When it comes to dividend stocks, no other sector has been more reliable than the healthcare sector. No matter the economic scenario, there will always be demand for drugs treating life-threatening diseases. This keeps the sector defensive, allowing large pharmaceutical companies to generate steady cash flow and consistently reward shareholders.

Two pharmaceutical giants — AbbVie (ABBV) and Eli Lilly (LLY) — stand out for some of the fastest-growing drug portfolios in the industry. However, only one is the better choice for income-seeking investors. Let's take a closer look.

The Case for AbbVie (ABBV)

AbbVie is a global biopharmaceutical company that develops medicines for immunology, cancer, neuroscience, and aesthetics, with blockbuster drugs including Skyrizi, Rinvoq, and Botox. AbbVie’s forward dividend yield of 2.65% is higher than the market and the healthcare sector average. This higher income compounds meaningfully over a decade, especially for investors who reinvest their dividends.

When AbbVie’s top-selling drug, Humira, began losing patent protection, investors questioned whether it would weaken earnings and pressure dividends. However, the company has spent the last few years successfully replacing it, as Skyrizi and Rinvoq have become AbbVie's new growth engines, generating $6.6 billion in combined revenue in the first quarter of 2026.

Rather than relying on a single blockbuster product, AbbVie now generates meaningful revenue from immunology, neuroscience, oncology, aesthetics, eye care, and other therapeutic areas. Total revenue surged 12.4% to $15 billion in Q1, with adjusted earnings up 7.7% to $2.65 per share. This consistent earnings growth allows AbbVie to maintain its forward payout ratio, which currently stands at 64.83%. It also implies AbbVie has the room for a dividend increase while investing in R&D, acquisitions, and debt reduction.

AbbVie recently announced plans to acquire Apogee Therapeutics (APGE) for $10.9 billion. This deal will add a promising immunology pipeline that management believes has blockbuster potential and could become a meaningful earnings contributor over the next decade. Despite the heavy spending on growth, ABBV stock investors know that management views dividends as a core part of shareholder returns.

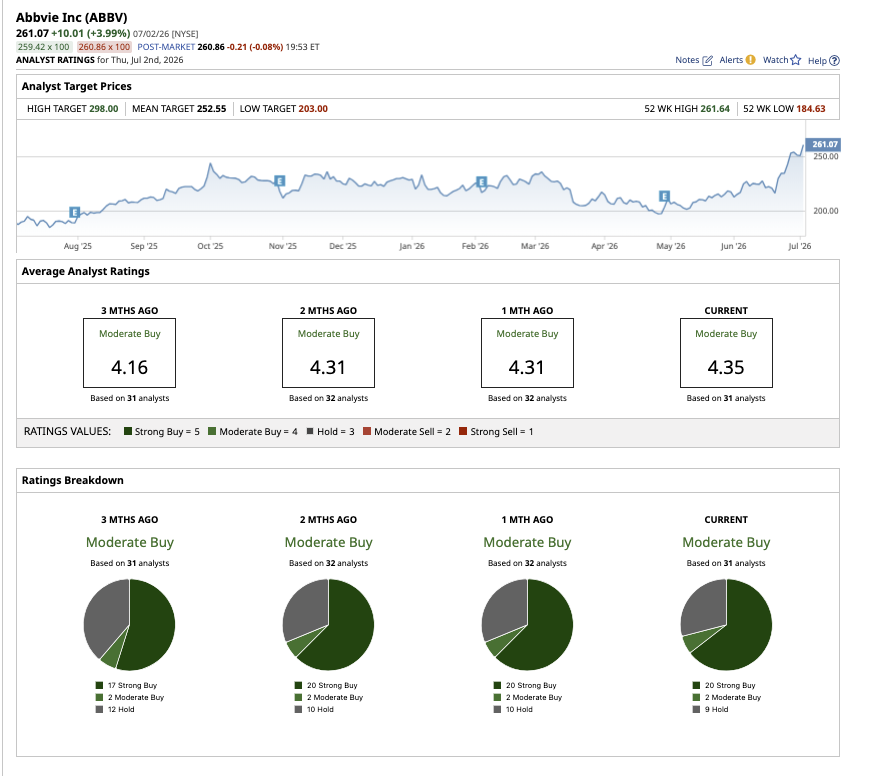

On Wall Street, ABBV stock has a consensus “Moderate Buy" rating. Out of the 31 analysts covering the stock, 20 have a “Strong Buy” rating, two suggest a “Moderate Buy,” and nine analysts recommend a “Hold.”

