European shares shrug off Athens slump

The Greek stock market ended 16.23% lower, its worst daily performance since 1985 when modern records began, with banking shares inevitably the main fallers. There were only nine gainers, including furniture maker Dromeas which gained around 29% after announcing - somewhat ironically given Greece’s problems with the EU - that it had wond a €30m deal to supply European Commission offices.

Elsewhere though, European shares held up remarkably well despite the slump in Athens. For a start, the decline had been expected after a five week suspension of the Greek market. There were also some reasonable eurozone PMI manufacturing figures (ignoring a shocking decline in Greece). And even though Greek banks dropped up to 30%, elsewhere the sector was buoyed by positive results from HSBC and Commerzbank.

The UK market was another exception, however, hit by a fall in mining shares following poor data from China, a key consumer of commodities. Overall the final scores showed:

- The FTSE 100 finished down 7.66 points or 0.11% lower at 6688.62

- Germany’s Dax added 1.19% to 11, 443.72

- France’s Cac closed 0.75% higher at 5120.52

- Italy’s FTSE MIB rose 0.75% to 23,714.38

- Spain’s Ibex ended up 0.76% at 11,265.9

On Wall Street the Dow Jones Industrial Average is currently down 167 points or 0.95% , following disappointing consumer spending and manufacturing data.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

And a bank on short-selling which came into effect when capital controls were introduced at the end of June and due to end today looks like it will be extended:

ESMA confirms 4-week renewal fo Greek short selling ban: BBG

— Live Squawk (@livesquawk) August 3, 2015

More meetings due between Greek officials and its creditors:

Greek FinMin @tsakalotos & Economy Min @g_stathakis to meet creditor reps Tue @ 1.30pm for talks on bank recap, privatization, & again Wed

— NikiKitsantonis (@NikiKitsantonis) August 3, 2015

Meanwhile Brent crude has dropped below $50 a barrel for the first time since January:

#BREAKING **** Brent #oil drops below $50 a barrel for the first time since January pic.twitter.com/k8h5y37rzr

— Javier Blas (@JavierBlas2) August 3, 2015

Oil has been hit by worries about the Chinese economy - with another set of weak data in the shape of the PMI manufacturing index out earlier - and the rest of the global economy. Demand seems to be slowing at the same time as there is global oversupply.

As the Athen market fell sharply on its first day of trading for five weeks, index provider MSCI has said it may reclassify its Greek market index from emerging to standalone status.

It said it may launch a consultation on such a move if capital controls continued. It said:

If there are continuing significant restrictive measures impacting the accessibility of the Greek equity market by international institutional investors, MSCI may potentially launch a consultation on a proposal regarding the reclassification of the MSCI Greece index to standalone market status from emerging markets status.

Here’s our full story on the UK government’s plan to begin selling its stake in Royal Bank of Scotland:

BREAKING NEWS

The UK government plans to sell part of its stake in Royal Bank of Scotland. It will dispose of 5.2% of the bank via a placing to institutional investors.

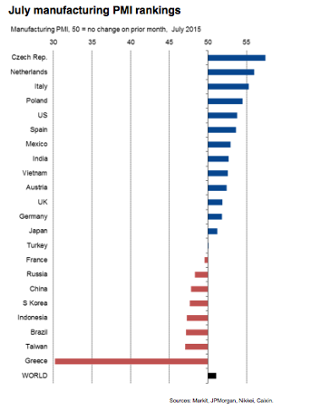

Here’s Markit’s summary of the global manufacturing PMIs for July, and it makes grim reading for Greece and its government:

Updated

The damage to the Greek economy is so severe that even if a third bailout plan is agreed, it is not likely to last very long and the country is still on course to leave the eurozone.

That is the view of Jonathan Loynes, chief European economist at Capital Economics, who writes:

The scale of the damage done to the Greek economy by the country’s renewed crisis and imposition of capital controls looks set to be far worse than the provisional plans for a third bailout envisaged and suggests that Greece is still likely to leave the currency union at some point.

Even before the Greek capital controls were implemented at the end of last month, the economy was being hit by the generally adverse effects of the renewed crisis. Although Greek GDP contracted by only 0.2% in the first quarter, the available hard data suggest that it did so much more sharply in the second quarter.

