/Amazon%20shopping%20page%20on%20computer%20by%20Thaspol%20Sangsee%20via%20Shutterstock.jpg)

Amazon (AMZN) hit its all-time high yesterday, April 23. The e-commerce giant is set to release its Q1 2026 earnings on April 29, after the close of markets. Let's look at Amazon’s Q1 earnings estimates and analyze whether the stock can continue its good run following the report.

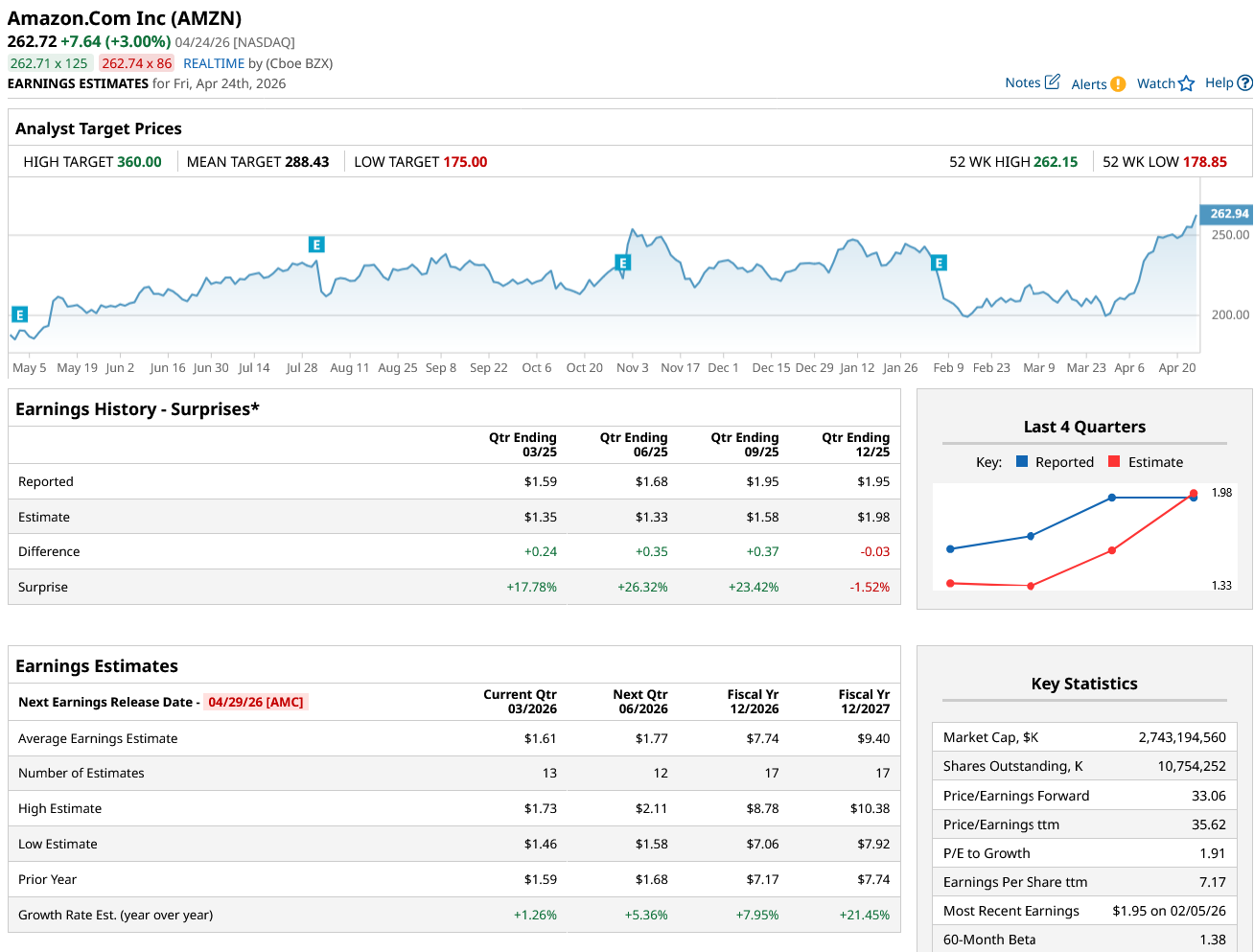

Amazon Q1 2026 Earnings Estimates

Analysts expect Amazon to report revenues of $177.2 billion in the March quarter, a year-over-year (YoY) rise of 13.8%. The estimates are towards the top end of the company’s guidance of $173.5 billion to $178.5 billion. Analysts are modeling Amazon’s Q1 earnings per share (EPS) at $1.61, which is just over 1% higher than the corresponding period last year. While Amazon does not provide EPS guidance, the company forecasted operating income between $16.5 billion and $21.5 billion, versus the $18.4 billion that it posted in Q1 2025.

To be sure, Amazon is not the only tech company whose bottom-line growth is expected to lag top-line growth. Big Tech companies have opened their coffers to build artificial intelligence (AI) infrastructure, which will put pressure on profitability over the next few quarters. Incidentally, Amazon has set its 2026 capex budget at $200 billion, which would mark the highest-ever annual capex by any company in history. The sharp increase in capex, well ahead of the $131 billion analysts were then modeling, was the key reason AMZN stock plunged following its Q4 confessional.

What To Watch in AMZN’s Q1 Earnings?

Apart from the headline numbers, I would watch out for the following in Amazon’s Q1 earnings call:

