AMD (AMD) stock has been one of the top performers in 2026. Shares have surged more than 130% year-to-date (YTD), significantly outperforming rival Nvidia (NVDA), whose stock has gained about 13% over the same period.

The rally reflects growing investor confidence in AMD's position within the artificial intelligence (AI) ecosystem. Demand for the company's Instinct GPUs continues to accelerate as enterprises and cloud providers ramp up spending on AI infrastructure.

Importantly, the AI opportunity extends beyond accelerators. High-performance CPUs are also seeing robust demand as AI workloads evolve from model training to inference and emerging Agentic AI applications. These increasingly complex workloads require greater computing power, creating a powerful tailwind for both AMD's GPU and CPU businesses.

However, AMD's sharp run-up has pushed its valuation well above Nvidia's. AMD currently trades at a forward price-to-earnings (P/E) ratio of about 84.4, compared with Nvidia's forward P/E multiple of 25.4.

At first glance, that premium appears difficult to justify. However, AMD's potential to deliver strong earnings, growing share in the AI market, and large CPU opportunity justify its high valuation. Meanwhile, AI infrastructure spending remains elevated, suggesting that both AMD and Nvidia are likely to deliver strong growth in the years ahead. In addition, strong bottom-line growth continues to support the bull case for both of these stocks.

Why AMD Could Be One of the Biggest AI Winners Through 2027

Despite trading at a premium to Nvidia, AMD stock still looks compelling, as it appears well-positioned to benefit from the ongoing AI boom, with strong growth prospects extending through 2027 and beyond. AMD’s expanding share in data centers and high-performance computing continues to strengthen its long-term investment case.

The company delivered an impressive first quarter, with revenue rising 38% year-over-year (YoY) to $10.3 billion. Earnings grew more than 40%, while free cash flow more than tripled, reflecting both strong demand and improving profitability.

Much of its growth is driven by the company’s data center business, where revenue surged 57% to $5.8 billion. Demand for its EPYC server processors and Instinct AI accelerators remains robust as enterprises and hyperscale cloud providers increase spending on computing infrastructure.

AMD’s server processor business has been particularly strong. Revenue grew by more than 50% as customers expanded deployments of its latest EPYC processors. AMD is gaining market share with its fifth-generation EPYC Turin chips, while earlier-generation products remain widely adopted across enterprise workloads.

The outlook for the server market remains highly favorable. Emerging technologies such as Agentic AI are expected to significantly increase computing requirements, creating a larger market opportunity for server processors over the coming years. Management expects server CPU revenue to grow more than 70% YoY in the second quarter and sees strong momentum continuing through the second half of 2026 and into 2027.

At the same time, AMD’s AI accelerator business is gaining traction. Its Instinct accelerators are seeing broader adoption. At the same time, existing customers are expanding usage across a wider range of AI workloads, while new customers are increasingly adopting the platform for both AI training and inference.

As global AI infrastructure spending continues to rise, AMD is positioned to benefit across multiple product categories. Management has also set strong long-term goals, targeting revenue growth above a 35% compound annual rate, adjusted operating margins exceeding 35%, and adjusted earnings per share of more than $20 within the next three to five years. These targets strengthen AMD’s bullish outlook.

AMD Stock Remains a Top AI Pick

While AMD's valuation premium over Nvidia may appear steep, the company continues to execute exceptionally well across both AI accelerators and server CPUs. With strong revenue growth, expanding market share, and significant exposure to rising AI infrastructure spending, AMD remains well-positioned to capitalize on the AI infrastructure boom.

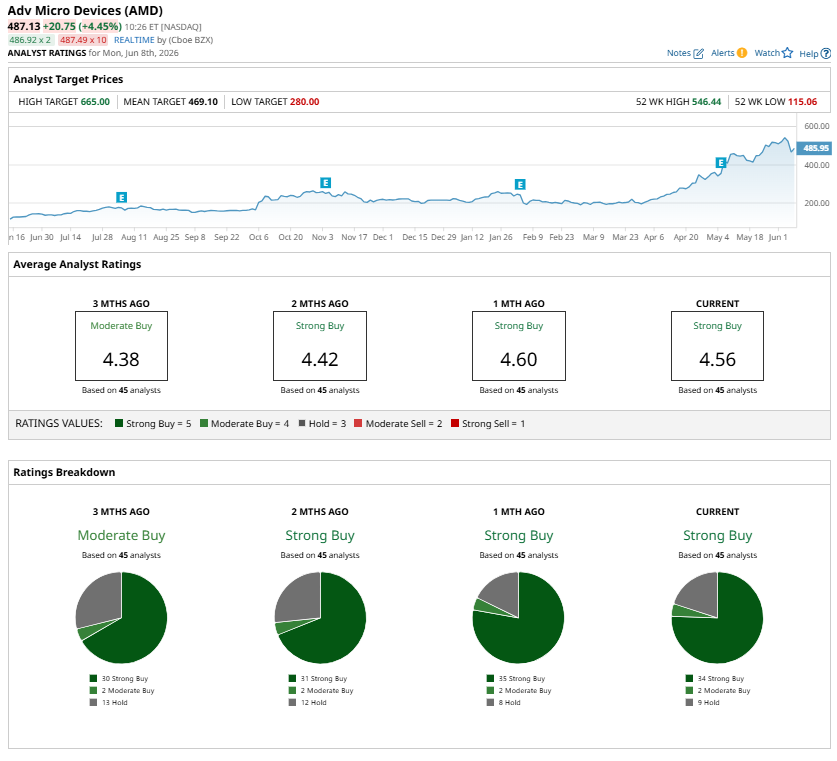

Analysts are backing AMD stock, with most of them recommending a “Strong Buy.” At the same time, analysts see a significant increase in AMD’s earnings through 2027, which justifies its premium valuation and indicates further upside potential.