...But the damage to the economy appears to have increased much further under the capital controls. Last week’s EC business & consumer survey revealed a sharp slump in economic sentiment across all of the main sectors of the economy in July, pointing to the likelihood of much weaker levels of activity.

And this picture was supported by July’s manufacturing Purchasing Managers’ Index, which included a precipitous collapse in the output index from June’s reading of 44.8 to an incredibly weak 18.8.

...Of course, such extreme weakness may not last long if the bailout plan under discussion allows the capital controls to soon be lifted and brings the crisis to at least a temporary end. But it is far from clear that this will happen. And even if it does, sharp declines in the PMI sub-orders indices in July suggest that it would take some time for growth to recover back towards “normal” rates.

The upshot is that the scale of the damage to the Greek economy from the crisis and imposition of capital controls looks set to be worse than most forecasters, including ourselves, had envisaged.

...Perhaps more importantly, the very low starting point suggests that, even with a stronger quarterly performance, next year’s average growth figure could be even weaker at -5% or below, no doubt much worse than any figure envisaged until very recently by Greece’s creditors.

Against that economic backdrop, the requirement in the current bailout plan for Greece to build up sizeable primary budget surpluses over the next few years looks extremely demanding, if not utterly fantastical. And that, in turn, casts serious doubts over whether the plan, if it is even implemented, will last for very long. In short, the acute weakness of the Greek economy continues to point to the country’s exit from the euro-zone in the not too distant future.

On the Athens market fall, market analyst Jasper Lawler at CMC Markets UK said:

The Athens Stock Exchange plummeted on Monday; its first day of trading in five months but an improving manufacturing outlook meant other European stock markets gained as a destination for funds coming out of Greece.

Greek bank stocks went immediately limit down 30% with the rest of the market not faring much better, down as much as 23% on the open. It makes sense to see these kinds of declines given the Greece’s flirtation with an exit from the Eurozone since the stock exchange was closed five weeks ago.

That said, dropping by over 20% in a single day is almost unprecedented for the benchmark stock index of a developed country- and really is an utter pasting. It puts recent moves in China to shame.

The uncertain solvency of Greek banks had investors moving hand over fist to dump the shares as quickly as possible before the Athens Stock Exchange’s maximum loss for an individual issue was reached and trading halted.

Athens market ends down 16.23%

The Athens stock market has closed sharply lower on its first day of trading for five weeks, but it has ended off its worst levels.

It finished 16.23% lower at 668.06 have initially dropped by around 23%.

Banks however plunged 30%, hitting the daily volatility limit, with analysts expecting further falls on Tuesday. One fund manager told Reuters:

Market value is being destroyed on very light volumes as buyers stay away from bank shares. It will take some days for the market to balance out.

Updated

As we reported earlier, representatives of Greece’s lenders met labour minister Giorgos Katrougalos today.

Now Reuters is reporting labour ministry officials saying that Greece and its lenders have agreed that new pension reforms will not have any effect on anyone who was eligible to retire by the end of June.

As part of the agreement to open talks about a third bailout, Greece agreed to implement pension reforms including scrapping early retirement and raising the retirement age limit by the end of October.

The ISM report has been confirmed, and ahead of Friday’s non-farm payrolls number, analysts have been looking at the implications of today’s data:

Today's Manufacturing PMI report correlates to a 119k reading in headline NFP (data since '01, r^2 =.594) ^MW

— FOREX.com (@FOREXcom) August 3, 2015

Here’s our full report on the Tom Hayes Libor verdict:

Back with the US data and James Knightly at ING says the US Federal Reserve is likely to raise rates in September despite the weaker than expected ISM data:

ISM manufacturing index appears to have been leaked a little early with the headline index coming in at 52.7 for July versus 53.5 in June. It is also weaker than the 53.8 consensus estimate.

The report in general is mixed to slightly positive. On the positive side the output and new orders components have both risen (output up 2 at 56.0 and new orders up 0.5 at 56.5). The new orders component is at its highest this year. This suggests decent growth in manufacturing activity both for July and coming months.

