2.89 per share, up 6.3% from $2.27 per share reported in the year-ago quarter. While the company has missed Street’s bottom-line estimates once over the past four quarters, it has surpassed the projections on three other occasions.

For the full fiscal 2025, Aon’s non-GAAP EPS is expected to come in at $16.86, up 8.1% from $15.60 in 2024. While in fiscal 2026, its earnings are expected to further surge 13.2% year-over-year to $19.09 per share.

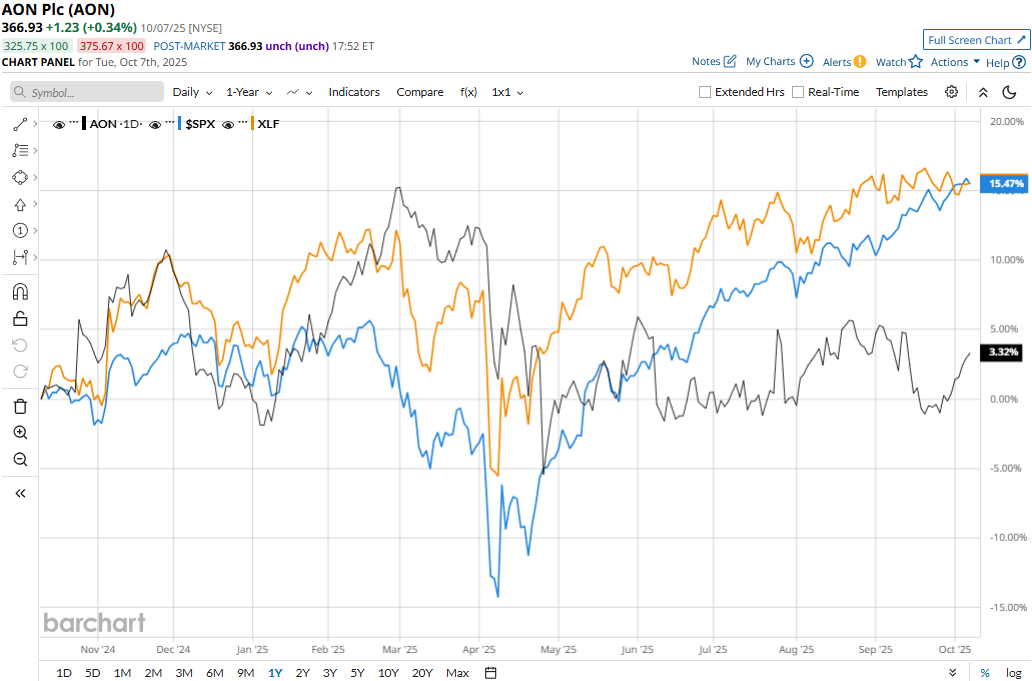

Aon’s stock prices have gained 6.7% over the past 52 weeks, notably lagging behind the Financial Select Sector SPDR Fund’s (XLF) 19.3% surge and the S&P 500 Index’s ($SPX) 17.9% gains during the same time frame.

Aon’s stock prices surged 4.6% in the trading session following the release of its impressive Q2 results on Jul. 25. The increasingly complex business environment and the need for newer sources of capital have notably increased the demand for Aon’s services. During the quarter, the company registered a 6% growth in organic revenues and a solid 10.5% year-over-year surge in overall topline to $4.2 billion, beating the Street’s expectations.

Further, the company also observed a notable expansion in its operating margins, leading to a 13.8% growth in non-GAAP operating income to $1.2 billion. Alongside, Aon’s non-GAAP EPS soared 19.1% year-over-year to $3.49, surpassing the consensus estimates by 2.7%.

Analysts remain optimistic about the stock’s prospects. Aon maintains a consensus “Moderate Buy” rating overall. Of the 23 analysts covering the stock, opinions include 12 “Strong Buys,” one “Moderate Buy,” seven “Holds,” one “Moderate Sell,” and two “Strong Sells.” Its mean price target of $415.06 suggests a 13.1% upside potential from current price levels.