- AWS Growth: Amazon Web Services (AWS) reported a 24% rise in Q4 2025 revenues, which was the highest in 13 quarters. More recently, in the shareholder letter, CEO Andy Jassy said that AWS AI revenues were running at an annualized pace of $15 billion in Q1. The company also provided an update on its custom AI chip business, which Jassy said is “on fire” with an annual revenue run rate exceeding $20 billion and “growing triple-digit percentages.” During the Q1 earnings call, I will watch for color on AWS, particularly the AI business, along with any further updates on third-party sales of its chips.

- Capex Budget: Since the Q4 earnings call, Amazon has announced a $50 billion investment in OpenAI, of which $15 billion was an initial investment. It also invested another $5 billion in Anthropic while committing to invest another $20 billion in the future. As part of the deal, Anthropic has committed to spending over $100 billion over the next 10 years on AWS technologies, including buying Trainium chips. During the Q1 earnings call, I would look out for Amazon management’s commentary on these deals as they raise concerns over “circular financing,” wherein the investment ultimately goes into buying chips and cloud capacity from Amazon. I will also watch out for any updates on the capex budget and any financing plan the company has in mind, considering the negative free cash flows it is expected to post this year.

- New Initiatives: Earlier this month, Amazon announced that it would acquire Globalstar in an $11.6 billion deal. The acquisition will help it expand its Leo satellite network that is set for a mid-2026 launch. During the earnings call, I would look out for commentary on new initiatives like Leo, Zoox autonomous ride-hailing service, and grocery delivery.