However, the employment component fell to 52.7 from 55.5, which is a bit of a concern given that the labour market is key to the timing of the first Fed rate hike - last week’s FOMC statement indicated that officials want to see “some” further improvement before tightening policy. That said, the employment component remains above the 6M average of 51.6 so it isn’t terrible and doesn’t alter the outlook for a 200,000 p;us reading for non-farm payrolls on Friday.

Given the positive growth story and the likelihood of a decent payrolls figure both this month and next we think that the Fed will deliver a September hike.

(Let’s hope the leaked ISM figure is correct.....)

BREAKING NEWS

Away from the eurozone crisis for a moment and Tom Hayes, the former UBS and Citi trader, has been found guilty of all eight charges of conspiracy to defraud in the Libor trial.

Updated

The US Markit PMI for manufacturing is out, and is steady at 53.8 in July from June, exactly as expected.

The US ISM manufacturing survey for July - due in around 20 minutes - appears to have leaked early:

July manufacturing #ISM (52.7 v 53.5) released early. Details mixed: new orders (56.5 v 56.0), prod. (56.0 v 54.0), employment (52.7 v 55.5)

— Joseph A. LaVorgna (@Lavorgnanomics) August 3, 2015

This is lower than the 53.6 expected.

On Wall Street, which has just opened, the Dow Jones Industrial Average is showing an initial 19 point or 0.11% decline.

The rival Markit index is imminent.

Greece unlikely to ask for ECB emergency funding for weeks - report

Some possible good news for Greek banks.

The country is unlikely to ask for an increase in emergency funding from the European Central Bank for weeks, according to a Reuters report citing two sources, because its liquidity buffer has risen thanks to cash inflows and help from the central bank:

The bank liquidity buffer has grown to about €5bn from €1bn to €2bn at the height of Greece’s debt crisis, thanks to two Emergency Liquidity Assistance (ELA) increases from the ECB, tax and tourism inflows, and pension payments, said one of the sources, who asked not to be named.

Greek banks, closed for much of July, rely on emergency liquidity from the ECB and limit cash withdrawals to €420 per week to prevent a run on banks.

The capital controls have stopped the exodus of cash. And the increase in the buffer indicates that money is leaving banks slower than feared and they retain at least some confidence.

“There’s been relative little outflows and there was actually a week in July when there was a net inflow into the banks,” one source said.

Another source close to the process added: “There is an adequate liquidity buffer, there is no reason to ask for an increase in the ELA cap.”

The ECB increased ELA to Greek banks twice in July by €900m each time and ELA is now capped at around €9bn, of which about €5bn is unused.

Updated

Global banks may have reduced their exposure to Greece, but not entirely:

Europe's banks aren't completely out from Greece yet. HSBC just took a $92m writedown on loans there.

— Steve Slater (@reuterssteves) August 3, 2015

Greek lenders meet labour minister

Greece’s lenders are continuing their meetings with officials in Athens today, including labour minister Giorgos Katrougalos.

Greek newspaper Kathimerini reports:

Declan Costello from the European Commission, Rasmus Rueffer of the European Central Bank, Nicola Giammarioli from the European Stability Mechanism and Delia Velculescu of the International Monetary Fund met Katrougalos at his office for talks that lasted just under two hours.

Ministry sources said the aim of the discussions was for the visiting officials and Katrougalos to acquaint themselves with each other. The talks were held at the minister’s suggestion, sources added.

The government said that the main issues the four officials would be discussing on Monday are related to the justice system and combatting corruption. Tax issues are also on the agenda for Monday’s talks.

Updated

Could Greece need a second bridging loan?

In July, after much tortuous negotiation, the country received €7.16bn which it immediately used to make a due payment to the European Central Bank and to pay its arrears to the International Monetary Fund.

Now talks are underway about a third bailout, but with another €3.2bn due to be paid to the ECB on 20 August, the timing to get everything signed and sealed looks increasingly tight. Hence the suggestion that another bridging loan of perhaps €5bn might be necessary. Open Europe writes:

Focus magazine reported over the weekend that the German government is increasingly pessimistic about the negotiations over the third bailout being wrapped up any time soon. The magazine cites unnamed government sources suggesting that the special session of the Bundestag slated for mid-August in order to approve the bailout may have to be moved. This is just one in an increasingly lengthy line of reports suggesting that the bailout negotiations may not be completed in time.