The Case for Eli Lilly (LLY)

Eli Lilly is a global pharmaceutical company that develops medicines for diabetes, obesity, cancer, immunology, and neuroscience, with blockbuster drugs such as Mounjaro and Zepbound driving its leadership in diabetes and obesity treatments. Eli Lilly offers a forward dividend yield of 0.57%, which is much lower than the market and the healthcare sector average, as management prefers to retain a much larger share of earnings to fund future growth. Eli Lily’s forward payout ratio of 22.28% implies dividends are safe even if earnings slow down, while also leaving enormous room to raise dividends in the future if the company chooses to do so. However, it also shows that management is prioritizing growth over income, which might not be so appealing to income investors.

Eli Lilly’s dividend may not be as appealing as AbbVie's dividend, but its growth case is certainly enticing. In the first quarter, Mounjaro revenue increased 125% year-over-year (YOY) to $8.6 billion, while Zepbound generated $4.1 billion, up 80% YOY. Total revenue jumped 56% YOY to $19.8 billion, while adjusted EPS of $8.55 climbed a whopping 156% YOY.

Demand for both Mounjaro and Zepbound continues to exceed supply in several markets, prompting Eli Lilly to invest billions of dollars into expanding manufacturing capacity. Research and development expenses totaled $3.5 billion in Q1, led by continued investments in the company's early- and late-stage portfolio. These heavy investments are currently weighing on free cash flow, which probably isn’t allowing Eli Lilly to pay higher dividends. However, these investments will position the company to capture one of the fastest-growing markets now.

Eli Lilly's growth story also extends well beyond GLP-1 drugs. The company maintains promising programs in Alzheimer's disease, oncology, immunology, and cardiovascular medicine, providing multiple opportunities for long-term revenue expansion when these new therapies reach commercialization. Hence, Eli Lilly is deliberately redirecting most of its profits back into the business.

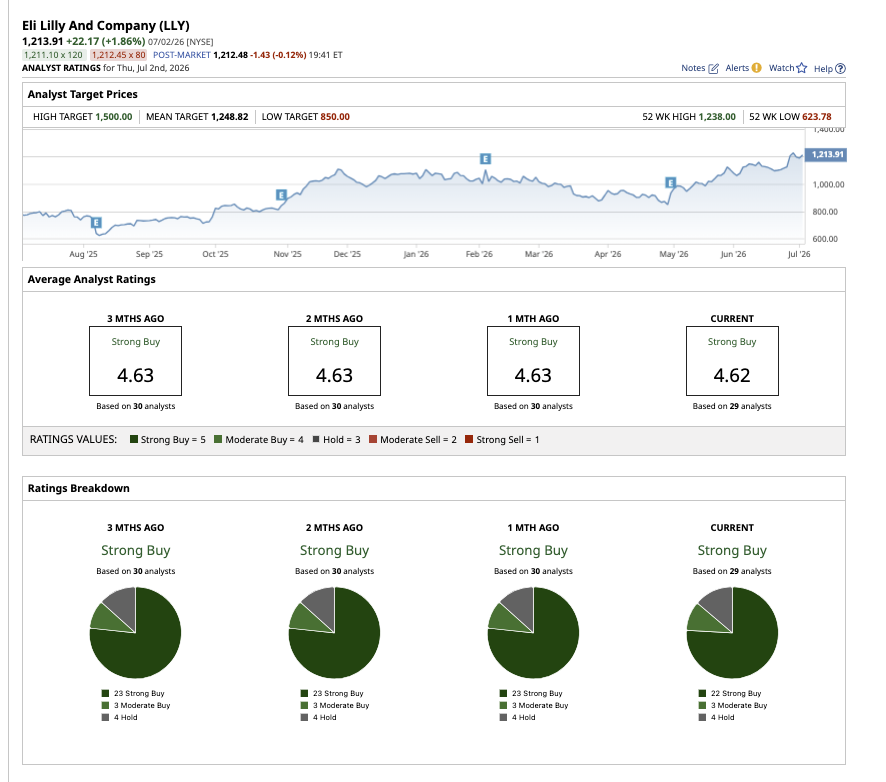

Overall, on Wall Street, LLY stock has a consensus “Strong Buy" rating. Out of the 29 analysts covering the stock, 22 have a “Strong Buy” rating, three suggest a “Moderate Buy,” and four recommend a “Hold.”

Which Is the Better Dividend Stock?

No doubt, Eli Lilly is the hottest pharma name on the market owing to its obesity drugs. Furthermore, its growth profile is extraordinary thanks to its pipeline, which remains one of the strongest in the industry.

However, when it comes to dividends, AbbVie takes the trophy home. Not only is it a Dividend King with a 54-year streak, but its dividend yield and payouts are much higher compared to Eli Lilly. This suggests that management prioritizes shareholder income, which is a green flag for income-focused investors. All told, Eli Lilly might be the superior growth stock, but AbbVie is the superior dividend stock for the next decade.