/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)

After Western Digital (WDC) announced a hefty $4 billion share buyback program and delivered remarkable fiscal second-quarter results, WDX stock is worth buying for growth investors, given the tech firm's rapid expansion, strong leverage to the AI Revolution, and relatively low valuation. Also importantly, its share buybacks can thwart short sellers, potentially igniting a short-covering rally in the name over the medium-to-long term.

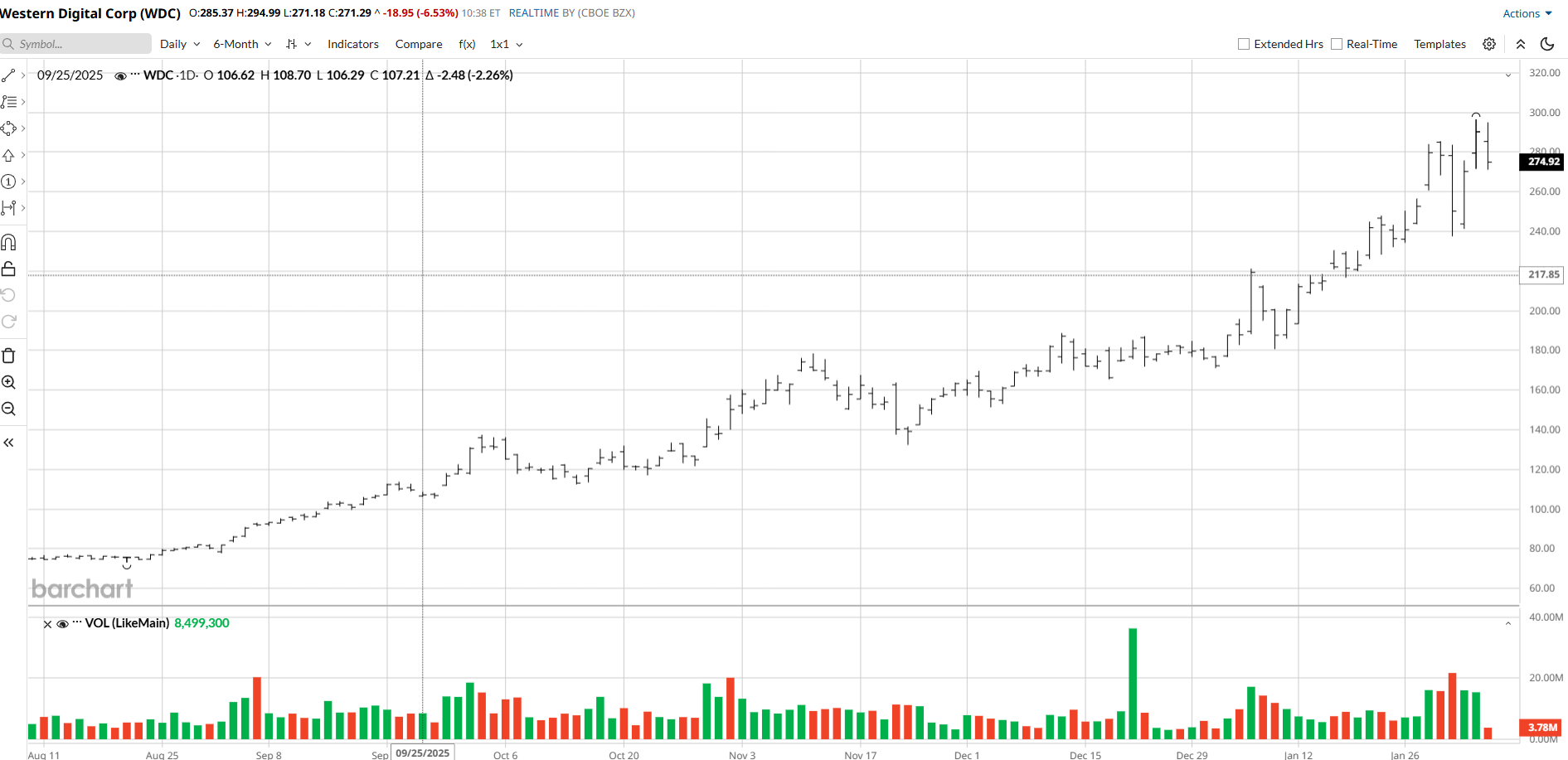

About WDC Stock

One of the largest markers of hard disk drives (HDDs) in the U.S. Western Digital is benefiting from data centers' strong demand for HDDs amid the AI boom. Its HDDs are also used in PCs and consumer electronic products.

The company has a market capitalization of $98.4 billion and a trailing price-earnings ratio of 42 times. Barchart Technical Opinion rates the shares as a Strong Buy.

WDC's Share Buyback Initiative and Q4 Numbers

On Feb. 2, Western Digital disclosed that its board had approved $4 billion of buybacks of WDC stock. The company noted that the authorization would be “effective immediately” and stated that the repurchases would be carried out based “on market conditions and other corporate considerations.” Last quarter, the firm's revenue jumped 25% versus the same period a year earlier to $3 billion, WDC reported on Jan. 29. Impressively, its operating income soared 62% year-over-year (YOY) to $908 million, helped by a 6.9 percentage-point increase in its operating margin compared with the previous year. Finally, its diluted net income per share soared 272% to $4.73 from $1.27.

A Big Beneficiary of the AI Boom

With a growing number of companies and government agencies compiling huge amounts of data to feed to AI agents and AI-powered apps, the demand for data storage is jumping, as shown by WDC's financial results. Indeed, CEO Irving Tan indicated that the firm has had a difficult time meeting the demand for its offerings. “Western Digital’s strong performance this quarter reflects our disciplined execution to meet demand in the AI-driven data economy," Tan said in a statement included in the company's earnings press release. In the wake of the company's Q2 results, Morgan Stanley (MS) expects the disk drive maker to benefit from the AI boom for a significant time period. Predicting that WDC's margins will continue to climb going forward, the firm raised its price target on the name to $369 from $306 while keeping an “Overweight” rating on the shares. And two new HDDs released by the firm recently look likely to keep data centers very interested in its products for the foreseeable future. One of the new HDDs provides double the bandwidth of traditional HDDS, while the other offers both double the bandwidth and double the I/O of standard HDDs. According to Tom's Hardware, “Over time, High-Bandwidth HDDs are projected to scale up bandwidth by eight times and I/O by four times when both approaches are combined within a single HDD.”

Using Buybacks to Thwart Short Sellers and Make a Short Squeeze More Likely

By reducing the number of shares counted in Western Digital's float, the company's massive share buybacks will increase its earnings per share and put downward pressure on its price-earnings ratio. As a result, the company's EPS growth will be lifted and it will look cheaper, making it more attractive to investors and increasing the demand for the shares. As a result of these dynamics, the stock is more likely to climb, forcing more short sellers to buy back shares. Further, the firm's share buybacks reduce the number of shares available, so it will be harder for shorts to find shares to buy, and they will likely be forced to pay more for the shares that they do locate. Finally, new short sellers will find it more difficult to find shares to short. All of these dynamics increase the chances of WDC undergoing a short squeeze. Valuation and the bottom line on WDC's forward price-earnings ratio of 36 times is a bit elevated. But given its strong growth and high leverage to the AI boom, the valuation is not excessive. Providing evidence for this assertion, the shares' PEG ratio, a measure of valuation which takes growth into account, is a rather low 0.97 times.Propelled by high leverage to AI, a $4 billion share buyback plan, and enhanced products, WDC stock appears well-positioned to outperform the stock market in the medium-to-long term.