As a reminder.. Greece has to repay €3.2bn to the ECB on 20 August. In order for this money to be released in time approval in a number of national parliaments needs to begin on the 12/13 August according to reports. This means the negotiations have to be completed by 10/11 of August with approval from the eurozone finance ministers coming quickly afterwards. Of course, we have seen such dates fudged before (they always seem to overestimate the time needed for national approval to give some wiggle room). But in any case there is probably between a week and two weeks before the third bailout needs to be signed, sealed and delivered. This looks incredibly optimistic – it means agreeing a three year reform programme, how much and when funds will be released, when and to what extent debt relief will be discussed or even take place and whether the IMF will be involved, amongst many other incredibly thorny issues.

How much would a second bridge loan total and where would it come from?

The agreement reached between Greece and its creditors noted that it would probably need around €5bn in August on top of the €7.16bn it received in July. Given the issues we encountered around the previous bridge loan, it is likely to once again come from the European Financial Stabilisation Mechanism (EFSM) (though I maintain that other options are on the table).

There remains just enough in the EFSM to provide a second bridge loan to Greece. Since the final tranche of the Portuguese bailout was not paid there was €13.2bn left before the €7.16bn disbursement of the first bridge loan, meaning there is conveniently the exact amount needed remaining.

...The original bridge loan was a bit of a disaster, at least in political terms. It managed to anger a number of non-Euro countries and rowed back on a previous European Council decision. It was also incredibly circular – the EU lent to Greece which repaid the ECB, the Eurozone states then guaranteed the non-Euro share of this loan with income from the ECB off the back of income from Greek bonds.

So why would the eurozone want to go through this exercise again? Well... it has little choice if it doesn’t want Greece to default on the ECB. However, it also settles a tricky problem for the eurozone – whether Greece will have to do further reforms before cash is released. By virtue of having to draw up a new EFSM bridge loan and have non-eurozone countries involved there will have to be a new short term reform programme tied to the loan. It also reduces the size of the first tranche of the loan and the total amount that needs to come from the eurozone bailout fund the ESM (though overall this makes little difference given the indemnity for non-eurozone states). These are not huge issues but may marginally be useful.

Whether the UK’s chancellor George Osborne and other non-eurozone ministers would be keen, is of course another matter.

Here’s the AP take on today’s slump in the Athens stock market:

Greece’s main stock index plunged over 22% as it reopened Monday after a five-week closure, giving investors their first opportunity since late June to react to the country’s latest economic crisis.

Greek bank stocks suffered the most, hitting or nearing the daily trading limit of a 30% loss. Markets in the rest of Europe, however, were largely unaffected.

The Athens Stock Exchange and Greek banks were closed on June 29, when the government imposed controls on money withdrawals and transfers to keep a run on bank deposits from causing the financial system to collapse.

Banks have since reopened, while maintaining strict cash withdrawal limits.

Greece is expected to head back into recession in 2015 after briefly emerging from a six-year contraction due to the effects of capital controls and months of uncertainty over the country’s future in the euro.

A monthly survey of business and consumer confidence, the Economic Sentiment Indicator, fell for a fifth consecutive month in July to its worst level since October 2012.

“The negative development is the result of the sharp deterioration in business expectations in all areas, but also a recent and significant decline in consumer confidence,” said the Foundation for Economic and Industrial Research, or IOBE, which conducts the survey.

Greece is currently in intense negotiations with bailout lenders in an effort to negotiate the terms of a massive new rescue package in the next two weeks.

The country needs to complete the talks and get more loans before August 20, when it has a repayment to make worth more than €3bn to the European Central Bank.

#EU has no comment on Greek market developments. Authorities in #Athens are more than competent enough to deal with market movements.

— Live Squawk (@livesquawk) August 3, 2015

*EU 'TAKES NOTE' OF ATHENS MARKET REOPENING, NO COMMENT ON DROP

— Stavros Kallinos (@StKallinos) August 3, 2015

Updated

The euro is under pressure after the plunge on the Athens stock market.

Having traded as high as $1.099 earlier is it now down at $1.096, although losses were mitigated by the reasonably positive manufacturing data for the eurozone as a whole.

More downbeat data from Greece.