AMZN Stock Forecast

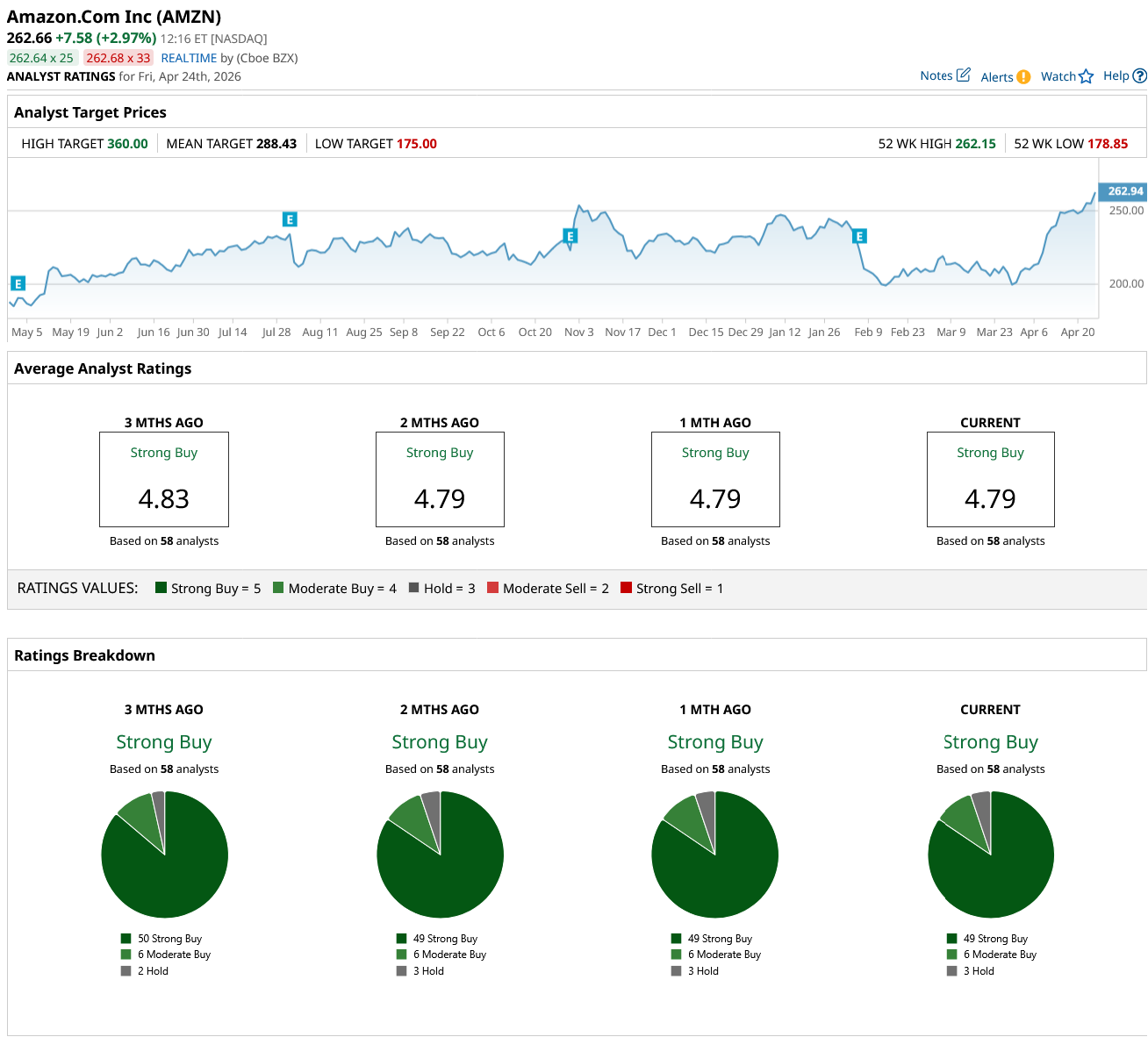

While several brokerages trimmed Amazon’s target price following the Q1 earnings, they have gradually warmed up to the stock, and Arete Research, Bernstein, BMO, Cantor Fitzgerald, KeyCorp, and Bank of America are some of the firms that have raised AMZN’s target price over the last week.

Overall, Amazon has a consensus rating of “Strong Buy” from the 58 analysts polled by Barchart, while its mean target price of $288.43 is around 10% higher than the current prices.

Should You Buy AMZN Stock?

I find AMZN stock is among the best AI plays, as apart from driving AWS growth, AI should help make Amazon’s e-commerce platform an even better proposition by improving customer experience. The stock trades at a forward price-to-earnings (P/E) multiple of 32.4x, which I find quite balanced given the risk-return trade-off.

However, while I remain bullish on Amazon and used the dip earlier this year to add to my positions, I won’t buy more shares heading into the earnings, as much of the positive news looks priced into the stock, which lowers the possibility of a post-earnings rally.