The country’s economic sentiment index fell sharply to 81.3 points in July from 90.7, according to the Institute for Economic and Industrial Research. This is the lowest reading since October 2012. The effect of capital controls could not be fully assessed since they were still in place, said the institute, but they would add a further burden to an already shrinking economy.

Athens market now at -17.8%. Financials still at -30% limit down but some blue chips & mid-caps find buyers at these levels. #ASE #Greece

— Yannis Koutsomitis (@YanniKouts) August 3, 2015

Elsewhere though, European markets are shrugging off the slump on the Athens exchange.

After all, the decline was not exactly unexpected, not least given the falls seen in the US ADRs of Greek banks.

Strong results from HSBC and Commerzbank in German helped offset the Greek situation and the continuing worries about China in the wake of yet more weak data.

So Germany’s Dax is currently up around 0.4%, France’s Cac has climbed 0.21% and Spain’s Ibex is up 0.46%. However the FTSE 100 has slipped 0.19%, hit by a fall in mining shares after the poor Chinese manufacturing figures.

The Athens market has recovered slightly from its worst levels, but is still down 19.25% at the moment. Banks, inevitably, are the worst performers:

Updated

UK manufacturing edges higher

Meanwhile in the UK, the manufacturing PMI has edged up from 51.4 in June to 51.9, slightly better than forecasts of a rise to 51.6.

But new orders grew at their slowest pace in nearly a year, according to Markit, and to put things in context, the June figure was the lowest level in more than two years. The UK recovery looks very much dependent on consumer spending, given the weak prospects for exports to the eurozone and the strong pound. Rob Dobson at Markit said:

Although a tick higher in the headline PMI breaks the decelerating trend in UK manufacturing, growth in the sector remains near stagnant and suggests that the sector is continuing to act as a drag on the economy.

Domestic demand bolsters UK manufacturers http://t.co/CZXlcgfzSL (as demand for investment goods slumps) pic.twitter.com/02WHyNAjBY

— Chris Williamson (@WilliamsonChris) August 3, 2015

Economists agree that the weakness in exports could prove a problem. Mike Rigby, head of manufacturing at Barclays, said:

No two surveys on UK manufacturing seem to chime with each other currently with some painting a promising picture and others a bleaker one. However, what is clear is that domestic demand is still driving growth and with continuing strength in the sterling-euro exchange rate restricting the competitiveness of our exporters, the exporting surge the sector craves to boost growth and help rebalance the recovery seems further away.

Muted manufacturing activity is worrying for hopes UK growth can become more balanced & less reliant on services sector & consumer spending

— Howard Archer (@HowardArcherUK) August 3, 2015

Updated

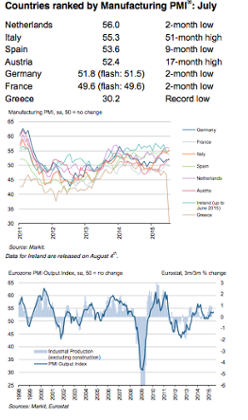

Elsewhere there has been a mixed picture for the monthly manufacturing indices.

But the overall eurozone performance was fairly steady despite the Greek crisis:

#Eurozone manufacturing expands solidly despite Greek slump. #PMI at 52.4 (June: 52.5) http://t.co/EFD23yn8WL http://t.co/oVzUZtbEEj

— Markit Economics (@MarkitEconomics) August 3, 2015

Markit said:

The eurozone manufacturing sector continued to expand at a solid steady pace at the start of the third quarter, as continued growth in the Netherlands, Italy, Spain, Austria and Germany offset the deepest contraction of the Greek manufacturing sector in the survey history.

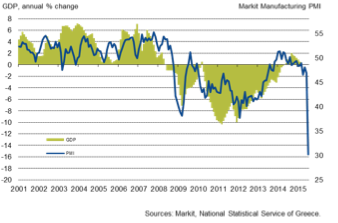

Greek manufacturing activity hits record low in July

With capital controls, banks closed and slumping demand, Greece’s factory output fell to its lowest level on record in July.

The manufacturing sector - which makes up about 10% of the economy - fell to 30.2 points according to Markit’s montly purchasing managers index. Anything below 50 is a sign of contraction. This is the worst performance since the company started compiling the data in 1999. Markit said:

July saw factory production in Greece contract sharply amid an unprecedented drop in new orders and difficulties in purchasing raw materials.

The main causes of the contraction in output were twofold: production requirements diminished as new orders plummeted while manufacturers had difficulty in sourcing materials and semi-completed goods for use in the production process.

July’s sharp decrease in the level of new business at manufacturers surpassed the previous record set in February 2012. Panel members commented on the impact of capital controls on demand, and also cited a generally uncertain operating environment which further weighed on sales.

Phil Smith, Markit economist said:

Manufacturing output collapsed in July as the debt crisis came to a head. Factories faced a record drop in new orders and were often unable to acquire the inputs they needed, particularly from abroad, as bank closures and capital restrictions badly hampered normal business activity.

Demand was hit amid the heightened uncertainty surrounding Greece’s future, leading both total new business and exports to contract sharply, and it remains to be seen how long it takes these to recover.

Although manufacturing represents only a small proportion of Greece’s total productive output, the sheer magnitude of the downturn sends a worrying signal for the health of the economy as a whole.

Heavy losses in Athens as trading resumes

The market has opened and it’s not pretty. The Athex Composite has plunged more than 20%, to 615.12. The falls are even deeper in financials, with banking shares down by as much as 30% – the maximum allowed. Market observers caution, however, that we will not know the true picture until things settle down a bit in a few hours’ time.

The 22% fall on the Athens Stock Exchange is the largest % fall even it has had #Greece

— Shaun Richards (@notayesmansecon) August 3, 2015

Updated

China woes deepen on manufacturing slowdown

The latest data from China is not good, reinforcing fears about the health of its economy and the knock-on effect on the rest of the world.

Here’s Reuters’ take on the data:

China’s factory activity shrank more than initially estimated in July, contracting the most in two years as new orders fell and dashing hopes that the world’s second-largest economy may be steadying, a private survey showed on Monday.

The report followed a downbeat official survey on Saturday which showed growth at manufacturing firms unexpectedly stalled, reinforcing views that the struggling economy needs more stimulus even as it faces fresh risks from a stock market slump.

Fears of a full-blown market crash have added a new sense of urgency for policymakers in Beijing, with many analysts expecting more support measures to be rolled out within weeks.

The final, private Caixin/Markit China Manufacturing Purchasing Managers’ Index (PMI) dropped to 47.8 in July, the lowest since July 2013, from 49.4 in June.

That was worse than a preliminary reading of 48.2 and marked the fifth straight month of contraction.

New orders contracted after growing in June, while factory output shrank for the third consecutive month to hit a trough of 47.1, a level not seen in more than 3-1/2 years.”

Introduction: Athens stock market set to re-open sharply lower

Good morning and welcome to our rolling coverage of the corporate and business world, global markets and the eurozone crisis.

It’s a big day in Athens as the stock market reopens there after its five-week suspension. Trading is scheduled to resume at 8.30am London time (10.30am Athens time) and it’s likely to be a bit of a bloodbath, with falls of up to 30% predicted. Banking stocks are expected to be hardest hit. Here’s Heather Stewart’s story on what to expect.

Just because the market’s reopening, doesn’t mean things are back to normal; far from it. As Michael Hewson at CMC Markets UK says:

“While it would be easy to suggest that today’s reopening of the Greek stock market is a key step on the road to some form of normalisation, it is likely to be anything but.

Aside from the fact that we could well see some big losses, there is the small matter that not only are the internal politics in Greece likely to remain difficult it is also likely to be extremely problematic to reconcile the positions the divergent positions of the IMF and Germany on debt relief, particularly given the proximity of the next debt deadline on 20 August.”

We’ve also had some poor manufacturing data from China; the eurozone and UK figures are due later.

On the corporate front, Europe’s largest bank, HSBC, has been hit by another $1.5bn of litigation costs but its first-half profits are ahead of forecasts. The government has also cut its stake in Lloyds Banking group again, taking it to below 14%.

Today may also be the day we get the verdict in the Tom Hayes Libor trial. We’ll be at the court in Southwark to bring you the verdict as it’s announced.

We’ll bring you more on all this throughout the day.

Updated